E

Eurofast

More

Eurofast is a regional business advisory organisation employing local advisers in over 21 cities in South East Europe, Middle East & the Baltics. The Organisation is uniquely positioned as one stop shop for investors and companies looking for professional services.

Residents are subject to personal income tax on their worldwide income. Non-residents are taxed on their Serbian-source income only. Income tax is assessed in the year, in which the income is earned on a current year basis.

Serbia

Tax

To print this article, all you need is to be registered or login on Mondaq.com.

Article Insights

Eurofast ’s articles from Eurofast are most popular:

- within Tax topic(s)

- with Senior Company Executives, HR and Finance and Tax Executives

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- in Europe

- with readers working within the Metals & Mining industries

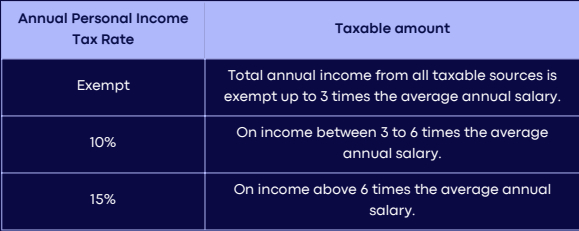

1. Individuals

1.1 Personal Income Tax

Residents are subject to personal income tax on their worldwide

income. Non-residents are taxed on their Serbian-source income

only. Income tax is assessed in the year, in which the income is

earned on a current year basis.

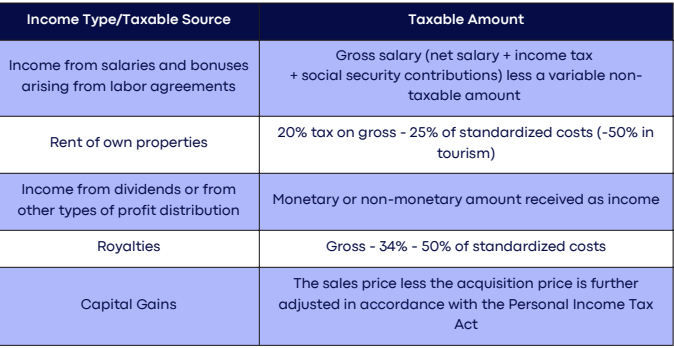

1.1.2 Taxable Income

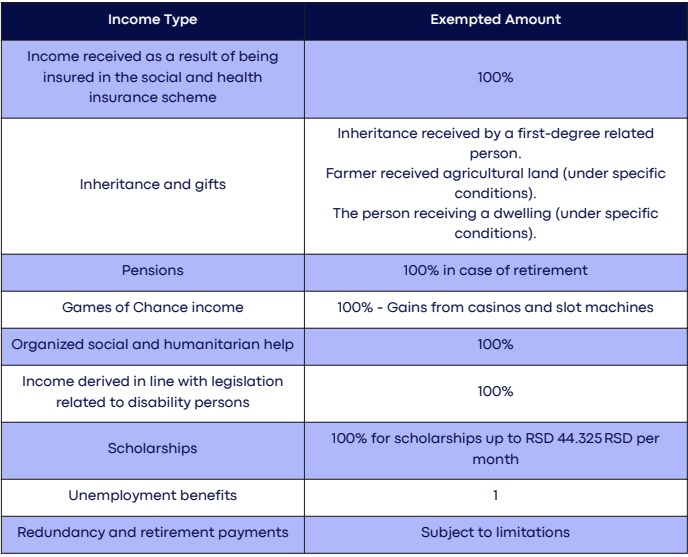

1.1.3 Exempt Income

Additionally, the following are the non-taxable amounts of

payments/benefits done by the employer:

- Daily allowance for business trips in the country – up to

RSD 3.471 (approx. EUR 29) per day - Daily allowance for business trips abroad – up to 90

EUR. - Business trip transportation cost – up to 10.121 RSD

(approx. EUR 85) Public transportation cost for going to and coming

from work – up to RSD 5.782 (approx. EUR 49) - Compensation for use of own vehicle for a business trip –

30% of the cost of 1L of gasoline per km of trip. - Remuneration for accommodation and meal expenses on a business

trip – must be justified by bills and is fully

non-taxable. - Severance pay at time of retirement – either prescribed

by the Company Act or two-fold average monthly salary (Labor Law

prescribed). - Redundancy severance pay – 1/3 of salary for each year of

employment with the employer making the payment. - Compensation for expenses of burial of employee, his/ her

spouse or child – RSD 101.194 (approx. EUR 857) - Solidarity bonus – in case of the death of an employee or

member of his family or of a company retiree – RSD 101.194

(approx. EUR 857) - Solidarity bonus in case of long or serious illness,

rehabilitation, or disability – RSD 57.827 (approx. EUR 490)

Solidarity bonus for the abatement of consequences of flood or

other acts of god or in other extraordinary circumstances – Can be

determined on a case-by-case basis and often depends on the extent

of the actual damage and the decision of the authority providing

the assistance. - Anniversary reward – RSD 28.912 (approx. EUR 245)

- Loan for the purchase of heating material, school books, and

winter supply of pickled vegetables and fruit preserves. - Christmas gifts for children of employees up to 15 years of age

14.457 (approx. EUR 122) - Scholarships for pupils and students – up to RSD 44.325

per month (approx. EUR 375) - Additional health insurance and retirement plan premiums

– RSD 8.677 (approx. EUR 73) per month

These are the valid amounts as of February 1st 2026 until

January 31st 2027.

1.1.4 Deductible Expenses

Expenses are non-deductible for personal income tax

purposes.

1.1.5 Allowances

Personal deduction for the purpose of the annual personal income

tax equal to 40% of the average annual salary is automatically

deducted. Additional allowance equal to 15% of the average annual

salary may be claimed for each dependent family member. The total

amount of the allowances may not exceed 50% of the aggregate

taxable income.

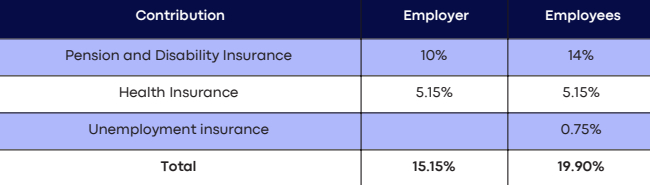

1.2 Social Security and Health Insurance

Contributions

Contribution rates are as follows:

1.3 Submission of Tax Returns

The deadline for the submission and payment of tax returns

varies depending on the income type and the income payer.

The deadline for submission of annual personal income tax

returns for income generated in 2025 is 15 May 2026.

Tax return is submitted electronically on the Tax

Authority’s portal and the instruction for payment is

automatically generated.

To view the full article clickhere

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.