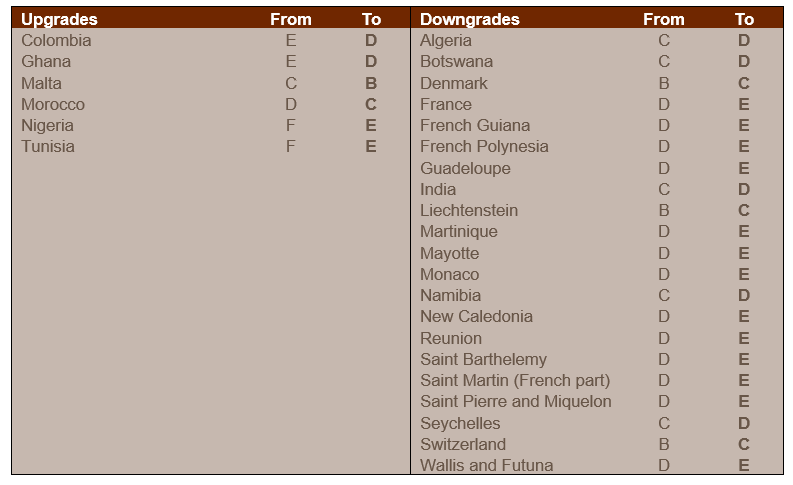

In the framework of its regular review of the business environment risk, Credendo has upgraded six countries and downgraded twenty-one countries.

Business environment risk

- Algeria: downgrade from C/G to D/G

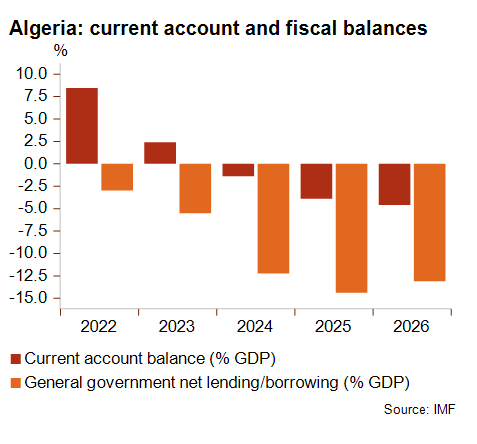

Algeria’s business environment risk has been downgraded from category C/G to D/G, reflecting the re-emergence of macroeconomic pressures. Following a temporary respite over the past three years, the country is facing once again significant fiscal and current account pressures, which are driven by limited economic reforms, the persistent reliance on the hydrocarbon sector and ongoing decline of oil prices. These pressures may further constrain the complex business climate. At the same time, recent measures aimed at curbing the large import bill and slow foreign exchange reserves erosion – such as July’s more stringent import regulations – may complicate access to foreign exchange and even lead to shortages of certain imported goods.

On a more positive note, Algeria’s growth momentum, which has characterised recent years, is expected to continue this year despite important uncertainty and headwinds facing both the MENA region and the world economy. Growth should be supported by the unravelling of oil production cuts under the OPEC+ agreement, which should partially offset the impact of lower hydrocarbon prices. Moreover, the country’s liquidity remains robust despite pressures.

- India: downgrade from C/G to D/G

The Indian rupee has been on a declining trend over the past months, including vis-à-vis a much weakened US dollar, which has lost 5% since May. Continuing depreciating pressures are possible in the near term, reflecting a slowing GDP growth and the impact of punitive US import tariffs of 50% since 27 August – the US being India’s first export market of goods (20%). Though trade talks are underway to lower US imports tariffs in exchange for concessions, some Indian red lines and harmed bilateral confidence will have to be overcome to reach a lasting agreement. Moreover, GDP is expected to reach 6.4% in the current fiscal year, ending in March 2026, which is a slightly lower growth outlook. Together with the downward pressures on the rupee, this motivated a downgrade of the business environment risk to a moderate D/G rating. However, the Goods and Services Tax reform and a resilient domestic demand could be supportive factors to the economy.

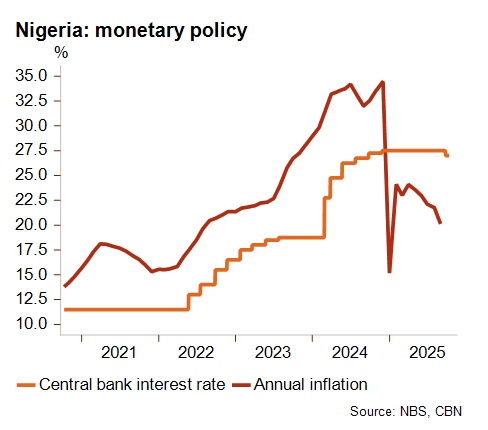

- Nigeria: upgrade from F/G to E/G

The business environment risk rating for Nigeria was upgraded from F/G to E/G, mainly because of lower inflation and the stabilisation of the naira following a period of sharp depreciation after the liberalisation of the currency initiated two years ago. President Tinubu’s ambitious monetary and fiscal reforms aimed to stabilise the macroeconomic situation and attract investments, yet their immediate impact caused a surge in inflation, a 70% depreciation of the naira and a halving of GDP in USD terms. Mid-2024, a cautious turnaround was noticeable after inflation sharply dropped, thanks to a statistical rebasing exercise, and has continued a downward path ever since (see graph). However, the IMF only expects year-on-year inflation to drop to 10% by 2029. So, despite a slowdown, inflation continues to raise the cost of living in Africa’s most populated country, causing social tensions and civil unrest. The CBN (Central Bank of Nigeria) introduced a first policy rate cut since 2020 in September 2025, but nevertheless, the policy rate remains high at 27%. Recent tax reforms have bolstered public revenue collection capacity and should improve economic growth prospects in time.

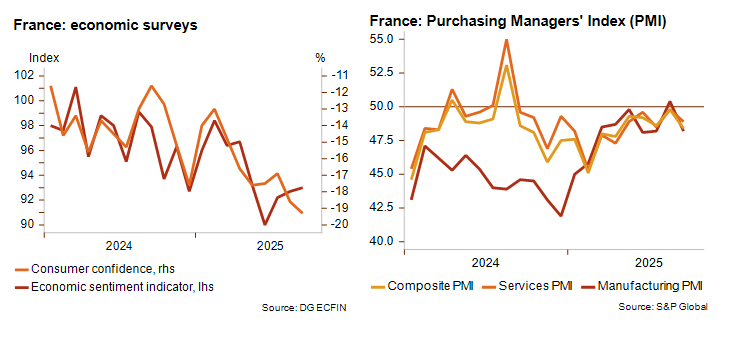

- France: downgrade from D/G to E/G

France’s business environment risk rating was downgraded from E/G to F/G. Political instability, driven by fiscal challenges and a fragmented political landscape, is currently weighing on business confidence and demand. The root of the problem lies in France’s persistent budget deficits and rising debt. As of September 2025, France’s fiscal deficit was the largest in the Eurozone and was projected to stay above 5% of GDP in 2026-27. This is significantly higher than the EU’s 3% limit, which is why France is subject to an EU Excessive Deficit Procedure. The political fragmentation, reflected by a divided parliament with no clear majority, has made it extremely challenging for the previous government to pass necessary fiscal and austerity reforms. The ongoing instability is expected to be prolonged and will likely further delay progress on these measures. Uncertainty is a major negative factor for the business sentiment.

Consequently, as highlighted by the most recent high frequency indicators, economic sentiment and consumer confidence are deteriorating and Purchasing Manager Indices (PMI) have returned to contractionary territories. Investments will likely dampen as a result. As long as more political certainty has not been restored, economic activity will tend to be weak, justifying the downgrade of the business environment risk rating.