Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

-

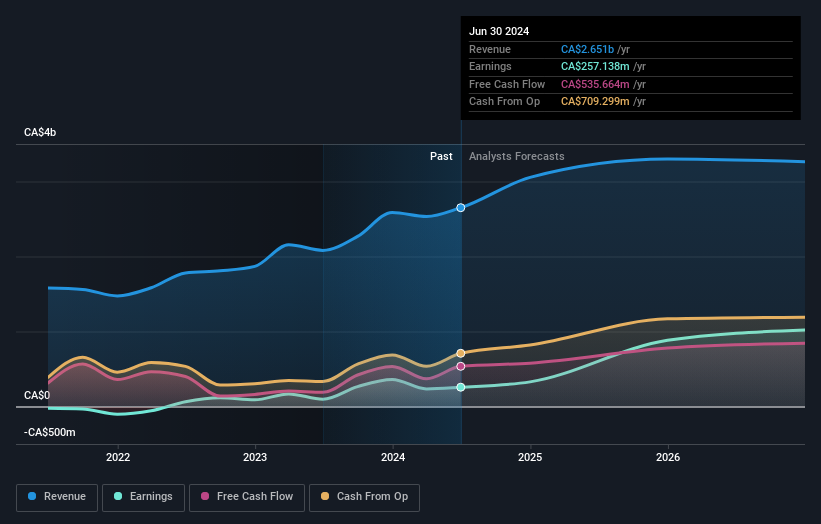

Cameco reported annual and fourth quarter results that exceeded expectations, with earnings and revenue above prior year levels.

-

The company highlighted the contribution of its investment in Westinghouse to its overall business profile.

-

Cameco pointed to growing global commitments to nuclear energy and its collaboration with the US government as key supports for its future positioning.

Cameco, traded as TSX:CCO, is drawing fresh attention after these results, with the stock up 13.7% year to date and 130.6% over the past year. At a current share price of CA$153.94, the company sits on a very large 5 year return, which reflects how strongly the market has already re-rated its role in the uranium and nuclear fuel space.

For investors watching longer term themes around decarbonization and energy security, Cameco’s deeper ties with Westinghouse and the US government are likely to be central talking points. As nuclear policies and investments continue to evolve, the company’s current positioning and recent performance provide a basis to judge how TSX:CCO might fit, or not, within a given portfolio approach.

Stay updated on the most important news stories for Cameco by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Cameco.

TSX:CCO Earnings & Revenue Growth as at Feb 2026

We’ve flagged 0 risks for Cameco. See which could impact your investment.

-

⚖️ Price vs Analyst Target: Cameco trades at CA$153.94 versus an average analyst target of CA$169.06, roughly 9% below, so the price is broadly in line with consensus expectations.

-

❌ Simply Wall St Valuation: The shares are described as trading about 22.9% above estimated fair value, which indicates a premium against that model.

-

✅ Recent Momentum: The 30 day return of about 0.08% suggests the strong 1 year move has paused rather than reversed.

There is only one way to know the right time to buy, sell or hold Cameco. Head to Simply Wall St’s company report for the latest analysis of Cameco’s Fair Value.

-

📊 The earnings beat and Westinghouse contribution highlight Cameco’s role across both uranium supply and nuclear services, which ties directly into growing nuclear commitments.

-

📊 Watch how revenue and earnings progress against the current P/E of about 127x and forward P/E of about 72x, as well as any updates on government collaborations.

-

⚠️ With the stock described as about 22.9% above estimated fair value, valuation risk is a key consideration if growth or nuclear policy momentum slows.