Cheaper Valuation Offsetting Its Weaker Earnings Outlook?")

- SM Energy recently drew attention after Zacks assigned it a Rank #5 (Strong Sell), following a decline in consensus earnings estimates that raised questions about its near-term earnings outlook.

- At the same time, SM Energy’s shares are trading at a discount to peers, creating an unusual mix of weaker earnings expectations and apparently cheaper valuation.

- With this context in mind, we’ll explore how weaker earnings estimates may influence SM Energy’s investment narrative for investors.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 23 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

What Is SM Energy’s Investment Narrative?

To be comfortable owning SM Energy today, you have to believe that its combination of discounted valuation, sizeable production base and ongoing dividends can outweigh the pressure from softer profitability trends and balance sheet risk. The recent Zacks Rank #5 (Strong Sell) on the back of lower earnings estimates sharpens that trade off rather than redefining it. Short term, the key catalysts still look tied to execution on production guidance, integration progress around its pending combination with Civitas, and management’s willingness to keep prioritizing shareholder returns despite a high level of debt and non cash earnings. Unless estimate cuts accelerate or signal deeper operational issues, this revision mostly reinforces existing concerns about earnings quality and return on equity rather than creating a new risk altogether.

However, one risk stands out that investors should not overlook around SM’s balance sheet.

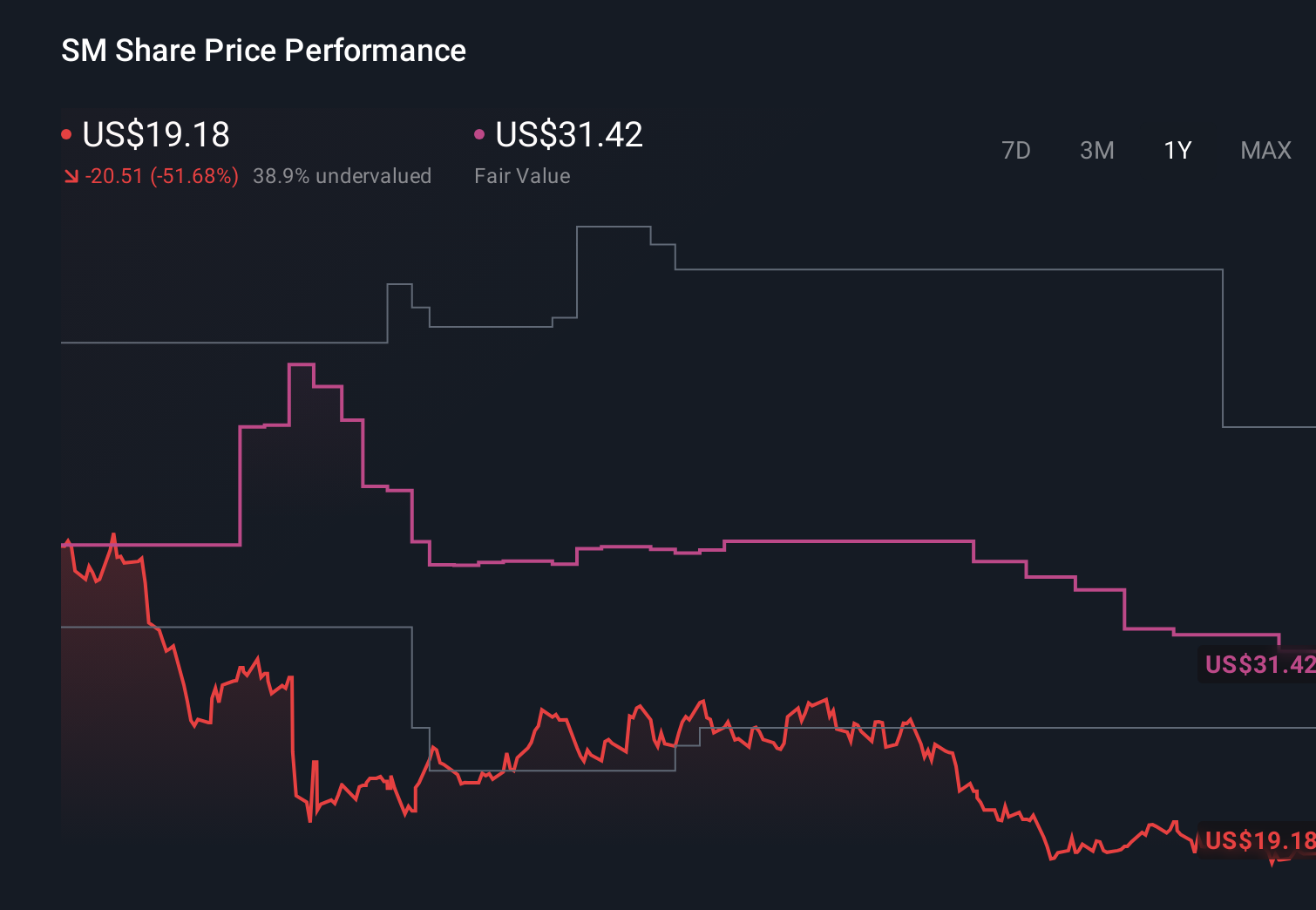

SM Energy’s shares have been on the rise but are still potentially undervalued. Find out how large the opportunity might be.Exploring Other Perspectives SM 1-Year Stock Price Chart The Simply Wall St Community’s four fair value estimates for SM Energy span from US$27 to a very large US$245.64, underlining how differently shareholders can view the same cash flow story. Set that against a stock trading well below consensus analyst targets and facing weaker earnings expectations, and it becomes clear why you may want to compare several viewpoints before deciding what SM’s future performance could look like.

SM 1-Year Stock Price Chart The Simply Wall St Community’s four fair value estimates for SM Energy span from US$27 to a very large US$245.64, underlining how differently shareholders can view the same cash flow story. Set that against a stock trading well below consensus analyst targets and facing weaker earnings expectations, and it becomes clear why you may want to compare several viewpoints before deciding what SM’s future performance could look like.

Explore 4 other fair value estimates on SM Energy – why the stock might be a potential multi-bagger!

Build Your Own SM Energy Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they’re targeting before they’ve flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com