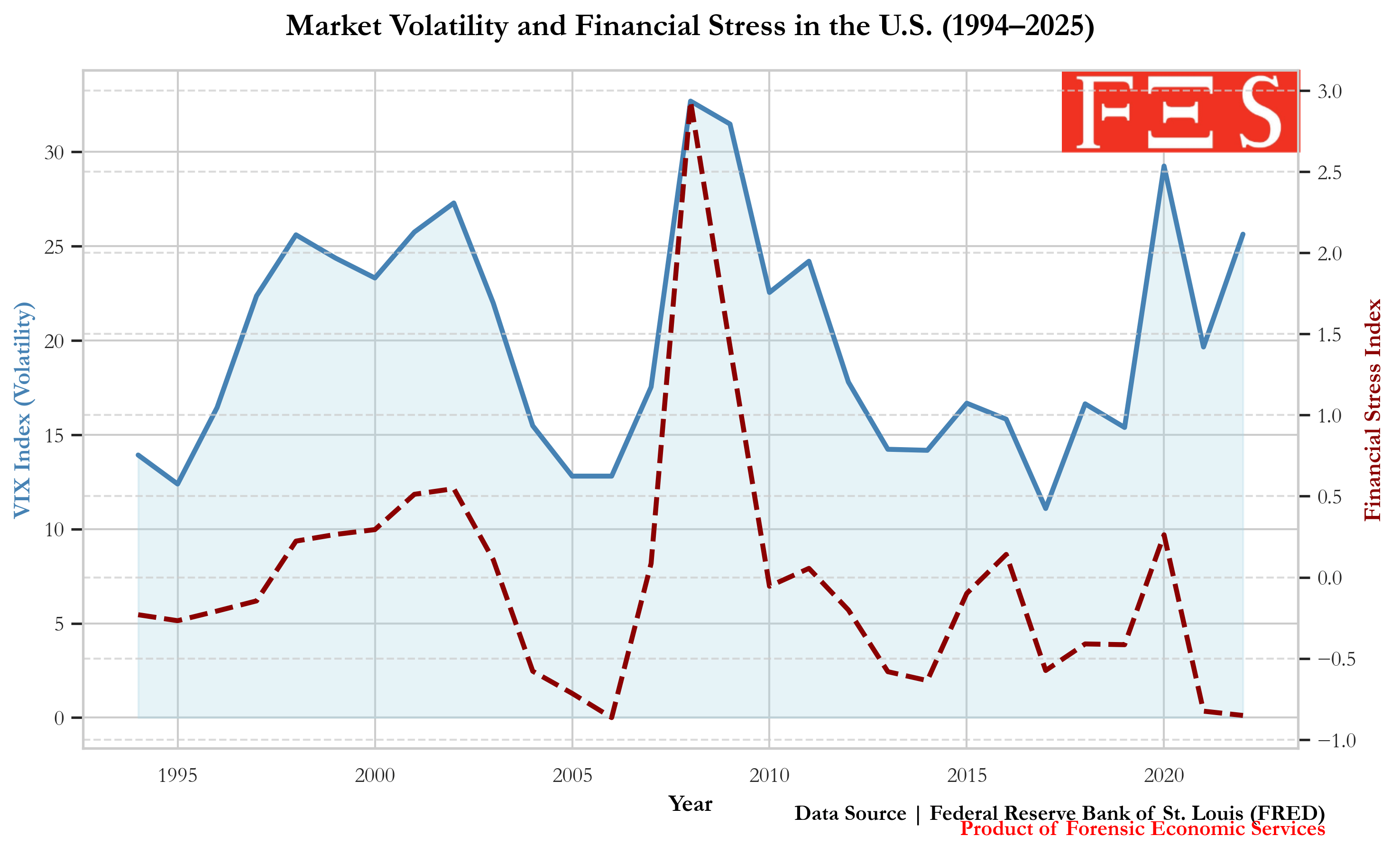

![U.S. Financial Stress and Market Volatility Since 1994 (VIX vs. STLFSI) [OC]](https://www.byteseu.com/wp-content/uploads/2025/11/nx8zz3pt734g1-1536x937.png "U.S. Financial Stress and Market Volatility Since 1994 (VIX vs. STLFSI) [OC]")

Data Source: Federal Reserve Bank of St. Louis (FRED) — VIXCLS (https://fred.stlouisfed.org/series/VIXCLS) & STLFSI2 (https://fred.stlouisfed.org/series/STLFSI2) | Tools: R, tidyverse, ggplot2

This visualization compares the CBOE Volatility Index (VIX) with the St. Louis Financial Stress Index (STLFSI) from 1994 through 2025.

Series Used:

- VIXCLS — CBOE Volatility Index

- STLFSI2 — St. Louis Fed Financial Stress Index

The VIX reflects expected stock-market volatility, while the STLFSI summarizes 18 financial indicators related to funding, credit, and market stress.

A few patterns that stand out:

- 2008–2009: Both volatility and overall stress spike dramatically during the Global Financial Crisis.

- 2020: Volatility surges during the onset of COVID-19, but financial stress rises less sharply due to rapid policy intervention.

- Post-2020: Financial stress falls below zero (below-average), while volatility remains more erratic.

Data were pulled directly from FRED using the API and aggregated into annual averages for clarity.

Happy to share the R code if anyone wants it.

Posted by forensiceconomics