Posts Q4 Loss That Challenges Bullish Margin Narratives")

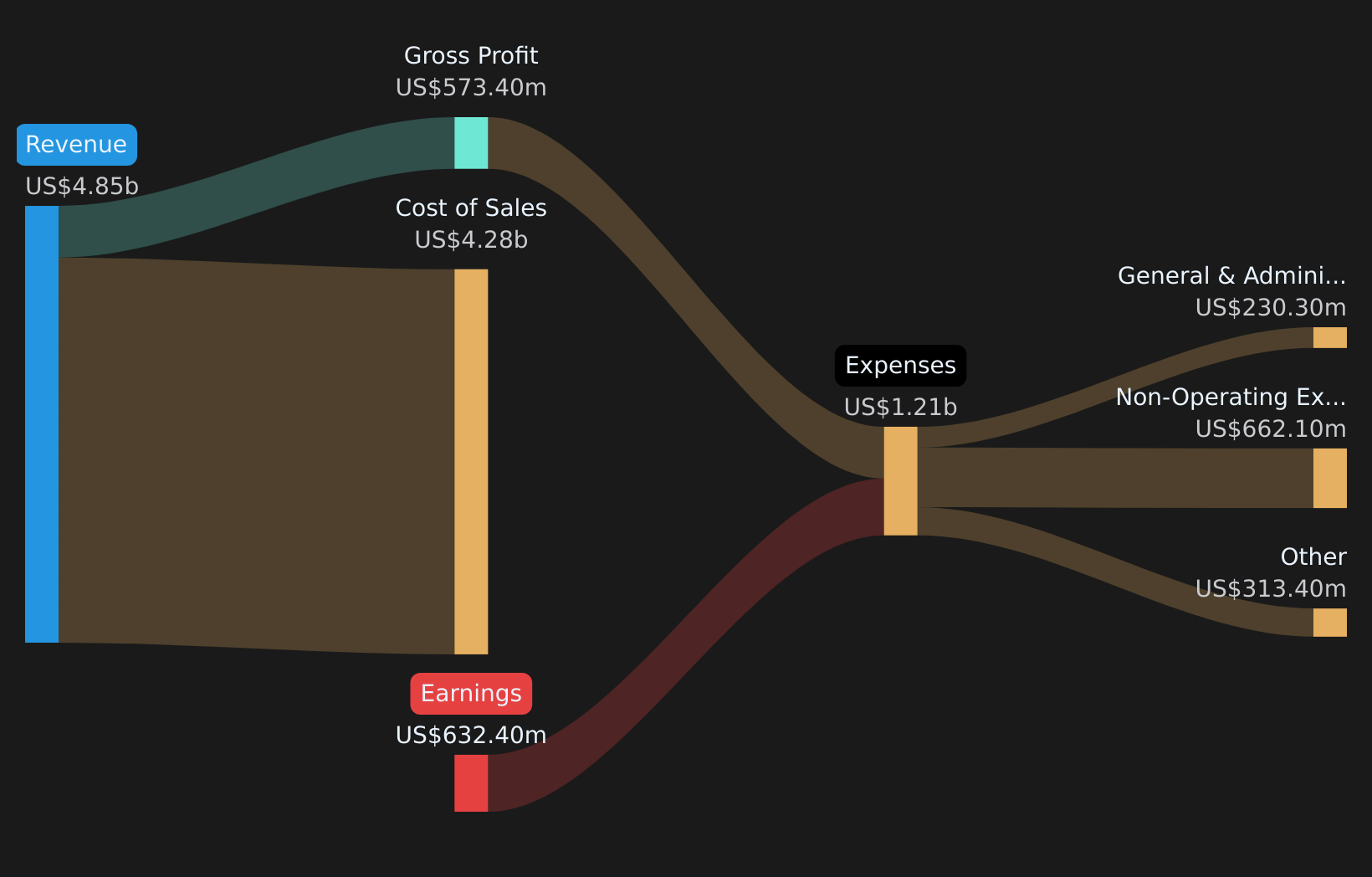

AMC Entertainment Holdings (AMC) just posted its FY 2025 numbers with Q4 revenue of US$1,288.3 million, a basic EPS loss of US$0.25, and net income excluding extra items showing a loss of US$127.4 million, while trailing 12 month figures sit at US$4.8 billion of revenue, a basic EPS loss of US$1.34, and a net loss of US$632.4 million. Over recent quarters, the company has seen quarterly revenue move from US$862.5 million in Q1 2025 to between roughly US$1.3 billion and US$1.4 billion through Q2 to Q4. EPS losses have ranged from US$0.01 to US$0.58 per share, which puts the current release squarely in focus for how you view the trade off between scale and ongoing losses. Margins remain under pressure, so this set of results is really about how much risk you are willing to accept for a business that is still loss making at this revenue level.

See our full analysis for AMC Entertainment Holdings.

With the latest figures on the table, the next step is to see how these margins and recurring losses line up against the dominant stories around AMC, and where the hard numbers push back on those narratives.

See what the community is saying about AMC Entertainment Holdings

- On a trailing 12 month basis, AMC generated US$4.8b of revenue and recorded a net loss of US$632.4 million, with a basic EPS loss of US$1.34.

- Bulls point to higher guest spending and premium formats as future margin drivers. However, the current loss profile sets a high bar for that view:

- Revenue growth of about 6.4% a year trails the wider US market’s 10.3%, even as premium formats and subscription programs are expected by optimistic investors to support stronger long term growth.

- Bullish narratives talk about margin expansion and earnings reaching positive territory over time. The latest year still shows hundreds of millions of dollars in losses, so any margin story has to work from a clearly loss making base.

If you are trying to see how bullish investors join the dots between premium formats, subscriptions, and these losses, 🐂 AMC Entertainment Holdings Bull CaseLow P/S vs peers, high capital structure risk

- AMC trades on a P/S of 0.1x compared with 1.8x for peers and 1.3x for the US entertainment industry, while carrying the major balance sheet risk of negative shareholders’ equity.

- Bears argue that high debt, negative equity, and ongoing dilution matter more than a cheap sales multiple. The trailing numbers give that concern some weight:

- The company is unprofitable over the last 12 months and is not expected to be profitable over the next three years, so debt and equity holders are currently being paid with hopes of future improvement rather than current earnings.

- Recent shareholder dilution, combined with negative equity, means any future recovery in earnings would be spread over a larger share base, which is exactly the kind of trade off cautious investors focus on.

If you are weighing that low P/S against the debt load and negative equity, 🐻 AMC Entertainment Holdings Bear CaseQuarterly swings show operating leverage at work

- Across FY 2025, AMC’s quarterly revenue moved between US$862.5 million and US$1.4b, while net income excluding extra items ranged from a loss of US$4.7 million in Q2 to losses of US$298.2 million in Q3.

- Analysts’ consensus narrative talks about premium experiences and content diversification supporting more stable, incremental revenue. The recent pattern underlines how sensitive earnings still are to revenue and cost mix:

- The swing from a small Q2 loss of US$4.7 million to a Q3 loss of US$298.2 million came alongside only a modest revenue move from US$1.4b to US$1.3b, which is a clear sign of strong operating leverage in both directions.

- Even with box office and alternative content helping revenue, margins remain negative across all reported quarters, so the story of loyalty programs and premium formats has not yet translated into consistent profitability in the financials.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for AMC Entertainment Holdings on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

If this mix of risks and potential rewards feels finely balanced, now is a good time to review the numbers yourself and decide where you stand. You can start with 1 key reward and 3 important warning signs.

See What Else Is Out There

AMC is still loss making on US$4.8b in revenue, carries negative shareholders’ equity, and shows earnings that swing sharply with relatively small revenue shifts.

If that mix of ongoing losses and a fragile balance sheet feels too tense, you might want to check companies in our solid balance sheet and fundamentals stocks screener (42 results) that aim for stronger financial footing and steadier returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com