Breadcrumb Trail Links

Official statistics will eventually reflect this contraction, but only after the fact

Restaurant owner posting a permanent close sign. Getty Images

Restaurant owner posting a permanent close sign. Getty Images

Article content

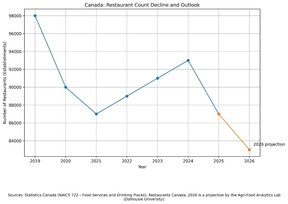

According to official figures, Canada’s restaurant sector appears remarkably resilient. The number of food service establishments has climbed steadily since the pandemic, surpassing pre-2020 levels and suggesting a sector that has not only recovered, but expanded. On paper, the industry looks stable.

Advertisement 2

Article content

On the ground, it does not.

Article content

Article content

Based on current cost trajectories, balance-sheet conditions, and consumer behaviour, we expect Canada to lose roughly 4,000 restaurants on a net basis in 2026. This adjustment is already underway, even if it is not yet visible in headline statistics.

The lived reality of Canada’s restaurant economy tells a very different story — one defined by margin compression, rising fixed costs, softening demand, and mounting financial fatigue. Speak with operators, suppliers, landlords, insurers, or lenders and a consistent picture emerges: Closures are accelerating, balance sheets are deteriorating, and survival increasingly depends on short-term coping strategies rather than long-term viability.

The problem is not that restaurants are failing suddenly. It is that the sector has been operating in a prolonged state of economic stress since 2021, masked temporarily by extraordinary policy interventions. Pandemic-era supports — wage subsidies, rent relief, loan deferrals, tax postponements — kept thousands of establishments afloat long after their underlying cost structures had become misaligned with market conditions. These measures were effective at preventing an immediate collapse, but they also delayed the necessary adjustment.

Your Midday Sun

Article content

Advertisement 3

Article content

That adjustment is now unavoidable.

Business model has changed

The restaurant business model has fundamentally shifted. Labour costs are structurally higher and unlikely to reverse. Commercial rents are resetting upward just as consumer traffic weakens. Insurance, utilities, compliance, and financing costs continue to rise. At the same time, Canadians are eating out less frequently and spending more cautiously when they do. Restaurants remain price takers in this environment, squeezed between rising input costs and demand that is increasingly price-sensitive.

Critically, one of the industry’s most reliable margin levers is also eroding: Alcohol sales. Canadians are drinking less alcohol overall, driven by higher prices, health considerations, and changing social norms. For restaurants, this shift is consequential. Alcohol — particularly beer, wine and spirits — has historically subsidized food margins. As alcohol volumes decline, operators lose one of the few high-margin categories capable of offsetting rising kitchen and labour costs. Replacing those margins through food alone is economically difficult in a consumer environment already resistant to further price increases.

Advertisement 4

Article content

Menu price inflation, often misinterpreted as a sign of pricing power, is in fact a symptom of distress. Operators are raising prices to slow losses, not to expand margins. Many are surviving by drawing down savings, refinancing debt, renegotiating leases, or delaying reinvestment. These are not indicators of health — they are indicators of exhaustion.

Business closures do not occur when conditions deteriorate — they occur when resilience is depleted. Owners exhaust personal capital, restructure debt, and postpone difficult decisions in the hope that conditions improve. For many restaurants, that hope carried them through 2023 and 2024. By 2026, the arithmetic becomes unavoidable. Pandemic-era loans mature, deferred liabilities crystallize, and margins that were already thin turn negative.

Losses will hurt independents more

The losses will not be evenly distributed. Independent restaurants — those without scale, brand leverage, or balance-sheet flexibility — are likely to absorb the majority of the contraction. These businesses are also among the sector’s most important contributors to food innovation and culinary artistry. They are often the first to experiment, the first to take risks, and the first to introduce Canadians to new cuisines, flavours, and dining concepts that later become mainstream.

Advertisement 5

Article content

Their disappearance would represent more than an economic correction. It would narrow Canada’s culinary landscape, reduce experimentation, and weaken the ecosystem that allows food culture to evolve at the neighbourhood level.

Official statistics will eventually reflect this contraction, but only after the fact. Establishment counts are inherently backward-looking, particularly in sectors dominated by small and independently owned businesses. By the time the decline becomes visible in aggregate data, thousands of operators will already have exited the market.

Policymakers underestimate urgency

The greater risk is not statistical lag, but policy misinterpretation. Headline growth figures can create a false sense of stability, leading policymakers to underestimate the urgency of reform — whether in labour policy, commercial leasing, taxation, or regulatory burden. Confusing administrative survival with economic viability risks leaving the sector without the tools it needs to adapt.

The restaurant sector is not collapsing overnight. It is contracting quietly, unevenly and structurally. The warning signs are already visible for those willing to look beyond topline counts and focus on fundamentals.

By 2026, the data will catch up to the economics. Unfortunately, many of Canada’s most creative and culturally important restaurants will not.

– Sylvain Charlebois is director of the Agri-Food Analytics Lab at Dalhousie University, co-host of The Food Professor Podcast and visiting scholar at McGill University

Article content

Share this article in your social network