Valuation After New Rail Partnership Opens Sustainability-Focused Growth Avenues")

Shares of Global Business Travel Group (GBTG) moved after parent investor Certares partnered with Italian rail operator FS to promote high speed rail over short haul flights, a development tied closely to rising sustainability priorities.

See our latest analysis for Global Business Travel Group.

The sustainability focused rail partnership arrives at a time when GBTG’s share price, last closing at US$8.15, has a 7 day share price return of 8.38% and a 90 day share price return of 8.09%. The 3 year total shareholder return of 24.24% contrasts with a 1 year total shareholder return decline of 5.12%, which suggests that recent momentum has picked up after a weaker period for longer term holders.

If you’re weighing how GBTG fits into your broader portfolio, it can be useful to compare it with other travel exposed names such as auto manufacturers that intersect with corporate and leisure demand trends.

With GBTG trading at US$8.15 alongside an implied discount to some valuation estimates, the real question for you is whether the current price underestimates its rail linked growth potential, or if the market is already pricing that in.

Most Popular Narrative: 24.9% Undervalued

Compared with the last close at US$8.15, the most followed narrative points to a higher fair value, built around earnings power and margin expansion.

The pending acquisition of CWT, now cleared for completion in Q3, is expected to drive substantial net synergies ($155 million targeted over three years), delivering scale and operational efficiency that should enhance EBITDA margins and long-term earnings power.

Curious what turns a travel platform on slim profits into a business some think deserves a higher price tag? The narrative leans heavily on faster earnings growth than revenue, a sharp lift in margins and a future earnings multiple that currently sits closer to premium hospitality names than its own history. Want to see exactly how those moving parts stack up to reach the fair value estimate? Read on and pressure test the assumptions yourself.

Result: Fair Value of $10.86 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this hinges on CWT integration going smoothly and travel budgets holding up, as costlier customer acquisition and softer demand in key client industries could quickly pressure that earnings story.

Find out about the key risks to this Global Business Travel Group narrative.

Another View On Value

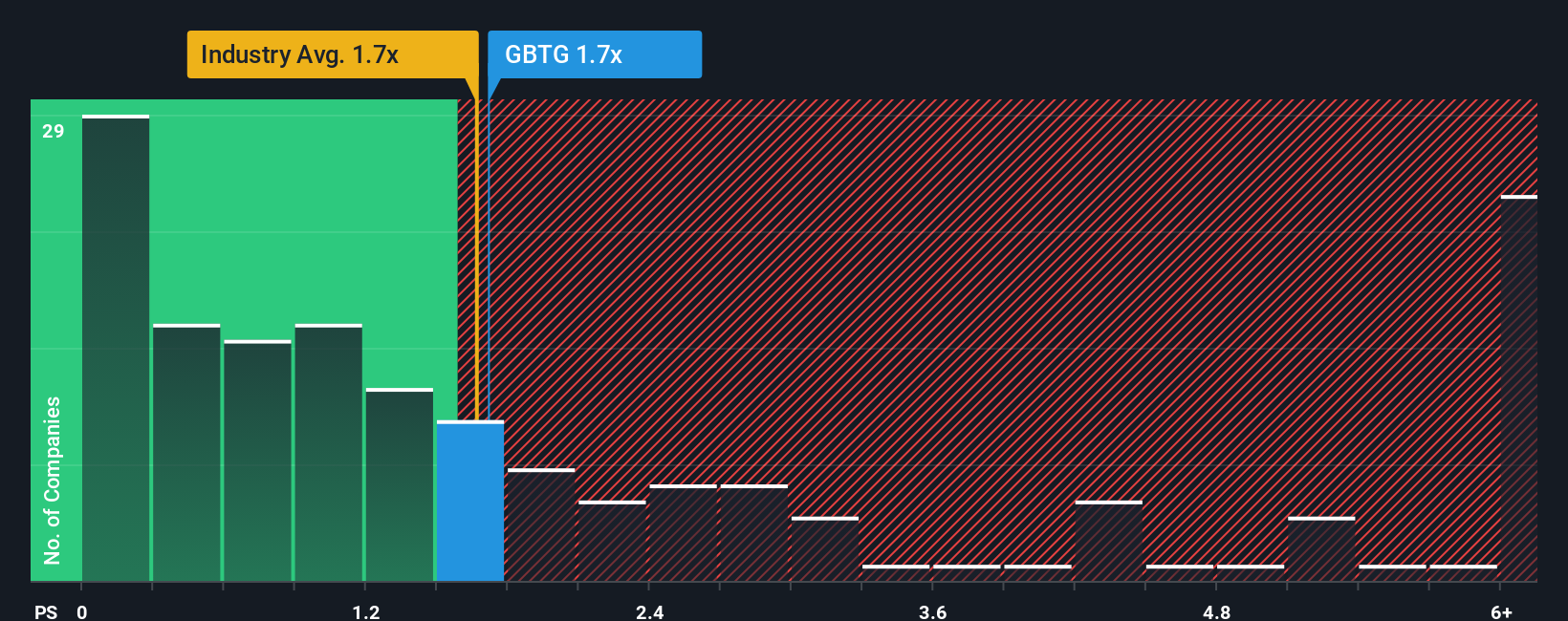

That 24.9% implied upside is rooted in earnings forecasts and margin lift, but the current P/S ratio of 1.7x tells a more mixed story. It sits in line with the US Hospitality average of 1.7x, yet well below peers at 3.7x and a fair ratio of 2.2x.

In plain terms, the market is pricing GBTG like the sector average even though both peers and the fair ratio suggest investors may be underpaying for each dollar of sales. This could limit downside or signal missed upside. Which signal do you trust more: the story or the simple sales multiple?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:GBTG P/S Ratio as at Jan 2026 Build Your Own Global Business Travel Group Narrative

NYSE:GBTG P/S Ratio as at Jan 2026 Build Your Own Global Business Travel Group Narrative

If you think the market has this story wrong, or you prefer to weigh the numbers yourself, you can build a personalized view in just a few minutes with Do it your way

A great starting point for your Global Business Travel Group research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you want to keep an edge and not miss the next opportunity, widen your search and let data rich screeners surface fresh ideas for you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com