Europe Vehicle Insurance Market Size

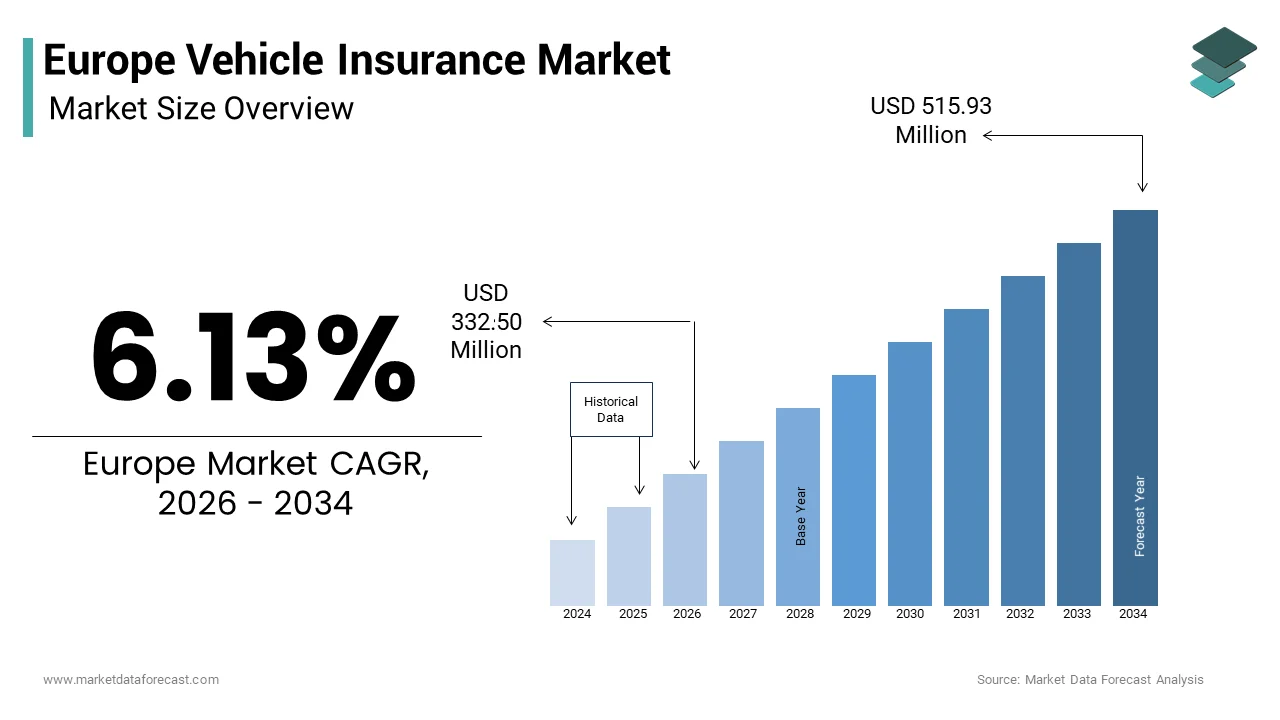

The Europe vehicle insurance market size was valued at USD 313.24 million in 2025 and is projected to reach USD 332.50 million in 2026 and from USD 515.93 million by 2034, growing at a CAGR of 6.13% during the forecast period from 2026 to 2034.

Vehicle insurance includes a range of financial protection products designed to cover liabilities and damages arising from the use of motor vehicles, including third party liability, comprehensive, and usage-based policies. This market operates within a tightly regulated framework where third party coverage is mandatory in all European Union member states under Directive 2009/103/EC. The landscape is being reshaped by technological innovation and evolving mobility patterns. As per Eurostat, there were many passenger cars registered in the European Union in 2024, establishing a vast and stable policyholder base. A significant structural shift is underway as vehicle ownership trends change. As per the European Environment Agency, urban car ownership rates have declined in major cities like Berlin and Amsterdam since 2020, driven by improved public transport and shared mobility adoption. Simultaneously, the European Commission’s General Safety Regulation mandates that all new vehicles sold from July 2024 must include advanced driver assistance systems such as automatic emergency braking and lane keeping assist, which are expected to reduce accident frequency and severity, thereby influencing long term risk modeling and premium structures across the insurance sector.

MAKET DRIVERS Mandatory Third-Party Liability Coverage Across All EU Jurisdictions

The legal requirement for third party liability insurance in every European Union member state, which is a mandate enshrined in EU law to ensure victims of traffic accidents receive compensation and propelling the expansion of the Europe vehicle insurance market. This regulatory framework creates a universal and non-discretionary demand for at least a baseline level of insurance coverage for every registered vehicle. As per the European Commission, this directive has resulted in near universal penetration, with a vast majority of registered vehicles in the EU holding valid third-party insurance. The enforcement mechanism is robust as vehicle registration and annual roadworthiness testing are contingent upon proof of insurance, which is creating a closed loop that minimizes evasion. This legal compulsion not only guarantees a stable customer base but also provides insurers with a predictable revenue stream from compulsory premiums. Furthermore, the minimum coverage limits are periodically revised upward to reflect inflation and rising medical costs to ensure the economic relevance of the product. This bedrock of mandated coverage insulates the market from economic downturns that might affect discretionary spending, which is making it a uniquely resilient segment within the broader financial services industry.

Rapid Proliferation of Telematics and Usage Based Insurance Models

The accelerating adoption of telematics technology that enables the development and deployment of usage-based insurance (UBI) policies is further contributing to the expansion of the European vehicle insurance market. This shift from traditional proxy-based risk assessment to real time data analytics is transforming customer engagement and risk management. As per the European Insurance and Occupational Pensions Authority, the number of UBI policies in Europe grew significantly in 2024, with millions of active policies now in force. Insurers leverage data from smartphone apps or embedded vehicle sensors to monitor factors such as speed, braking patterns, time of day, and distance driven, allowing them to offer personalized discounts to safe drivers. As per the German Insurance Association, UBI policyholders exhibit lower claim frequency on average, validating the model’s efficacy in promoting safer driving. This data driven approach not only enhances pricing accuracy but also fosters a proactive safety culture, aligning insurer and customer incentives in a way that traditional models cannot.

MARKET RESTRAINTS Persistent Price Sensitivity and High Customer Churn Rates

A significant restraint on the Europe vehicle insurance market is the intense price sensitivity among consumers, which fuels aggressive competition and high policyholder churn. In many European markets, vehicle insurance is viewed as a commodity, leading customers to switch providers annually in search of the lowest premium. As per a 2024 consumer survey by the European Consumer Organisation, many policyholders in Western Europe changed their insurer within the past two years, primarily driven by price comparisons on aggregator websites. This hyper competitive environment compresses profit margins and discourages long term investment in value added services, as insurers focus on short term acquisition costs. The proliferation of digital comparison platforms has exacerbated this trend, which is enabling instantaneous price shopping and reducing brand loyalty. Consequently, insurers are often trapped in a cycle of discounting to retain market share, which undermines their ability to invest in innovation or build deeper customer relationships. This dynamic is particularly acute in mature markets like the UK and Germany, where penetration is saturated and differentiation is difficult.

Complex and Fragmented Regulatory Landscape Across Member States

The growth of the Europe vehicle insurance market is also hampered by a complex and fragmented regulatory environment that varies significantly between member states, despite overarching EU directives. While third party liability is mandatory, the rules governing claims handling, no claims discount portability, premium rating factors, and data privacy differ markedly from country to country. For instance, France prohibits the use of gender in premium calculations, while Italy allows it under certain conditions, and Germany has strict rules on the use of telematics data under its national implementation of the GDPR. As per the European Insurance and Occupational Pensions Authority, these divergences increase operational complexity and compliance costs for multinational insurers, who must maintain separate underwriting and claims processes for each jurisdiction. This fragmentation acts as a barrier to cross border service provision and economies of scale, limiting the ability of insurers to deploy standardized pan European products. The administrative burden of navigating 27 different regulatory regimes stifles innovation and increases the cost of doing business, ultimately constraining market efficiency and consumer choice.

MARKET OPPORTUNITIES Integration of Electric Vehicle Specific Risk Models and Services

A major opportunity for the Europe vehicle insurance market lies in the development of specialized insurance products and services tailored to the unique risk profile of electric vehicles (EVs). As the EU accelerates its transition to zero emission mobility with a regulation mandating that all new car sales be zero emission by 2035, the insurer that can accurately model EV risks will capture significant value. Electric vehicles present distinct characteristics such as higher upfront repair costs due to complex battery systems, lower center of gravity reducing rollover risk, and different driving dynamics that influence accident patterns. As per the European Automobile Manufacturers Association, EVs accounted for a notable share of new car registrations in the EU in 2024, with projections indicating substantial growth in the coming years. Insurers are responding by partnering with OEMs to access granular vehicle data and developing policies that include EV specific benefits such as mobile charging assistance, battery degradation coverage, and preferential rates for home charger installation. This niche allows for premium differentiation and deeper customer integration within the emerging EV ecosystem.

Expansion into Mobility as a Service and Shared Fleet Insurance

The rise of new mobility paradigms, including car sharing, ride hailing and subscription-based vehicle access that create novel and complex insurance needs is another promising opportunity in the European vehicle insurance market. Traditional personal auto policies are ill suited for vehicles that switch between private and commercial use multiple times a day. This gap presents a lucrative opening for insurers to develop hybrid or on demand policies that provide seamless coverage across usage modes. As per the International Transport Forum, the number of shared mobility users in Europe is expected to grow significantly by 2026. Companies like Free Now and Bolt require fleet wide insurance solutions that cover both their drivers and passengers, while peer to peer platforms like Getaround need policies that activate only when a privately owned car is rented out. Insurers that can build flexible, real time underwriting engines capable of switching coverage based on GPS and usage data will dominate this fast-growing segment. This shift moves the industry from insuring static assets to ensuring dynamic mobility events, which is opening a new frontier of revenue and customer engagement.

MARKET CHALLENGES Escalating Repair Costs Driven by Advanced Vehicle Technology

A primary challenge confronting the Europe vehicle insurance market is the exponential increase in vehicle repair costs, driven by the integration of sophisticated sensors, cameras, and structural materials in modern automobiles. Advanced driver assistance systems (ADAS), now standard on most new cars, require precise calibration after even minor collisions, a process that is both time consuming and expensive. As per a 2025 analysis by the European Council of Independent Garages, the average cost to repair a vehicle equipped with Level 2 ADAS is significantly higher than for a comparable model without such systems. This inflation in claims severity directly pressures insurer profitability, especially as the European Commission’s General Safety Regulation mandates more of these features on all new vehicles. Furthermore, the shortage of certified technicians qualified to perform ADAS recalibrations creates bottlenecks in the repair process, extending vehicle downtime and increasing rental car expenses. These compounding factors force insurers to either raise premiums, potentially alienating price sensitive customers, or absorb losses, threatening their financial stability in a highly competitive market.

Data Privacy Constraints Limiting Personalized Underwriting Potential

The Europe vehicle insurance market faces a critical challenge in balancing the potential of data driven underwriting with the stringent data privacy regulations imposed by the General Data Protection Regulation. While telematics and connected car data offer unprecedented insights for risk assessment, the GDPR places significant restrictions on the collection, processing, and storage of personal data, including location and driving behavior. As per the European Data Protection Board, any usage-based insurance program must obtain explicit, informed consent from the policyholder and allow for easy data withdrawal, which complicates the user experience and reduces participation rates. In countries like Germany and France, national data protection authorities have issued additional guidelines that further limit the granularity of data insurers can use. This regulatory friction prevents insurers from fully leveraging the predictive power of big data, forcing them to rely on less accurate proxies for risk. Consequently, the market’s ability to achieve true actuarial fairness and offer deeply personalized pricing is fundamentally constrained by Europe’s strong privacy ethos.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

6.13%

Segments Covered

By Coverage, Application, Distribution Channel, Vehicle, and Region.

Various Analyses Covered

Global, Regional, an, Country-Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe

Market Leaders Profiled

People’s Insurance Company Of China, Allstate Insurance Company, China Pacific Insurance Co., Allianz, State Farm Mutual, Tokio Marine Group, Automobile Insurance, Geico, Ping An Insurance (Group) Company Of China, Ltd., Admiral Group Plc, Berkshire Hathaway Inc.

SEGMENTAL ANALYSIS By Coverage Insights

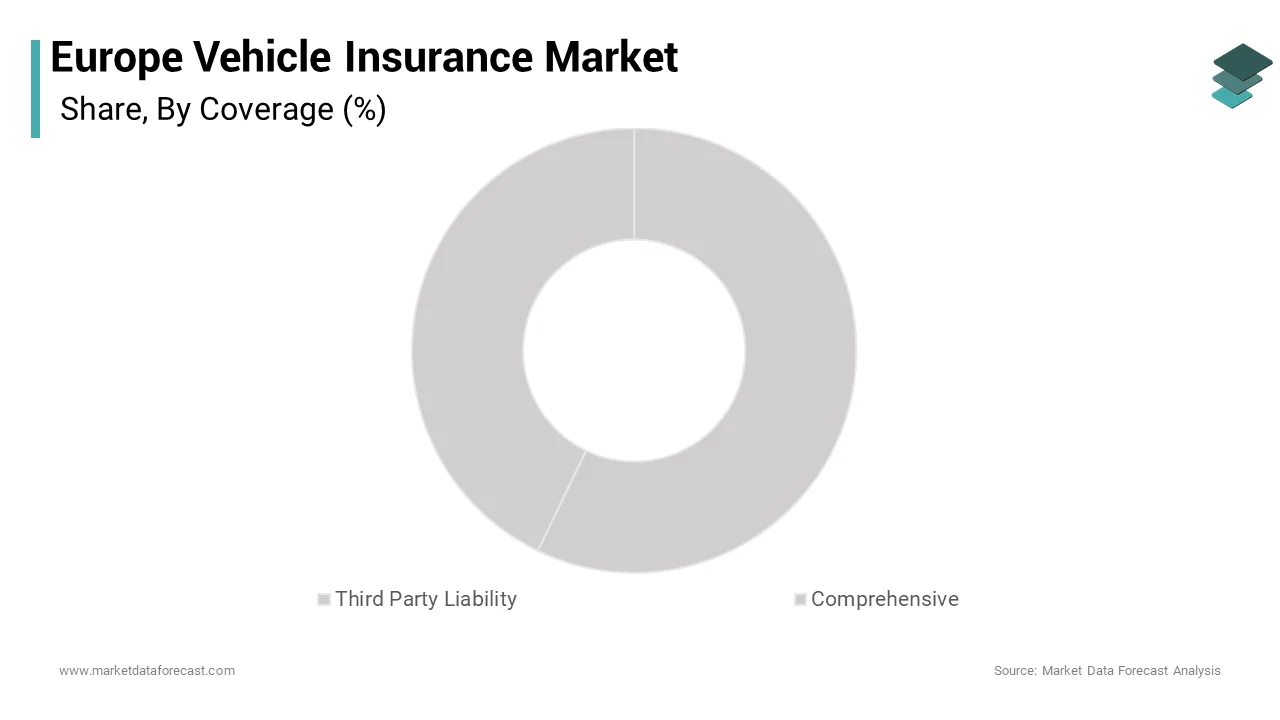

The third-party liability coverage segment commanded for the highest share of 56.5% of the regional market share in 2025. The growth of the third-party liability coverage segment in the European market is driven by its status as a legal requirement across all European Union member states under Directive 2009/103/EC, which mandates that every registered motor vehicle must carry a minimum level of insurance to cover injury or damage to third parties. As per the European Commission, this directive has resulted in near universal penetration, with a vast majority of registered vehicles in the EU holding valid third-party liability insurance. The enforcement mechanism is robust, with vehicle registration and annual roadworthiness tests contingent upon proof of coverage, effectively eliminating evasion. Furthermore, the directive sets harmonized minimum coverage limits that are periodically adjusted for inflation, maintaining the product’s economic relevance. This legal bedrock provides insurers with a stable and predictable revenue stream, insulating the segment from economic volatility that affects discretionary spending.

The comprehensive coverage segment is the fastest growing category in the Europe vehicle insurance market and is estimated to record a CAGR of 7.17% over the forecast period owing to the rising vehicle values, increasing consumer awareness of financial risk, and the proliferation of advanced safety features that make full protection more appealing. As per the European Automobile Manufacturers Association, the average new car price in the EU exceeded €35,000 in 2024, which is making out of pocket repair costs prohibitively expensive for many owners. Additionally, comprehensive policies now often include value added services such as roadside assistance, glass repair, and rental car coverage, enhancing their perceived utility. As per the German Insurance Association, a large majority of new car buyers opted for comprehensive coverage in 2025, citing peace of mind and protection against non-collision incidents like theft or natural disasters. The growing popularity of electric vehicles, which have higher repair and replacement costs due to complex battery systems, further fuels this trend.

By Application Insights

The personal vehicle segment led the market by holding 80.6% of the European market share in 2025. The dominance of the personal vehicle segment in the European market is driven by the sheer scale of private car ownership across the continent, where automobiles remain the primary mode of daily transportation for millions of households. As per Eurostat, there were many passenger cars registered for private use in the EU in 2024, forming a vast and stable policyholder base. The segment is further reinforced by cultural norms in many European countries, where car ownership is deeply embedded in suburban and rural lifestyles despite urban transit improvements. Insurers benefit from high renewal rates and well-established underwriting models for personal lines, which rely on decades of claims data related to driver age, location, and vehicle type. Moreover, the mandatory nature of third-party liability for all registered vehicles ensures that even infrequent drivers maintain active policies, creating a resilient and low churn customer pool that forms the financial backbone of the European motor insurance industry.

The commercial vehicle segment is the fastest growing application category in the Europe vehicle insurance market and is predicted to witness a CAGR of 8.84% over the forecast period owing to the explosive expansion of e commerce logistics, last mile delivery networks, and gig economy transportation services. As per Eurostat, the volume of light commercial vehicle registrations in the EU increased in 2024, driven by van purchases for delivery fleets. Companies like Amazon, DHL, and regional food delivery platforms are continuously expanding their vehicle fleets, creating sustained demand for specialized commercial motor policies. These policies are inherently more complex and higher premium than personal lines, as they cover business interruption, cargo liability, and multiple drivers. As per the International Road Transport Union, the number of professional drivers in Europe grew in 2025, reflecting the sector’s dynamism. This structural shift toward on demand mobility and home delivery is transforming commercial vehicle insurance into a high growth engine for the industry.

By Distribution Channel Insights

The insurance agents and brokers segment remain the dominant distribution channel in the Europe vehicle insurance market and held 44.9% of the European market share in 2025. The leading position of insurance agents and brokers segment in the European market is driven by the deep trust consumers place in independent advisors who can navigate the complex landscape of coverage options, compare offerings from multiple carriers, and provide personalized guidance. In many European countries, particularly in Southern and Central Europe, the broker model is culturally entrenched, with long standing relationships between families and local agencies. As per the European Insurance Intermediaries Federation, there are hundreds of thousands of licensed insurance brokers operating across the EU, serving as a critical interface between insurers and policyholders. Their value is especially pronounced in commercial vehicle and comprehensive personal lines, where policy complexity demands expert consultation. Furthermore, regulatory frameworks in countries like Germany and Italy actively support the intermediary model by requiring clear disclosure of commission structures, enhancing transparency and consumer confidence in broker mediated transactions.

The direct response channel segment is the fastest growing distribution method in the Europe vehicle insurance market and is estimated to register a CAGR of 10.5% over the forecast period owing to the digital transformation of consumer behavior, where price comparison websites and insurer owned online portals enable instant and self-service policy purchases. As per the European Consumer Organisation, many European consumers aged 18 to 45 now initiate their insurance search on digital aggregators. Insurers are investing heavily in user friendly interfaces, AI driven quote engines, and seamless digital onboarding to capture this tech savvy demographic. The model’s efficiency is unmatched; direct channels eliminate intermediary commissions, allowing for lower premiums that appeal to price sensitive customers. Moreover, the integration of telematics enrollment and digital claims filing within these platforms creates a closed loop experience that enhances retention. As broadband penetration continues to rise across the EU and mobile commerce becomes ubiquitous, the direct response model is poised to reshape the competitive dynamics of the entire market.

COUNTRY ANALYSIS Germany Vehicle Insurance Market Analysis

Germany stood as the largest national market in the Europe vehicle insurance market by holding 19.2% of the regional market share. Its position is anchored in the country’s high vehicle ownership rate, stringent regulatory environment, and mature insurance culture. As per the Federal Motor Transport Authority, Germany had over 48 million registered passenger vehicles in 2024, the highest in Europe. The market is characterized by a strong preference for comprehensive coverage, with a majority of policies including full protection, as reported by the German Insurance Association. The nation’s robust automotive industry and high average vehicle values further drive demand for sophisticated insurance products. Additionally, Germany’s strict liability laws and dense road network contribute to a high frequency of minor claims, reinforcing the perceived necessity of robust coverage. This combination of scale, affluence, and risk awareness makes Germany the most valuable and competitive market in the European motor insurance landscape.

United Kingdom Vehicle Insurance Market Analysis

The United Kingdom was the second largest market in Europe for vehicle insurance. Its prominence stems from a highly developed and competitive insurance ecosystem, dominated by a mix of global insurers and agile digital natives. As per the UK’s Department for Transport, there were 39 million licensed vehicles in 2024, with London alone hosting millions of cars. The UK pioneered the use of price comparison websites, which have fundamentally reshaped consumer behavior. As per a 2025 Financial Conduct Authority survey, a large majority of new policies were purchased after an online comparison. Despite challenges from post Brexit regulatory divergence, the UK remains a hub for innovation in usage-based insurance and telematics. The market’s sophistication, coupled with high urban congestion and accident rates, sustains strong demand for both third party and comprehensive products, ensuring its continued leadership in the European context.

France Vehicle Insurance Market Analysis

France is estimated to showcase a promising CAGR in the Europe vehicle insurance market during the forecast period owing to its unique regulatory framework and consumer protection ethos. The French market operates under the “Bonus Malus” system, a government mandated no claims discount mechanism that directly links driving behavior to premium costs, encouraging safe driving and long term policy retention. As per France’s Ministry of the Interior, there were 37 million registered vehicles in 2024, with a notable trend toward smaller, urban friendly cars. The market is also shaped by strong consumer rights; French law allows policyholders to cancel their insurance at any time after one year, fostering intense competition and innovation in customer service. As per the French Insurance Federation, a majority of policies include legal expense coverage as a standard add on, reflecting a litigious culture that increases policy complexity and value. This blend of behavioral incentives, regulatory specificity, and high service expectations defines France’s distinct and resilient insurance landscape.

Italy Vehicle Insurance Market Analysis

Italy is expected to command for a notable share of the Europe vehicle insurance market over the forecast period. The high claim frequency and a historically fragmented competitive structure are propelling the expansion of the Italian market. The country has one of the highest motor accident rates in Western Europe. As per ISTAT, Italy’s national statistics institute, there were many road accidents involving injuries in 2024. This elevated risk profile drives up premiums and reinforces the necessity of robust coverage, even in a price sensitive environment. The market has undergone significant consolidation in recent years, with major players acquiring smaller regional insurers to achieve scale and improve risk pooling. A distinctive feature is the widespread use of “RCA” (Responsabilità Civile Auto), the Italian term for third party liability, which is universally understood and mandated. Furthermore, the Italian government’s push for digitalization has led to the adoption of electronic risk certificates, streamlining renewals and reducing fraud. Despite economic headwinds, the sheer volume of vehicles and the persistent risk of accidents ensure Italy remains a cornerstone of the European motor insurance industry.

Spain Vehicle Insurance Market Analysis

Spain is anticipated to witness a healthy CAGR in the European vehicle insurance market over the forecast period. Spain is exhibiting steady growth driven by economic recovery and rising vehicle ownership. As per Spain’s Directorate General of Traffic, the national vehicle fleet surpassed 28 million units in 2024, with new car registrations growing year on year, which is the fastest pace in Southern Europe. The market is increasingly shifting toward comprehensive coverage, particularly among younger urban professionals purchasing new or nearly new vehicles. As per UNESPA, the Spanish insurance association, telematics-based policies now account for a growing share of new personal auto policies, reflecting a growing appetite for personalized pricing. Tourism also plays a role; the influx of millions of international visitors in 2024, as per the World Tourism Organization, fuels demand for short term rental car insurance. Spain’s improving economic outlook, combined with digital adoption and a young, mobile population, positions it as a dynamic and expanding market within the European motor insurance sector.

COMPETITIVE LANDSCAPE

The competition in the Europe vehicle insurance market is intense and multifaceted, characterized by a mix of pan European giants, national champions and agile digital insurers. Global players like Allianz AXA and Generali dominate through scale brand recognition and diversified product portfolios, while regional specialists such as Admiral in the UK and MAIF in France compete on niche expertise and customer loyalty. The market is further disrupted by insurtech startups offering fully digital experiences and hyper personalized policies. Price competition remains fierce due to the widespread use of comparison websites which empower consumers to switch providers easily. This dynamic has pushed incumbents to innovate rapidly in areas like telematics AI driven underwriting and EV specific coverage. Regulatory harmonization under EU directives provides a common framework but national differences in claims culture and consumer protection laws sustain local competitive nuances, making the landscape both integrated and fragmented simultaneously.

KEY MARKET PLAYERS

A Projected dominant market players are in the Europe vehicle insurance market are

- People’s Insurance Company Of China

- Allstate Insurance Company

- AXA Group

- Generali Group

- China Pacific Insurance Co.

- Allianz

- State Farm Mutual

- Tokio Marine Group

- Automobile Insurance

- Geico

- Ping An Insurance (Group) Company Of China, Ltd.

- Admiral Group Plc

- Berkshire Hathaway Inc.

Top Players In The Market

- Allianz SE is a cornerstone of the Europe vehicle insurance market, offering a comprehensive portfolio of motor insurance products across personal and commercial segments in over 20 European countries. Headquartered in Munich, the company leverages its deep regional expertise and extensive distribution network to serve millions of policyholders. Allianz contributes significantly to the global insurance landscape by pioneering data driven underwriting models and sustainable mobility solutions. To strengthen its position, Allianz launched an AI powered claims processing platform across its European operations in early 2025, reducing settlement times by up to 40%. The company has also expanded its usage-based insurance offerings in partnership with major automotive manufacturers, embedding telematics directly into new vehicles to provide real time driving feedback and personalized premiums, aligning with Europe’s evolving mobility and safety standards.

- AXA Group is a dominant force in the Europe vehicle insurance market, with a strong presence in key markets including France Germany and the UK. The company integrates advanced analytics and customer centric digital services to deliver tailored motor insurance solutions. AXA plays a pivotal role globally by championing climate resilient insurance products and promoting road safety through behavioral incentives. In 2025, AXA enhanced its DriveSmart telematics program across Southern Europe, introducing gamified safe driving challenges and instant rewards to boost engagement. It also forged a strategic alliance with leading European electric vehicle charging networks to offer integrated roadside assistance and battery support services, positioning itself at the forefront of the EV insurance ecosystem and reinforcing its commitment to innovation and sustainability in the European mobility transition.

- Generali Group is a major participant in the Europe vehicle insurance market, renowned for its localized approach and robust digital transformation strategy. Operating in over 15 European countries, Generali offers a wide range of motor policies supported by agile claims handling and preventive risk management tools. The company contributes to the global insurance sector by advancing inclusive and green insurance frameworks aligned with EU sustainability goals. To reinforce its European footprint, Generali rolled out its “MyDrive” usage-based insurance platform in Central and Eastern Europe in January 2025, featuring real time eco driving coaching and carbon footprint tracking. Additionally, it partnered with municipal authorities in Milan and Vienna to develop insurance products for shared micro mobility fleets, demonstrating its proactive adaptation to emerging urban transportation models and solidifying its relevance in the future of European mobility.

Top Strategies Used by the Key Market Participants

Key players in the Europe vehicle insurance market are deploying several strategic initiatives to maintain competitive advantage. First, they are heavily investing in artificial intelligence and machine learning to automate claims processing and enhance fraud detection accuracy. Second, they are expanding usage-based insurance programs through partnerships with automotive manufacturers and telematics providers to enable personalized pricing. Third, they are developing specialized insurance products for electric and shared mobility vehicles to address emerging risk profiles. Fourth, they are strengthening digital distribution channels by optimizing mobile apps and integrating with price comparison platforms to capture online traffic. Finally, they are embedding sustainability metrics into their policies, such as rewarding eco driving behavior and supporting circular economy initiatives, to align with European regulatory and consumer expectations on environmental responsibility.

MARKET SEGMENTATION

This research report on the Europe vehicle insurance market is segmented and sub-segmented into the following categories.

By Coverage

- Third Party Liability

- Comprehensive

By Application

- Personal Vehicle

- Commercial Vehicle

By Distribution Channel

- Insurance Agents/Brokers

- Direct Response

- Banks

- Others

By Vehicle Type

- New Vehicles

- Used Vehicles

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe