Europe Agricultural Tractors Market Size

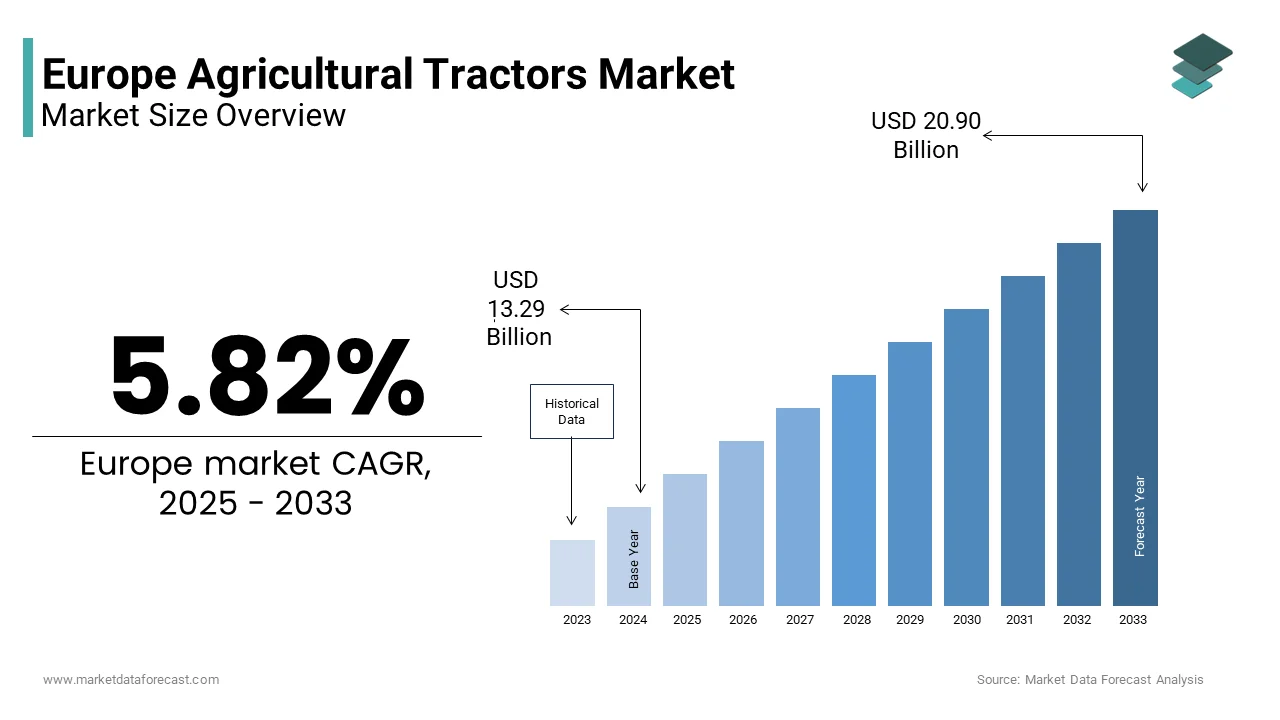

The Europe agricultural tractors market was valued at USD 12.56 billion in 2024 and is anticipated to reach USD 13.29 billion in 2025 to USD 20.90 billion by 2033, growing at a CAGR of 5.82% during the forecast period from 2025 to 2033.

Agricultural tractors are a cornerstone of the continent’s mechanized agricultural framework, defined by the deployment of power-driven vehicles engineered to execute core field operations such as plowing, seeding, hauling, and harvesting. These machines function as indispensable tools for enhancing productivity, mitigating labor shortages, and enabling precision cultivation across Europe’s diverse agroecological zones. According to Eurostat, small and medium-sized holdings dominate Europe’s farming structure, accounting for more than 80% of all agricultural operations. Europe’s utilised agricultural area spans approximately 170 million hectares, as documented by the Food and Agriculture Organization of the United Nations. Moreover, agriculture continues to sustain rural livelihoods, with more than 9 million individuals employed in farming activities across the European Union, as reported by the European Commission. As environmental sustainability and digital integration reshape agricultural paradigms, tractors are evolving from mere mechanical assets into intelligent platforms aligned with Europe’s green and digital transitions without reliance on market valuation metrics.

MARKET DRIVERS Modernization Imperative in Aging Farm Equipment Fleet

Europe’s agricultural sector faces mounting pressure to rejuvenate its aging tractor inventory, a significant proportion of which predates current efficiency and emissions benchmarks and is one of the major factors propelling the agricultural tractors market growth in Europe. According to the European Environment Agency, a large share of tractors in Western Europe were manufactured before 2000, making them incompatible with modern precision agriculture systems and costly to maintain. The European Union’s Stage V emission standards, fully enforced since 2019, mandate substantial reductions in particulate matter and nitrogen oxide outputs, which is compelling farmers to transition toward compliant machinery. National policies in key markets such as Germany and France actively encourage this shift. According to Germany’s CAP Strategic Plan, billions of euros in subsidies are available annually, with replacement grants tied to emission performance criteria. This regulatory and financial ecosystem accelerates equipment turnover cycles, which is reinforcing tractor replacement as a non‑discretionary investment rather than an optional upgrade. Consequently, the demand for newer models equipped with advanced engine technologies, automated controls, and digital interfaces remains robust across both commercial and family‑run farms.

Policy Driven Acceleration of Sustainable Farming Practices

The institutional push toward environmentally responsible agriculture is further contributing to the expansion of the European agricultural tractors market. Anchored by the European Green Deal and its Farm to Fork Strategy, the EU has set ambitious targets including a 50% reduction in pesticide use and risk, and a 20% reduction in fertilizer use by 2030. Achieving these goals necessitates machinery capable of precision input application as these functions predominantly delivered through modern tractors integrated with GPS guidance, variable rate technology, and soil sensing systems. According to the European Commission, CAP Strategic Plans for 2023–2027 direct a significant share of funding toward climate and environmental objectives. This financial realignment incentivizes farmers to procure tractors that support sustainable practices. In the Netherlands, tax incentives for low‑emission machinery have supported purchases of ammonia‑reducing tractors. These policy levers not only redefine technical expectations for agricultural machinery but also embed tractor modernization within Europe’s broader food system transformation agenda.

MARKET RESTRAINTS Stringent Emission and Safety Compliance Requirements

The Europe agricultural tractors market contends with escalating regulatory complexity stemming from rigorous environmental and occupational safety mandates. The Stage V emission standards require manufacturers to incorporate costly exhaust after‑treatment systems such as diesel particulate filters and selective catalytic reduction units, raising production expenses for mid‑range models. Concurrently, safety regulations impose additional engineering burdens. According to the European Committee for Standardization and EU type‑approval rules, hundreds of criteria must be satisfied for approval of a new tractor model. These requirements disproportionately affect small‑scale farmers who dominate Europe’s agricultural landscape According to Eurostat, more than 60% of EU farms are under 5 hectares, with many operating below economic viability thresholds. Consequently, regulatory stringency, while environmentally necessary, creates affordability barriers and suppresses market penetration in economically vulnerable regions.

Demographic Decline in Agricultural Workforce

A structural headwind for tractor demand arises from Europe’s shrinking and aging farming population, which dampens long‑term investment confidence, which is further impeding the growth of the European agricultural tractors market. According to the European Commission’s agri‑food data portal, 57% of EU farm managers are over 55 years of age, while only 12% are under 40. Critically, succession planning remains weak. According to Eurofound and related studies, a majority of farms lack formal succession strategies. This demographic reality discourages capital expenditure on advanced tractors, especially those requiring technical proficiency for operation or maintenance. In Eastern Europe, informal labor remains prevalent; according to the International Labour Organization, informal employment accounts for a significant share of agricultural work in the region. The result is a preference for second‑hand or entry‑level models, which constrains the market’s upward mobility and limits adoption of next‑generation technologies.

MARKET OPPORTUNITIES Expansion of Digital Farming Ecosystems

Europe’s strategic investment in digital agriculture is forging new demand for tractors capable of functioning as integrated data platforms, which is a promising opportunity in the European agricultural tractors market. According to the European Union’s Digital Europe Programme, more than €2 billion has been committed to smart farming initiatives between 2021 and 2027, which is promoting interoperability between machinery and farm management software. Tractors equipped with ISOBUS compatibility, telematics, and automated guidance systems are increasingly essential for participation in this ecosystem. According to the Standing Committee on Agricultural Research, over 45% of large farms in Germany and the Netherlands already deploy telematics‑enabled tractors for real‑time monitoring and remote diagnostics. Additionally, the European Commission’s Code of Conduct on Agricultural Data Sharing standardizes data formats, which is enhancing the analytical value of tractor‑generated information. This convergence empowers tractors to serve not only as power sources but as mobile command centers, opening premium segments for manufacturers offering open‑architecture, data‑ready platforms compliant with Agricultural Industry Electronics Foundation protocols.

Growing Adoption of Alternative Fuel Tractors

The transition toward low‑carbon propulsion systems presents a dynamic growth frontier for the European tractor market, propelled by decarbonization policies and energy security concerns. Electric and advanced biofuel‑powered tractors are gaining traction, particularly in nations with strong renewable energy infrastructures. According to the International Energy Agency, electricity’s share in final energy consumption within EU agriculture rose to 18% in 2024 from 11% in 2020, which is signalling rapid electrification. Sweden and Austria offer subsidies covering up to 30% of the price premium for electric tractors, supporting adoption. According to Statistics Sweden, battery‑powered tractor models recorded double‑digit growth between 2022 and 2024. Concurrently, hydrotreated vegetable oil usage in agricultural machinery increased significantly in 2023, with lifecycle emissions reductions of around 70% compared to fossil diesel as per the European Biofuels Technology Platform. These developments are catalysing partnerships between tractor OEMs and energy providers to build rural refueling and recharging networks, enhancing the practicality of alternative fuel adoption.

MARKET CHALLENGES Supply Chain Vulnerabilities in Critical Components

The market faces ongoing disruption risks due to Europe’s limited self‑sufficiency in semiconductor and advanced electronics manufacturing as these components are vital for modern tractor functionality. According to the European Semiconductor Industry Association, Europe produces less than 10% of the world’s semiconductors, leaving agricultural machinery manufacturers heavily reliant on Asian suppliers. Tractors featuring automated systems require hundreds of chips each, and during the peak of the global shortage in 2022, lead times exceeded 40 weeks as per the European Automobile Manufacturers Association. Although the European Commission’s Chips Act aims to double regional semiconductor capacity by 2030, near‑term supply remains constrained. According to VDMA Agricultural Machinery Association, electronic systems now constitute up to 30% of total tractor manufacturing expenses. This dependency inflates production costs and undermines delivery reliability, compromising manufacturers’ ability to meet demand for high‑tech models, particularly in precision agriculture segments where electronic integration is non‑negotiable.

Fragmented Market Structure and Diverse Regional Requirements

Europe’s agricultural tractor market operates within a highly heterogeneous landscape shaped by divergent farm sizes, soil conditions, cropping patterns, and national regulatory nuances. According to Eurostat, average farm sizes range from 6 hectares in Romania to 135 hectares in the Czech Republic, necessitating a vast product spectrum from compact vineyard tractors to high‑horsepower arable machines. Furthermore, despite EU harmonization efforts, member states interpret technical directives differently, resulting in country‑specific compliance variations in areas such as noise limits and safety certifications. As per the European Committee of Agricultural Machinery Manufacturers, tractor producers must maintain an average of 17 localized variants per base model to satisfy fragmented requirements. This complexity inflates research and development, certification, and inventory costs while eroding economies of scale. The operational burden of managing such diversity impedes rapid innovation rollout and complicates after‑sales support networks, ultimately slowing the diffusion of advanced technologies across the continent’s multifaceted agricultural terrain.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2024 to 2033

Base Year

2024

Forecast Period

2025 to 2033

CAGR

5.82%

Segments Covered

By Machinery, and Country Analysis

Various Analyses Covered

Global, Regional and Country Level Country-Level segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe

Market Leaders Profiled

Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation (Kubota Corporation), CLAAS KGaA mbH, Kuhn Group (Bucher Industries AG), Lemken GmbH & Co. KG, SDF Group, Mahindra & Mahindra Ltd, Tractors and Farm Equipment Ltd, Amazonen-Werke H. Dreyer SE, Pottinger Landtechnik GmbH, Vaderstad AB, Maschio Gaspardo S.p.A., Salford Group (Linamar Corporation)

SEGMENTAL ANALYSIS By Machinery Insights

Among machinery types linked to tractor implement integration, the plowing and cultivating machinery segment had the major share of 40.4% of the European agricultural tractors market in 2024. The dominance of the plowing and cultivating segment in the European market is primarily attributed to the foundational role of soil preparation in European crop production cycles, where conventional and conservation tillage remain widespread despite advances in no‑till practices. As per Eurostat, European farms allocate over 30% of annual field operation time to primary and secondary tillage activities, reinforcing consistent demand for tractors compatible with moldboard plows, disc harrows, and rotary tillers. Additionally, regulatory incentives promoting soil health require periodic tillage for compaction management, further embedding plowing machinery in farm workflows. According to the European Commission, countries like France and Germany, with extensive arable land covering over 11 million and 10 million hectares respectively, exhibit particularly high utilization rates of cultivating implements. Moreover, aging soil structure in intensively farmed regions of the North European Plain necessitates regular mechanical intervention, ensuring sustained reliance on this machinery class. The segment’s entrenched operational necessity, combined with compatibility across tractor power bands, solidifies its market leadership in Europe’s mechanized agriculture landscape.

The planting machinery segment is emerging as the fastest growing category within the Europe agricultural tractors market and is anticipated to grow at a CAGR of 7.07% over the forecast period owing to the continent’s strategic pivot toward precision seeding technologies that optimize seed placement, reduce input waste, and enhance yield uniformity. As per the European Commission, over 55% of its 2023 eco‑scheme payments were linked to precision planting adoption, underscoring policy support for resource efficiency. In countries like the Netherlands and Denmark, where average farm sizes exceed 30 hectares, over 40% of arable farmers now utilize GPS‑guided seed drills integrated with tractor auto‑steering systems, according to national agricultural census data. These systems reduce seed overlap by up to 20% and improve germination rates by ensuring consistent sowing depth—a critical advantage in drought‑prone regions of Southern Europe.

REGIONAL ANALYSIS Germany Agricultural Tractors Market Analysis

Germany held 18.4% of the Europe agricultural tractors market share in 2024. The dominance of Germany in the European market is attributed to its dense network of medium‑ to large‑scale arable farms concentrated in Lower Saxony and North Rhine‑Westphalia, which together manage over six million hectares of cropland as per the Federal Statistical Office of Germany. Germany’s farming sector benefits from robust institutional support, including the Agricultural Investment Support Program, which allocated over €400 million to machinery modernization in 2024. Crucially, German farmers exhibit among the highest adoption rates of precision agriculture in Europe, with over 50% of tractors above 100 horsepower equipped with automated guidance systems, according to the VDMA Agricultural Machinery Association. This technological readiness enhances demand for high‑specification tractors compatible with advanced implements. Additionally, the country’s strong domestic manufacturing base ensures rapid access to service networks and spare parts, reducing downtime and reinforcing purchase confidence. The interplay of policy backing, digital maturity, and industrial proximity sustains Germany’s top‑tier status in Europe’s mechanized agriculture landscape.

France Agricultural Tractors Market Analysis

France captured the second leading share of the European agricultural tractors market in 2024. The country’s dominance is driven by its vast arable expanse exceeding 11 million hectares, the largest in the European Union, according to the European Commission. French agriculture emphasizes cereal and oilseed production, operations that demand high‑horsepower tractors for primary tillage and planting across extensive fields in regions like Picardy and Champagne‑Ardenne. The France 2030 investment plan has dedicated over €200 million to accelerating farm equipment decarbonization, with subsidies covering up to 30% of the cost differential for low‑emission tractors, as reported by the French Ministry of Agriculture. This policy framework is accelerating the replacement of aging fleets; over 45% of tractors in operation were manufactured before 2010, according to Agreste. Moreover, cooperative farming structures facilitate shared machinery investments, enabling access to advanced tractors even among smaller holdings. These institutional and agronomic factors collectively sustain France’s pivotal role in Europe’s tractor market.

Italy Agricultural Tractors Market Analysis

Italy is anticipated to hold a promising share of the European agricultural tractors market over the forecast period. The country’s market is distinguished by its dual structure. The large mechanized farms in the Po Valley coexist with fragmented small holdings in the south, which is creating demand across the full power spectrum. Northern Italy alone accounts for over 60% of national tractor sales, driven by intensive maize, rice, and soybean cultivation requiring high‑capacity machinery, as per FederUnacoma. The Italian government’s National Recovery and Resilience Plan allocated €120 million in 2023 to agricultural modernization, with priority given to tractors meeting Stage V emission standards, as per the Ministry of Agricultural Policies. Additionally, Italy exhibits Europe’s highest density of specialized vineyard and orchard tractors, which is reflecting its leadership in high‑value horticulture. This diversity in farming systems ensures consistent demand for both standard and specialized tractor configurations, reinforcing Italy’s enduring market relevance.

United Kingdom Agricultural Tractors Market Analysis

The United Kingdom is anticipated to command for a prominent share of the European agricultural tractors market over the forecast period. Despite its departure from the European Union, the UK maintains a highly mechanized farming sector characterized by large cereal farms in East Anglia and livestock operations in the West. Over 85% of UK farms employ tractors as their primary source of field power, according to the Agricultural Census. The UK’s Environmental Land Management scheme now ties 50% of direct payments to sustainable practices, incentivizing adoption of precision‑ready tractors that support variable‑rate fertilization and minimal tillage—practices shown to reduce diesel consumption by up to 22%, according to Rothamsted Research. Furthermore, labor shortages exacerbated by post‑Brexit immigration rules have intensified reliance on mechanization; the agricultural workforce declined by 7% between 2020 and 2024, as documented by the Office for National Statistics. This structural pressure elevates tractor necessity beyond productivity to operational viability, underpinning steady demand even amid macroeconomic uncertainty.

Spain Agricultural Tractors Market Analysis

Spain is expected to grow at a healthy CAGR in the European agricultural tractors market over the forecast period. The country’s market dynamics are shaped by its climatic diversity, with extensive dryland cereal farming in Castilla y León contrasting with intensive irrigated horticulture in Andalusia and Murcia. This duality drives demand for both high‑horsepower tractors for large‑scale tillage and compact specialized models for olive groves and citrus orchards. Spain has experienced a 23% increase in tractor registrations since 2020, the highest growth rate in Western Europe, as per ANSEMAT, the National Association of Agricultural Machinery. This surge is partly attributable to the National Irrigation Plan, which expanded irrigated area by 400,000 hectares between 2020 and 2023, necessitating mechanization for year‑round cultivation. Additionally, EU NextGeneration funds allocated €250 million to Spanish farm modernization in 2024, with emphasis on fuel‑efficient machinery. The synergy of climate adaptation needs, policy support, and expanding irrigated agriculture sustains Spain’s upward trajectory in Europe’s tractor landscape.

COMPETITIVE LANDSCAPE

The Europe agricultural tractors market features intense competition characterized by a blend of global machinery giants and agile regional specialists. Established players leverage extensive distribution channels advanced R and D capabilities and deep agronomic understanding to maintain leadership. Simultaneously niche manufacturers cater to specialized applications such as mountain orchards and organic farms with compact and low impact models. The competitive landscape is further shaped by rapid technological evolution where digital integration emission compliance and automation define product differentiation. Regulatory alignment with EU environmental directives creates both barriers and opportunities influencing entry and expansion strategies. Companies increasingly compete not only on hardware performance but also on data services software compatibility and total cost of ownership. This multifaceted rivalry drives continuous innovation while challenging firms to balance global scale with local responsiveness across Europe’s fragmented yet technologically progressive agricultural terrain.

KEY MARKET PLAYERS

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation (Kubota Corporation)

- CLAAS KGaA mbH

- Kuhn Group (Bucher Industries AG)

- Lemken GmbH & Co. KG

- SDF Group

- Mahindra & Mahindra Ltd

- Tractors and Farm Equipment Ltd

- Amazonen-Werke H. Dreyer SE

- Pottinger Landtechnik GmbH

- Vaderstad AB

- Maschio Gaspardo S.p.A.

- Salford Group (Linamar Corporation)

Top Players In The Market

- John Deere maintains a significant presence in the Europe agricultural tractors market through its portfolio of high horsepower tractors and precision farming technologies. The company integrates advanced telematics and automated guidance systems across its European product lineup to align with the region’s sustainability imperatives. In recent years John Deere has expanded its digital farming platform in collaboration with European agri data initiatives and reinforced its service network through partnerships with local dealerships. It also inaugurated a new customer innovation center in Germany to accelerate co development of region specific tractor solutions tailored to diverse European cropping systems and regulatory requirements.

- CNH Industrial operates globally through its Case IH and New Holland Agriculture brands which are deeply embedded in Europe’s agricultural machinery landscape. The company emphasizes alternative fuel tractors including methane powered and electric prototypes tested extensively in Italy and the Netherlands. CNH Industrial has intensified its focus on circular economy principles by launching remanufactured tractor component programs across Western Europe. It also enhanced its digital ecosystem with the rollout of AFS Connect telematics compatible with EU data sharing standards. These initiatives reflect its strategic alignment with Europe’s decarbonization and digitalization agendas.

- AGCO Corporation leverages its Fendt and Massey Ferguson brands to serve varied European farming segments from small vineyards to large arable estates. The company has invested heavily in smart tractor development including the launch of the Fendt Seven series with fully integrated precision planting suites. AGCO strengthened its European footprint by expanding its logistics hub in Switzerland and establishing training academies for digital farming in France and Poland. Its recent collaboration with European research institutions on autonomous tractor trials further underscores its commitment to advancing next generation mechanization solutions across the continent.

Top Strategies Used by the Key Market Participants

Key players in the Europe agricultural tractors market deploy a range of strategic initiatives to sustain competitiveness and meet evolving regulatory and technological demands. Product innovation centered on emission compliant and digitally enabled tractors forms a core pillar with manufacturers consistently upgrading engine systems and integrating precision agriculture tools. Strategic collaborations with technology providers and agronomic data platforms enhance interoperability and user value. Expansion of after sales service networks ensures operational continuity for farmers. Investment in alternative propulsion systems including electric and biofuel powered models addresses decarbonization pressures. Additionally, companies pursue localized manufacturing and training programs to strengthen customer relationships and accelerate adoption of advanced machinery across diverse European agricultural contexts.

MARKET SEGMENTATION

This research report on the Europe agricultural tractors market is segmented and sub-segmented into the following categories.

By Machinery Type

- Plowing and Cultivating Machinery

- Plows

- Harrows

- Rotovators and Cultivators

- Other Plowing and Cultivating Machinery

- Seed Drills

- Planters

- Spreaders

- Other Planting Machinery

- Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe