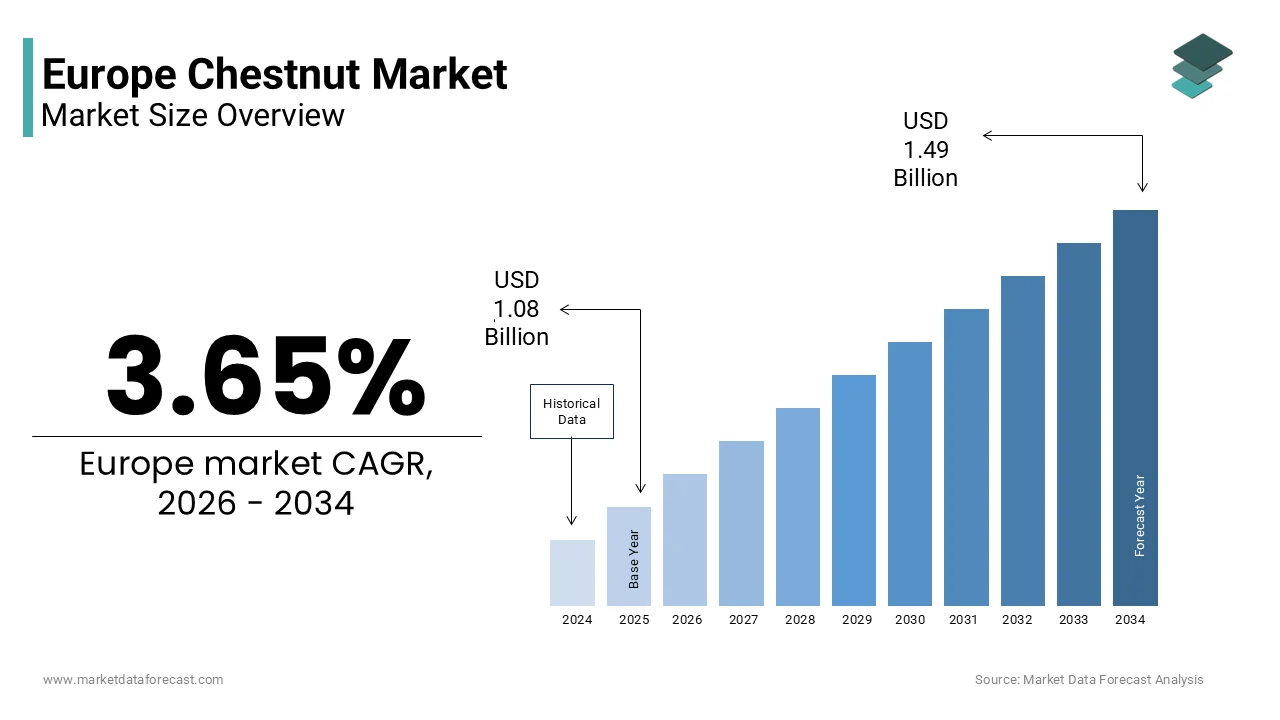

The Europe chestnut market was valued at USD 1.08 billion in 2025 and is projected to reach USD 1.49 billion by 2034 from USD 1.12 billion in 2026, growing at a CAGR of 3.65% during the forecast period. Market growth is supported by rising consumer preference for natural and plant based food products, increasing demand for chestnut based bakery and confectionery items, and expanding applications in processed and packaged foods. Seasonal consumption patterns, growing awareness of the nutritional benefits of chestnuts such as high fiber and antioxidant content, and the strong culinary heritage of chestnut usage across Southern Europe are further driving steady market expansion.

Key Market Trends

- Rising demand for fresh and minimally processed chestnuts due to increasing consumer focus on clean label and natural food ingredients.

- Growing use of chestnut flour in gluten free bakery and specialty food products across European markets.

- Expansion of organized retail channels, particularly supermarkets and hypermarkets, enhancing product visibility and accessibility.

- Increasing incorporation of chestnuts in ready to eat meals, desserts, and confectionery items within the food processing industry.

- Strengthening domestic production and regional sourcing strategies to maintain product quality and seasonal supply stability.

Segmental Insights

- Based on product type, the fresh chestnuts segment dominated the Europe chestnut market in 2025. The segment’s leadership is attributed to strong traditional consumption, seasonal demand during festive periods, and consumer preference for whole, unprocessed chestnuts in roasting and culinary applications.

- Based on application, the food industry segment led the Europe chestnut market in 2025. Chestnuts are widely utilized in bakery products, confectionery, purees, soups, and specialty dishes, making the food processing sector the primary revenue contributor.

- Based on distribution channel, the supermarkets segment held the majority share of the Europe chestnut market in 2025. The dominance of supermarkets is driven by broad product assortment, private label offerings, competitive pricing strategies, and high consumer footfall across urban and semi urban regions.

Regional Insights

- Italy was the leading country in the Europe chestnut market and accounted for a substantial share in 2025. The country’s dominance is supported by favorable agro climatic conditions for chestnut cultivation, strong domestic consumption, and a well established processing industry.

- Other European countries also contribute significantly, supported by traditional culinary practices, expanding retail infrastructure, and increasing demand for value added chestnut products across Western and Southern Europe.

Competitive Landscape

The Europe chestnut market is moderately fragmented, with the presence of regional producers and specialized processing companies. Market participants focus on product quality, seasonal supply chain management, and expansion into value added chestnut products such as flour, puree, and frozen formats. Companies are also strengthening retail partnerships and enhancing export capabilities to expand their footprint across European markets. Prominent players in the Europe chestnut market include SECA SUD, Blife Srl, Concept Fruits, Brusco, Sagi Srl, MASTROGREGORI ALDO SRL, Fratelli Castellino S.r.l., Agroaguiar, Sortegel, Monsurgel, Alcido Nunes, and De Marchi Srl.

Europe Chestnut Market Size

The Europe chestnut market size was valued at USD 1.08 billion in 2025 and is projected to reach USD 1.49 billion by 2034 from USD 1.12 billion in 2026, growing at a CAGR of 3.65%.

A chestnut is defined as a large deciduous tree belonging to the genus Castanea or the edible nut that it produces. Following a period of expansion that reached a recent high, the total land area used for European chestnut cultivation has begun to contract slightly. Despite the prominence of a few key Mediterranean countries, European agricultural output represents a niche component within the global supply chain, significantly smaller than that of major global agricultural producers. Unlike industrial crops, chestnuts are embedded in seasonal traditions and rural landscapes, particularly across Mediterranean mountainous regions. The harvested product serves both fresh and processed markets, ranging from roasted street snacks to flour for gluten-free baking, yet remains distinct due to its strong regional character and limited mechanization. Environmental and biological risks keep the European chestnut industry, a vital heritage crop, in a state of chronic, unpredictable yield instability.

MARKET DRIVERS Revival of Traditional Gastronomy and Seasonal Consumption Patterns

Chestnuts occupy a cherished place in the regional autumnal and winter culinary customs, which drives consistent seasonal demand and the growth of the Europe chestnut market. From roasted chestnuts sold at Christmas markets in Berlin to marrons glacés in French patisseries and castagnaccio in Italian villages, these traditions sustain consumer interest year after year. European industry experts highlight that deeply ingrained culinary traditions and a regional preference for artisanal food products continue to sustain the primary market for chestnut flour across Southern European territories.The European Union’s geographical indication protections, such as “Châtaigne d’Ardèche” in France and “Marrone di San Zeno” in Italy, further elevate perceived quality and command premium pricing. rESEARCH reveals a sharp surge in the retail purchase of fresh chestnuts during the late autumn and winter months, as consumer interest is heavily influenced by seasonal celebrations and cultural practices rather than nutritional considerations alone. This cultural continuity creates a resilient baseline of demand, insulating the market from short-term economic volatility and reinforcing intergenerational transmission of consumption habits.

Expansion of Health-Conscious and Plant-Based Food Trends

Chestnuts are gaining traction beyond seasonal treats as a functional food aligned with modern dietary preferences, which is among the key accelerators of the Europe chestnut market. Their low-fat, high-fiber, and gluten-free profile makes them ideal for plant-based, clean-label, and allergen-sensitive diets. Health-conscious consumers in Western Europe are increasingly viewing chestnuts as a nutritious, gluten-free, and lower-fat alternative to traditional refined carbohydrate-based snacks, driving interest in the nut for its health benefits. This shift has spurred innovation: chestnut flour is used in vegan baking, purees replace dairy in desserts, and syrups serve as natural sweeteners. In Italy and France, startups have launched chestnut-based beers and dairy-free creams, capitalizing on the ingredient’s natural sweetness and nutrient density. The European Food Safety Authority’s ongoing evaluation of health claims related to fiber and glycemic control indirectly benefits chestnut-derived products. Research emphasizes that the rising availability of processed, ready-to-eat chestnut products in retail channels is shifting the nut’s perception from a seasonal specialty to a year-round functional ingredient, enhancing its market relevance.

MARKET RESTRAINTS Devastating Impact of Chestnut Blight Disease Across Continental Europe

Chestnut blight, caused by the invasive fungus Cryphonectria parasitica, remains the most severe biological threat to European chestnut ecosystems. This impedes the growth of the Europe chestnut market. First introduced in the early 1900s, the pathogen has spread throughout all major production zones, causing lethal cankers that kill trees within three to five years. Despite their superior resistance to American varieties, European chestnuts still face significant yield losses when infected. Forest Research confirms that entire stands in the Balkans and Southern France have required costly removal and replanting. No chemical cure exists; management relies on labor-intensive sanitation pruning and biocontrol using hypovirulent strains, a method that is inconsistent across microclimates. The EU’s Plant Health Directive restricts movement of chestnut wood to limit spread, increasing compliance burdens. Critically, the disease undermines long-term investment in new orchards, especially among smallholders who lack resources for sustained phytosanitary interventions, thereby constraining supply reliability and market expansion.

Climate-Induced Stress and Declining Suitability in Core Production Zones

Climate change is eroding the agroecological viability of traditional chestnut-growing regions, which constrains the growth of the Europe chestnut market. This impact is particularly severe in Southern Europe. Chestnut trees are highly sensitive to water stress during flowering and fruit development, and prolonged droughts, now more frequent, trigger significant fruit drop and reduced kernel size. Recent research in the Mediterranean region indicates that increasing summer aridity is driving a long-term decline in the growth and resilience of forest ecosystems. Climate models indicate a substantial reduction in habitat suitability for forest species across Southern Europe, with projections showing a major contraction of suitable areas in Spain, Italy, and Greece due to accelerating climate change. The extreme heatwave of 2003, which caused widespread chestnut mortality in the Alps, exemplifies future risks. These stresses exacerbate soil erosion on steep slopes and increase vulnerability to secondary pests like the chestnut weevil. MDPI’s review emphasizes that warming and erratic rainfall are accelerating the abandonment of marginal orchards, especially where irrigation is absent. The decline in farming succession, driven by unpredictable yields, poses a serious threat to the demographic stability of the agricultural sector.

MARKET OPPORTUNITIES Diversification into High-Value Processed and Functional Food Products

Transforming raw chestnuts into value-added products offers a strategic pathway to enhance profitability and extend market reach beyond the harvest season, which is expected to boost the growth of the Europe chestnut market. Innovations now enable shelf-stable purees, flours, syrups, and dairy alternatives that align with clean-label and plant-based trends. Artisanal producers in France and Italy have successfully commercialized chestnut beer and gluten-free baking mixes, targeting premium niches. Industry assessments indicate that the European chestnut flour segment is poised for substantial growth through 2035, driven by demand from vegan and allergen-sensitive consumers. Value addition also mitichestnut post-harvest losses, which can be significant for perishable fresh nuts. The EU’s Farm to Fork Strategy supports such circular economy models, incentivizing investments in cold-chain logistics and gentle drying technologies. Eurostat notes that rural development funds under the Common Agricultural Policy increasingly support non-wood forest product processing in depopulated mountain areas. Producers can boost margins and lower fresh-market volatility risk by pivoting from bulk commodities to branded, story-driven products that highlight health and sustainability.

Integration of Chestnut Agroforestry into Carbon Farming and Biodiversity Schemes

Traditional chestnut agroforestry systems deliver significant ecosystem services that align with the EU’s environmental policy agenda, which offers fresh prospects for the expansion of the Europe chestnut market. These multifunctional landscapes sequester carbon, support pollinators, prevent soil erosion, and conserve native genetic diversity. Under the EU’s Carbon Removal Certification Framework and revised Common Agricultural Policy, landowners may soon receive payments for verified carbon sequestration and biodiversity outcomes. Well-managed, high-density chestnut plantations are capable of storing a significant volume of carbon dioxide in their biomass and soil over several decades, providing a carbon sequestration capacity comparable to that of established mixed deciduous forests. The European Green Deal promotes such nature-based solutions in regions at risk of desertification. Pilot projects demonstrate that integrating chestnuts with livestock grazing or legume understories improves soil health without compromising yields. FAO emphasizes that Europe dominates global trade in non-wood forest products, giving it a strategic edge in marketing chestnuts as part of certified sustainable landscapes. This paradigm shift, from crop to ecosystem service provider, opens access to green finance, eco-certification premiums, and public-private conservation partnerships, creating a novel revenue stream independent of conventional market forces.

MARKET CHALLENGES Labor Shortages and Rising Costs of Manual Harvesting

Chestnut harvesting remains overwhelmingly manual due to the spiny burrs and rugged terrain of traditional orchards, which inhibits the growth of the Europe chestnut market. Consequently, this makes mechanization impractical. Each autumn, producers require daily labor to collect fallen nuts before spoilage or wildlife predation occurs. However, rural depopulation and competition from other agricultural sectors have drastically reduced available workers. In Italy’s Piedmont region, farm associations report a significant, sustained decline in available harvesters over the past decade, resulting in a substantial portion of the chestnut crop remaining uncollected. Wages for skilled pickers have risen consistently on an annual basis in France and Spain, placing severe financial pressure on the margins of smallholder farmers. Agricultural census data indicates that the average age of chestnut farmers is high, with few younger generations willing to undertake the physically demanding, manual labor required for the harvest. Robotic harvesting remains experimental and cost-prohibitive for fragmented landholdings. Failure to invest in collaborative labor, ergonomic tools, and seasonal, targeted programs will result in continued,, supply disruptions and deter new talent, threatening the industry’s stability.

Fragmented Supply Chains and Lack of Standardized Quality Grading

A lack of harmonized quality standards and a fragmented supply chain lead to inefficiencies and post-harvest losses, which slow down the expansion of the European chestnut market. Unlike major horticultural commodities, chestnuts are traded under inconsistent national or informal criteria, resulting in variable sizing, moisture levels, and pest contamination. Cross-border transactions between Spain, France, and Italy often involve batch inconsistencies that increase sorting costs and waste. Inadequate cold chain infrastructure and logistical delays in developing markets lead to significant, high-percentage spoilage of fresh produce after harvesting. The absence of a unified traceability system hampers certification for origin, organic status, or blight-free provenance, weakening Europe’s competitiveness against standardized imports from South Korea or Turkey. The European Union has increased its reliance on non-EU suppliers for chestnuts to address shortages caused by declining domestic production quality. The market will continue to struggle with inefficiency and volatility until partners standardize European grading, invest in temperature-controlled logistics, and adopt advanced digital traceability.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

3.65%

Segments Covered

By Product Type, Application, Distribution Channel, End Use, and Region

Various Analyses Covered

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

SECA SUD, Blife Srl, Concept Fruits, Brusco, Sagi Srl, MASTROGREGORI ALDO SRL, Fratelli Castellino S.r.l., Agroaguiar, Sortegel, Monsurgel, Alcido Nunes, and De Marchi Srl

SEGMENTAL ANALYSIS By Product Type Insights

The fresh chestnuts segment dominated the Europe chestnut market in 2025. The dominance of the segment is driven by deep-seated cultural consumption patterns, where fresh chestnuts are a seasonal staple during autumn and winter festivities across Southern and Western Europe. According to research, fresh chestnuts account for the overwhelming majority of volume-based consumption, driven by their use in traditional roasting, home cooking, and local market sales. The segment’s leadership is not merely a function of volume but also of its role as the primary raw material for all other processed forms. Its position is further reinforced by consumer preference for minimally processed, natural foods, especially in rural and peri-urban communities where chestnut harvesting is part of local heritage. The immediacy of demand during the harvest season, coupled with limited shelf life, creates a high-turnover, high-visibility market that anchors the entire sector.

The chestnut flour segment is predicted to witness the highest CAGR of 7.8% percent from 2026 to 2034 due to its unique functional properties as a gluten-free, nutrient-dense, and naturally sweet alternative to conventional flours. The rise of plant-based and allergen-sensitive diets has created a robust demand for versatile ingredients that align with clean-label trends, and chestnut flour fits this profile precisely. The European chestnut flour market is experiencing growth driven by rising demand for gluten-free, healthy alternative ingredients, with baking and confectionery applications forming a significant portion of its usage. Artisanal bakeries in France and Italy are increasingly incorporating it into premium pastries, while health food manufacturers are using it in protein bars, pancake mixes, and dairy-free desserts. The European Union’s Farm to Fork strategy, which promotes diversification of non-wheat cereals, provides additional policy tailwinds. Unlike fresh chestnuts, flour offers year-round commercial viability, reduced post-harvest losses, and access to global e-commerce channels, making it an attractive investment for processors seeking to modernize the traditional chestnut value chain.

By Application Insights

The food industry application segment led the Europe chestnut market in 2025. The leading position of the segment is attributed to the foundational role chestnuts play in European gastronomy, particularly in Mediterranean countries where they are integral to regional identity. This broad category encompasses everything from fresh retail sales to industrial use in ready meals, sauces, and side dishes, reflecting the nut’s versatility as a culinary ingredient. The food industry’s scale, distribution networks, and ability to absorb seasonal harvests make it the primary outlet for chestnut producers. While confectionery is a significant sub-segment, the wider food industry, including both residential and commercial kitchens, drives the bulk of demand through consistent, large-volume procurement. This segment benefits from low barriers to entry for small-scale processors and strong alignment with existing supply chains for fresh produce, ensuring its continued primacy.

The confectionery application segment is estimated to register the fastest CAGR of 7.8% due to the premiumization of traditional sweets, such as marrons glacés, Mont Blanc desserts, and chestnut cream fillings, which command high margins in luxury and gourmet markets. Consumer willingness to pay for artisanal, heritage-based treats has surged, especially in urban centers where experiential consumption is valued. Furthermore, the natural sweetness and smooth texture of chestnut puree make it an ideal substitute for refined sugar and dairy in vegan and organic confectionery, a niche that is expanding rapidly. The rising consumer demand for premium, gluten-free, and nutrient-dense ingredients has solidified baking and confectionery applications as the primary driver for chestnut flour consumption in 2025, heavily influencing the overall processed chestnut market. This segment’s growth is also amplified by tourism, as confectionery items serve as popular edible souvenirs, creating a stable export-oriented revenue stream that is less susceptible to domestic economic fluctuations.

By Distribution Channel Insights

The supermarkets segment held the majority share of the Europe chestnut market in 2025. Their extensive reach, established cold-chain logistics, and ability to offer both fresh and packaged products make them the primary point of sale for the average consumer. During the peak season, major supermarket chains in France, Italy, and Spain dedicate prominent shelf space to fresh chestnuts, often sourced from local cooperatives, which reinforces their image as a seasonal, authentic product. This channel’s dominance is supported by its capacity to handle the high volume and perishable nature of fresh chestnuts, providing a reliable and efficient route to market that smaller channels cannot match. For end use, the residential segment is the clear leader, as the vast majority of chestnut consumption occurs in private households for cooking, roasting, or baking, driven by long-standing cultural traditions rather than commercial or industrial applications.

The online retail distribution segment is anticipated to witness the fastest CAGR during the forecast period owing to the digitalization of food shopping and the rise of direct-to-consumer models. Consumers are increasingly purchasing specialty and gourmet food items online, including chestnut flour, vacuum-packed peeled chestnuts, and artisanal confectionery, which are well-suited for e-commerce due to their longer shelf life and premium positioning. This channel allows small producers from remote chestnut-growing regions to bypass traditional intermediaries and access a pan-European customer base, often at higher margins. The growth is further accelerated by the proliferation of online platforms dedicated to organic, local, and sustainable foods, which align perfectly with the chestnut’s narrative as a heritage, eco-friendly crop. The rise of digital connectivity across Europe is accelerating the shift toward online purchasing, with processed, branded chestnuts gaining significant market share.

REGIONAL ANALYSIS Italy Chestnut Market Analysis

Italy was the top performer in the European chestnut market and accounted for a substantial share in 2025. The dominance of the Italian market is driven by its position of being both a leading producer and the dominant exporter within the EU. Italy maintained its position as the dominant exporter of European Union chestnuts in 2024, commanding a significant majority of both total shipment volume and value, with a disproportionately high share of value indicating a specialized focus on premium market segments. The country’s production is centered in regions like Tuscany and Piedmont, which are renowned for their Marroni, a protected designation of origin chestnut variety prized for its large size and sweet flavor. This emphasis on quality over quantity has allowed Italian producers to command premium prices in both domestic and international markets. The market status in Italy is characterized by a blend of traditional orchard management and modern processing, with a strong focus on value-added products like flour and confectionery. Government support for agri-food heritage and geographical indications has been instrumental in maintaining this competitive edge, ensuring that Italian chestnuts remain synonymous with excellence in the European marketplace.

Spain Chestnut Market Analysis

Spain was the next prominent country in the Europe chestnut market in 2025. In 2024, Spain became a leading producer by volume in Europe, despite challenging climatic conditions causing low productivity across the region. Along with Italy and Greece, Spain contributed a major share of the significantly reduced total European chestnut harvest, which continues to struggle to meet rising local demand. The market in Spain is primarily fuelled by extensive chestnut forests in regions like Galicia and Extremadura, where the crop is often integrated into silvopastoral systems. This large-scale production supports a robust domestic market and provides a substantial raw material base for the processing industry. However, a significant challenge lies in the prevalence of chestnut blight, which affects yield consistency and quality. Despite this, Spain’s market status is one of volume leadership, with its production playing a critical role in stabilizing the overall European supply. The focus is gradually shifting towards improving quality standards and developing more resilient varieties to enhance its position beyond just tonnage, aiming to capture more value from its considerable output.

France Chestnut Market Analysis

France occupies a significant position in the Europe chestnut market due to its strong cultural attachment to the product and its leadership in premium, terroir-driven offerings. Despite lower production volumes compared to European rivals, French truffles are revered for their exceptional quality. The market is also dominated by protected geographical indications such as “Châtaigne d’Ardèche,” which guarantees origin and traditional cultivation methods, allowing French chestnuts to command some of the highest prices in Europe. The market status in France is characterized by a vibrant network of local festivals, farmers markets, and artisanal producers who have successfully linked chestnut consumption to national and regional identity. This cultural capital translates into a resilient and loyal consumer base, insulating the French market from price volatility. Government initiatives further demonstrate a commitment to preserving this heritage crop and supporting its future through research and promotion.

Greece Chestnut Market Analysis

Greece is a lucrative region in the European chestnut market by securing its place among the top producers on the continent. Following a peak in the previous year, European chestnut production experienced a significant decline in 2024, with Spain, Italy, and Greece continuing to dominate as the leading producers in the region. The market in Greece is mainly centered in mountainous regions like Eurytania and Aetolia-Acarnania, where chestnut cultivation is a vital part of the rural economy and a key tool for preventing land abandonment. The market status is one of steady expansion, supported by a favorable climate and a growing recognition of the chestnut’s economic potential. Greek producers are increasingly focusing on organic certification and sustainable forestry practices, aligning with broader European consumer trends. Despite the current prevalence of selling fresh nuts in regional markets, an emerging, promising movement toward value-added processing, such as flour and liqueur production, is poised to strengthen the sector’s profitability and resilience in the coming years.

Portugal Chestnut Market Analysis

Portugal is predicted to expand in the Europe chestnut market during the forecast period. It is known for its high-quality output and strong export orientation. The country is a major exporter of chestnuts, ranking third globally, which shows its integration into international trade flows. Portuguese chestnuts, particularly those from the Trás-os-Montes region, are celebrated for their flavor and are a key component of the nation’s gastronomic identity. The market status in Portugal reflects a balance between tradition and modernization, with many orchards managed using centuries-old techniques while simultaneously adopting new technologies to combat threats like chestnut blight. The sector is a crucial source of income for the country’s interior, where it helps maintain population and economic activity in otherwise depopulated areas. Government and EU rural development funds have been instrumental in supporting this sector, funding projects for replanting with blight-resistant varieties and improving post-harvest handling. This strategic support, combined with a strong export focus, ensures that Portugal remains a key and dynamic player in the European chestnut market.

COMPETITIVE LANDSCAPE

The Europe chestnut market is characterized by a fragmented yet dynamic competitive landscape where small and medium-sized enterprises dominate alongside a few specialized regional leaders. Competition is not primarily price driven but rather based on product quality, geographical origin, and adherence to traditional or organic practices. Italian French and Spanish producers hold distinct advantages through protected designations of origin which create strong brand equity and consumer loyalty. The absence of large multinational corporations allows for niche differentiation but also limits economies of scale. New entrants face significant barriers including biotic threats like chestnut blight climate vulnerability and labor-intensive harvesting. However competition is intensifying in the value-added segment where innovation in processing and packaging is enabling companies to reach broader audiences. Strategic focus on sustainability storytelling and digital sales channels is reshaping how players compete beyond local markets. This environment fosters collaboration among cooperatives while encouraging individual brands to invest in traceability and premium positioning to stand out in an increasingly discerning marketplace.

KEY MARKET PLAYERS

Some of the notable key players in the Europe chestnut market are

- SECA SUD

- Blife Srl

- Concept Fruits

- Brusco

- Sagi Srl

- MASTROGREGORI ALDO SRL

- Fratelli Castellino S.r.l.

- Agroaguiar

- Sortegel

- Monsurgel

- Alcido Nunes

- De Marchi Srl

Top Players in the Market

- Based in Italy, Società Agricola Castellaro Srl is a leading producer and processor of high-quality chestnuts, particularly known for its certified IGP Marrone di San Zeno. The company operates extensive orchards in the Veneto region and specializes in both fresh and value-added products such as peeled vacuum-packed chestnuts and flour. It has strengthened its market position by investing in sustainable harvesting techniques and cold-chain logistics to extend shelf life. Recently, the company launched an e-commerce platform targeting health-conscious consumers across Europe, enhancing direct access to premium chestnut products and reinforcing its brand as a guardian of Italian chestnut heritage.

- Headquartered in France, Marrons de la Drôme is a key player in the European chestnut sector, renowned for its PDO-certified Châtaigne d’Ardèche. The company integrates traditional cultivation with modern processing, offering a range of products from fresh chestnuts to confectionery-grade purees. To solidify its presence, it recently partnered with major organic food retailers in Germany and Belgium, expanding its distribution beyond Southern Europe. Additionally, the firm has implemented traceability systems using QR codes on packaging, allowing consumers to verify origin and farming practices, thereby aligning with growing demand for transparency and sustainability in agri-food supply chains.

- Operating from Spain, Castañas del Noroeste SL is a prominent exporter and processor specializing in Galician chestnuts. The company manages a vertically integrated supply chain, from forest management to packaging, ensuring consistent quality for both domestic and international markets. It has recently upgraded its processing facility with automated sorting and peeling technology to reduce labor dependency and post-harvest losses. Its strategic focus on innovation and export readiness has significantly enhanced its global footprint, particularly in Northern and Central Europe.

Top Strategies Used by the Key Market Participants

Key players in the Europe chestnut market are pursuing vertical integration to control quality from orchard to consumer. They are investing in blight-resistant chestnut varieties to secure long-term supply stability. Companies are expanding into value-added processing such as flour and purees to capture higher margins. Strategic partnerships with organic and gourmet retailers are being formed to access premium urban markets. Digital transformation through e-commerce platforms and traceability technologies is being adopted to enhance consumer trust and direct sales. Geographic diversification of distribution channels beyond traditional Southern Europe is underway. Emphasis on geographical indication certifications is used to differentiate products and justify premium pricing. Sustainability initiatives including carbon farming and agroforestry models are being promoted to align with EU green policies. Collaborative research with agricultural institutes is supporting innovation in harvesting and storage. Brand storytelling centered on heritage and terroir is leveraged to build emotional consumer connections.

MARKET SEGMENTATION

This research report on the European chestnut market has been segmented and sub-segmented based on categories.

By Product Type

- Fresh Chestnuts

- Roasted Chestnuts

- Dried Chestnuts

- Chestnut Flour

By Application

- Food Industry

- Confectionery

- Cosmetics

- Pharmaceuticals

By Distribution Channel

- Online Retail

- Supermarkets

- Specialty Stores

- Wholesale

By End Use

- Residential

- Commercial

- Industrial

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe