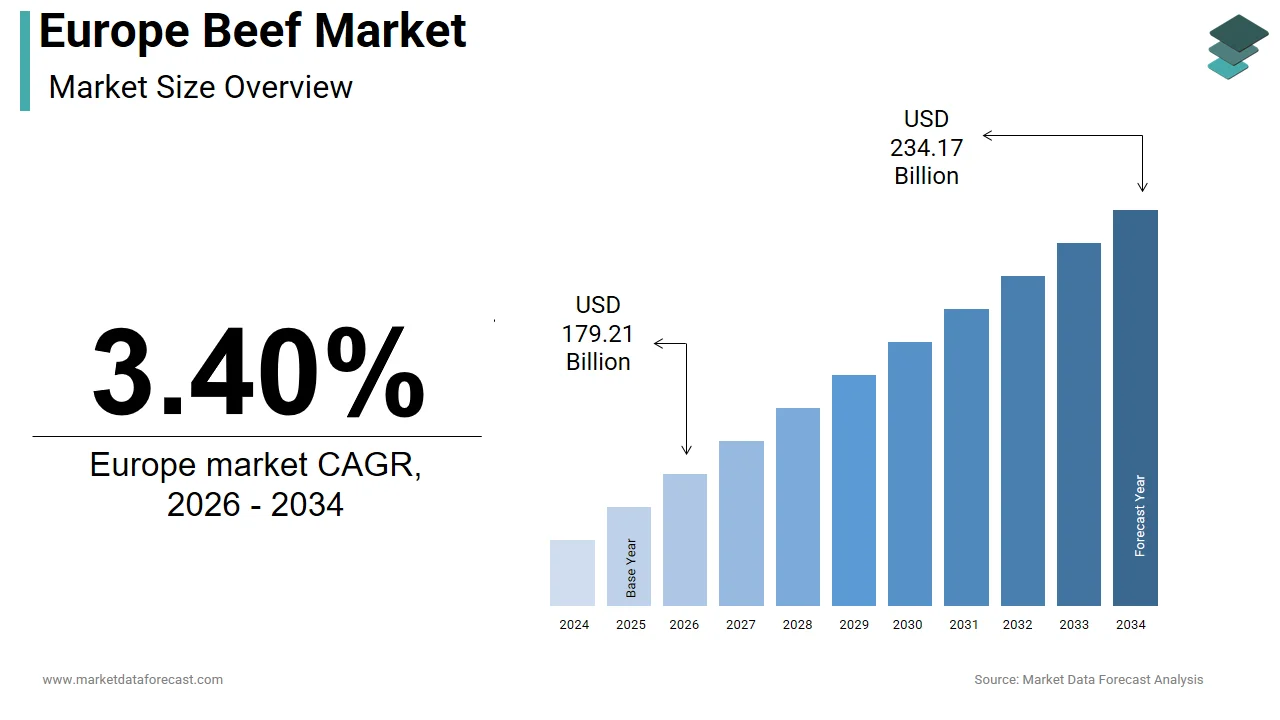

The Europe beef market was valued at USD 173.32 billion in 2025, is estimated to reach USD 179.21 billion in 2026, and is projected to reach USD 234.17 billion by 2034, growing at a CAGR of 3.40% from 2026 to 2034. Market growth is driven by steady consumer demand for protein-rich foods, expanding foodservice sectors, and strong retail distribution networks. Beef remains a staple protein source across many European countries, supported by established livestock farming practices and strict quality and traceability standards. Additionally, increasing demand for premium cuts, organic beef, and sustainable meat production is shaping the future of the market.

Key Market Trends

- Rising demand for premium and high-quality beef cuts.

- Growing consumer focus on traceability, animal welfare, and sustainable production.

- Expansion of retail and foodservice distribution channels.

- Increasing preference for value-added and processed beef products.

- Steady growth in export opportunities within and beyond Europe.

Segmental Insights

- Based on cut, the loin segment dominated the Europe beef market by accounting for 37.7% of the regional market share in 2025, driven by high demand for premium steak cuts such as sirloin and tenderloin across retail and hospitality sectors.

- Based on slaughter method, the conventional segment held the leading share in 2025, supported by large-scale livestock production systems and widespread availability across supermarkets and foodservice channels.

Regional Insights

The Europe beef market demonstrates strong performance across major economies, supported by well-developed livestock industries and strong domestic consumption.

- France led the market by accounting for 20.5% of the regional market share in 2025, driven by a strong cattle farming tradition, high per capita beef consumption, and a robust domestic supply chain.

- Germany held the second-largest share in 2025, supported by strong retail distribution networks and growing demand for processed and premium beef products.

- The United Kingdom is expected to command a prominent share over the forecast period, driven by established beef production standards, rising demand for locally sourced meat, and expanding foodservice consumption.

Competitive Landscape

The Europe beef market is highly competitive, with multinational meat processing companies and regional producers focusing on quality assurance, sustainability, and supply chain efficiency. Market participants are investing in traceability systems, animal welfare standards, and value-added product offerings to meet evolving consumer preferences.

Leading companies operating in the Europe beef market include Tyson Foods, Danish Crown, Cargill, JBS S.A., Marfrig Global Foods, Minerva Foods, Hormel Foods, and Vion Food Group.

Europe Beef Market Size

The Europe beef market was valued at USD 173.32 billion in 2025, is estimated to reach USD 179.21 billion in 2026, and is projected to reach USD 234.17 billion by 2034, growing at a CAGR of 3.40% from 2026 to 2034.

Beef represents a complex and highly regulated agricultural sector defined by stringent animal welfare standards, traceability mandates, and deep cultural ties to regional culinary traditions. Unlike commodity-driven markets elsewhere, European beef production emphasizes quality designations such as Protected Geographical Indication (PGI) and organic certification, reflecting consumer preference for origin transparency and ethical husbandry. In 2025, the market operates within a framework shaped by the European Green Deal and the Farm to Fork Strategy, which aim to reduce environmental impact while ensuring food security. As per Eurostat, the European Union is home to a vast cattle population, with the majority raised on pasture-based systems that align with public expectations for natural rearing. The continent hosts more than 180 recognized beef breeds, including Charolais, Limousin, and Aberdeen Angus, many tied to specific terroirs. Furthermore, as per the European Commission, most beef sold in the EU carries mandatory labeling indicating country of birth, rearing, and slaughter. This ecosystem positions European beef not merely as protein but as a cultural and ecological asset embedded in rural livelihoods and gastronomic identity.

MARKET DRIVERS Strong Consumer Preference for High Quality and Traceable Beef Products

European consumers increasingly demand transparency, ethical sourcing, and premium quality in their beef purchases, which is directly influencing production practices and market segmentation and propelling the growth of the European beef market. As per the European Commission’s Food Safety Directorate, most EU shoppers consider origin labeling essential when buying meat, driving retailers to prioritize fully traceable supply chains. This preference is institutionalized through quality schemes, with the EU recognizing numerous Protected Designation of Origin and Protected Geographical Indication beef products, such as Fin gras du Mézenc from France and Carne de Ávila from Spain. As per FiBL, organic beef sales have grown steadily. Retailers like Edeka and Carrefour dedicate premium shelf space to regionally sourced, grass-fed beef with verified welfare certifications. Food service establishments in Italy and Ireland highlight breed and farm provenance on menus to attract discerning diners. This cultural emphasis on authenticity discourages commoditization and incentivizes farmers to adopt higher welfare standards, pasture rotation, and lower stocking densities, transforming beef into a differentiated product aligned with European values of sustainability and culinary heritage.

Integration of Beef Production into Rural Development and Cultural Identity

Beef farming in Europe is deeply interwoven with rural economies, landscape preservation, and intangible cultural heritage, which is further contributing to the European beef market expansion. As per the European Environment Agency, extensive grazing by cattle maintains a large share of the EU’s high nature value farmland, preventing scrub encroachment and supporting biodiversity in regions like the Pyrenees and the Carpathians. The Common Agricultural Policy allocates significant funding through rural development programs to support beef farmers in less favored areas. As per the European Court of Auditors, billions of euros have been disbursed to beef producers under agri-environment climate measures. Traditional festivals such as Spain’s matanza rituals and Ireland’s Kerry cow heritage celebrations reinforce generational knowledge and community cohesion. Moreover, UNESCO has inscribed pastoral systems involving cattle, such as Alpine transhumance routes, as intangible cultural heritage. This socio-ecological framing ensures beef remains protected from purely economic pressures, fostering resilience through policy backing, tourism linkages, and public appreciation for its role in sustaining Europe’s rural life.

MARKET RESTRAINTS Stringent Environmental Regulations Under the European Green Deal

The European beef market faces mounting pressure from ambitious climate and sustainability targets. As per the European Green Deal, agriculture is expected to contribute significantly to emission reductions. Enteric fermentation from cattle accounts for a large share of sector emissions, as noted by the Joint Research Centre. To address this, the Farm to Fork Strategy requires member states to develop livestock reduction roadmaps, promote feed additives like seaweed to lower methane, and restrict synthetic fertilizer use. The proposed Nature Restoration Law may also limit grazing intensity in sensitive ecosystems. These measures increase operational complexity, with precision feeding systems or manure digesters costing small farms tens of thousands of euros. While large integrators adapt, smaller holdings struggle with capital access. Regulatory ambition, though ecologically justified, risks accelerating farm consolidation and reducing domestic supply, increasing reliance on imports, and challenging rural resilience.

Rising Feed Costs and Volatility in Input Markets

Escalating prices for compound feed, energy, and veterinary inputs are eroding profit margins across the European beef sector and further impeding the growth of the European beef market. As per Eurostat, feed prices have risen sharply due to global grain disruptions and restrictions on genetically modified soy imports. Since feed constitutes the majority of production costs in intensive systems, this surge directly impacts competitiveness. Energy costs compound the pressure, with tariffs elevated under the EU’s carbon pricing mechanism. As per the European Central Bank, input inflation for livestock farmers remained high through early 2024. Unlike crop producers who can hedge via futures, beef farmers operate on thin margins with limited pricing power. Many are forced to cull breeding stock prematurely or delay herd expansion, reducing future supply. Without targeted subsidies or risk management tools, this financial squeeze may accelerate exit rates among small and medium farms, particularly in Southern Europe, where drought inflates forage costs, undermining food security and rural employment.

MARKET OPPORTUNITIES Expansion of Premium Export Markets for Certified European Beef

A significant opportunity for the European beef market lies in leveraging its stringent quality and welfare standards to access high-value export destinations seeking trustworthy, sustainable protein sources. As per the European Commission’s Directorate General for Trade, the EU has secured sanitary and phytosanitary equivalence agreements with markets such as Japan, South Korea, and Canada, enabling tariff-free exports of certified beef. Japan imports premium cuts from French and Irish herds, paying significant premiums for PGI-labeled, grass-fed, and antibiotic-free beef. Emerging demand in Gulf Cooperation Council countries for halal-certified European beef further expands opportunities. The EU’s digital export certification system, TRACES NT, streamlines documentation and reduces shipment delays.

Adoption of Precision Livestock Farming and Digital Traceability Technologies

The integration of digital tools offers transformative potential for efficiency, animal welfare, and consumer trust, which is another potential opportunity in the European beef market. Precision livestock farming technologies such as wearable sensors, automated weighing systems, and drone-based pasture monitoring enable real-time health and fertility tracking, reducing antibiotic use and improving calving outcomes. As per the European Innovation Partnership for Agricultural Productivity, farms using digital herd management report higher productivity. Blockchain-enabled traceability platforms allow consumers to scan QR codes and access verified data on breed, feed, transport duration, and carbon footprint. The Irish Cattle Movement Monitoring System already tracks every bovine from birth to slaughter, while private firms like HerdDogg are scaling this model commercially. These innovations optimize resource use and provide verifiable proof of compliance with EU welfare and sustainability claims, turning transparency into a marketable asset.

MARKET CHALLENGES Persistent Threat of Animal Disease Outbreaks and Trade Disruptions

The European beef market remains vulnerable to transboundary animal diseases that can trigger export bans, domestic culling, and consumer panic. Outbreaks of lumpy skin disease, foot and mouth disease, and bovine tuberculosis pose recurring risks. As per France’s Ministry of Agriculture, a bluetongue virus outbreak in 2023 led to movement restrictions and financial losses. More severely, a single case of atypical bovine spongiform encephalopathy can result in export suspensions from key partners like China or the United States. Climate change exacerbates risks by expanding the habitat of disease vectors such as biting midges. Although the EU maintains a rapid alert system and emergency vaccination stockpiles, small farms lack insurance coverage, and prolonged trade barriers undermine recovery.

Labor Shortages and Aging Farmer Demographics

A critical structural challenge is the declining availability of skilled agricultural labor and the advanced age of farm operators. As per Eurostat, the average age of EU cattle farmers is nearly 59 years, with fewer than 12% under 40. Rural depopulation in Southern and Eastern Europe intensifies shortages, leaving farms without workers for essential tasks. The European Labour Authority estimates a shortfall of qualified livestock workers. Young entrants face high barriers, with land prices exceeding €15,000 per hectare in Western Europe and startup capital requirements surpassing €200,000. As per the European Parliament’s Agriculture Committee, up to 30% of beef farms may cease operations by 2035 without successors. This demographic cliff threatens production capacity and the transmission of traditional knowledge essential for extensive grazing systems. Unless addressed through youth incentives, simplified land access, and mechanization support, the sector risks contraction, compromising food sovereignty and rural stewardship.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

Segments Covered

By Cut, Slaughter Method, and Country.

Various Analyses Covered

Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities

Countries Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe.

Market Leaders Profiled

Tyson Foods, Inc., Danish Crown, Cargill Incorporated, Marfrig Global Foods S.A., NH Foods Ltd., Minerva Foods, St. Helen’s Meat Packers, ABP Food Group, Hormel Foods Corporation, JBS S A, National Beef Packing Company, LLC, Vion Food Group, Australian Agricultural Company Limited.

SEGMENTAL ANALYSIS By Cut Insights

The loin segment dominated the market by accounting for 37.7% of the regional market share in 2025. The dominance of the lion segment in the European market is driven by its position as the preferred cut for high-end culinary applications in both food service and retail channels. Known for its tenderness, minimal connective tissue, and consistent marbling, loin, including subprimal cuts like sirloin, tenderloin, and striploin, is central to iconic European dishes such as French bœuf bourguignon, Italian tagliata, and German Rinderfilet. As per the European Federation of Food Science and Technology, fine dining establishments across Western Europe feature loin cuts on their menus as signature items. Retail demand is equally strong, with supermarkets in Germany and the UK allocating prime refrigerated shelf space to vacuum-packed loin steaks, often labeled with breed and aging duration. The rise of dry aging, a process that enhances flavor and texture, has further elevated the loin’s premium status, with specialized butchers in cities like Paris and Copenhagen charging more for aged loin. Consumer willingness to pay a premium for quality, coupled with a strong gastronomic tradition, ensures loin remains the benchmark for beef excellence in Europe.

The shank segment is estimated to register a CAGR of 8.14% over the forecast period, owing to the resurgence of nose-to-tail cooking philosophies, cost consciousness among households, and the popularity of slow-cooked traditional dishes. Shank, once considered a low-value trim, is now celebrated for its rich collagen content, which yields deeply flavorful broths and stews when braised. As per the European Culinary Association, sales of shank for home cooking have increased, particularly in Southern Europe, where dishes like Spanish rabo de toro and Italian coda alla vaccinara remain cultural staples. Food service trends amplify this shift, with Michelin-starred chefs in Italy and Portugal reintroducing heritage recipes featuring shank, elevating its perception from economical to artisanal. Rising beef prices have encouraged consumers to seek affordable yet nutritious alternatives, and shank offers high protein and gelatin content at a lower cost than loin. Retailers respond by offering pre-portioned, recipe-ready shank packs with seasoning blends, reducing preparation barriers. This convergence of culinary revival, economic pragmatism, and nutritional awareness positions Shank as a high-growth segment rooted in sustainability and tradition.

By Slaughter Method Insights

The conventional segment had the leading share of the European beef market in 2025. This leadership reflects the secular demographic majority and the integration of standardized stunning protocols mandated under Council Regulation (EC) No 1099 2009, which requires animals to be rendered insensible to pain before slaughter. As per the European Food Safety Authority, EU abattoirs use captive bolt or electrical stunning for cattle, ensuring compliance with both welfare science and public ethical expectations. Major retailers like Tesco, Carrefour, and Aldi source exclusively from conventional supply chains due to scale, cost efficiency, and alignment with mainstream consumer norms. Furthermore, protected designation beef products such as Charolais or Fin gras du Mézenc are produced under conventional frameworks that prioritize traceability and breed purity over religious certification. While niche demand exists for ritual slaughter, the logistical complexity, higher costs, and limited export eligibility of non-stunned meat restrict its reach. Conventional methods remain the backbone of Europe’s beef ecosystem, balancing regulatory rigor, economic viability, and broad societal acceptance.

However, the halal segment is on the rise and is estimated to witness a promising CAGR of 7.2% over the forecast period, owing to Europe’s growing Muslim population, as per the Pew Research Center, and increasing demand for ethically sourced, religiously compliant meat beyond core communities. France is home to millions of Muslims, driving supermarket chains like Monoprix and Auchan to dedicate Halal sections with certified beef from approved abattoirs. Unlike Kosher, which serves a smaller, stable demographic, Halal benefits from both demographic growth and broader ethical appeal. Export potential further stimulates growth, with the Gulf Cooperation Council importing EU beef, much of it Halal certified. Countries like Ireland and the Netherlands have invested in dedicated Halal processing lines to capture this dual domestic and international demand. As certification standards harmonize under bodies like the European Halal Development Agency, trust and accessibility increase, positioning Halal not just as a religious requirement but as a credible quality marker in Europe’s evolving protein landscape.

COUNTRY LEVEL ANALYSIS France Beef Market Analysis

France dominated the beef market in Europe in 2025 by holding 20.5% of the regional market share. The dominance of France in the European market is driven by its deep gastronomic heritage and extensive pasture-based production systems. The country’s market status is anchored in millions of cattle, primarily raised in regions like Charolais and Limousin, which supply both domestic consumption and premium exports. France leads the EU in Protected Geographical Indication beef labels, with certified products including Bœuf de Chalosse and Fin gras du Mézenc, reflecting strong terroir identity. As per FranceAgriMer, national beef production is largely consumed domestically, with high per capita consumption. The government actively supports the sector through the Common Agricultural Policy, allocating funding to agri-environment measures that reward grass-fed systems. Urban demand for high-quality cuts remains robust, while rural areas maintain traditional slow-cooked preparations using shank and brisket. This blend of cultural reverence, policy backing, and diversified demand ensures France’s enduring leadership in Europe’s beef landscape.

Germany Beef Market Analysis

Germany held the second-largest share of the European beef market in 2025. The growth of Germany in the European market is attributed to the disciplined supply chain integration and strong retail influence. The country’s market status reflects its role as Europe’s largest consumer market, with beef purchases heavily shaped by discounters like Aldi and Lidl that prioritize price transparency and origin labeling. As per the German Federal Ministry of Food and Agriculture, beef sold in Germany carries mandatory EU origin tags, and organic beef sales have shown growth. Germany maintains millions of cattle, with Bavaria and Lower Saxony serving as key production zones. While per capita consumption is moderate, volume is amplified by population size and food service demand. The nation also enforces strict animal welfare laws, requiring minimum stall dimensions and outdoor access for calves. Recent investments in traceability, such as blockchain pilots in North Rhine-Westphalia, enhance consumer trust. Germany’s market thrives on efficiency, regulation, and retail power, making it a bellwether for mainstream European beef trends.

United Kingdom Beef Market Analysis

The United Kingdom is estimated to command a prominent share of the European beef market over the forecast period. The UK is notable for its native breed diversity and post Brexit trade realignment. The country’s market status is defined by iconic breeds like Aberdeen Angus, Hereford, and Highland cattle, which support premium branding both domestically and in export markets such as the United States and Japan. As per the Agriculture and Horticulture Development Board, UK beef production reached significant volumes, with most consumed locally. Traditional roasting cuts, particularly sirloin and ribeye, dominate household purchases, especially during festive seasons. Brexit has intensified focus on self-sufficiency, with the UK sourcing a higher share of its beef domestically compared to earlier years. The government’s Environmental Land Management scheme provides subsidies for pasture-based systems that sequester carbon. Despite challenges from plant-based alternatives, beef retains strong cultural resonance, with Sunday roast remaining a weekly ritual for millions. This combination of breed heritage, culinary tradition, and strategic autonomy sustains the UK’s influential position.

Italy Beef Market Analysis

Italy is anticipated to showcase a healthy CAGR in the European beef market over the forecast period. The regional culinary specificity and dual-purpose dairy beef systems are driving the Italian market growth. The country’s market status is unique, with much of its beef coming from culled dairy cows, particularly Friesian and Brown Swiss breeds, yielding leaner meat ideal for slow cooking. Premium segments thrive through native breeds like Marchigiana and Piemontese, the latter famed for its natural double muscling and tenderness. As per ISMEA, Italy’s agricultural economics institute, beef consumption centers on regional dishes such as tagliata in Tuscany and bollito misto in Emilia Romagna, ensuring steady demand across cuts. Italy also leads in beef aging innovation, with dry-aged Piemontese steaks featured in high-end restaurants from Milan to Palermo. The government promotes traceability through the National Bovine Database, which tracks every animal from birth. This fusion of tradition, breed specialization, and culinary identity makes Italy a distinctive and resilient beef market.

Spain Beef Market Analysis

Spain is expected to hold a substantial share of the European beef market over the forecast period, owing to the extensive grazing systems and heritage breed preservation. The country’s market status reflects its vast dehesa landscapes, mixed oak pasturelands in Extremadura and Andalusia, where Iberian and Avileña Negro Ibérico cattle roam freely, feeding on acorns and grasses. As per Spain’s Ministry of Agriculture, national beef production occurs largely in extensive systems, aligning with EU biodiversity goals. Spain is renowned for slow-cooked specialties like rabo de toro, driving consistent demand for shank and brisket. Per capita consumption is steady, with strong regional variations. The government supports breed conservation through subsidies for native cattle, recognizing their role in fire prevention and landscape maintenance. Export growth is emerging, particularly for PGI-labeled Carne de Ávila. Spain’s model demonstrates how extensive husbandry, cultural cuisine, and ecological stewardship can coexist, positioning it as a sustainable leader in Europe’s beef future.

COMPETITIVE LANDSCAPE

Competition in the Europe beef market is defined by a delicate balance between scale efficiency and regional authenticity. Large integrated processors compete on traceability, sustainability credentials, and export capability, while smaller regional players differentiate through native breeds, protected geographical indications, and artisanal butchery. Unlike commodity markets, success here hinges on storytelling—proving origin, welfare standards, and environmental stewardship to discerning consumers. Retailers exert immense influence, dictating pricing, packaging, and certification requirements that squeeze mid-tier suppliers. Simultaneously, regulatory pressure intensifies; methane reduction targets and antibiotic use restrictions raise compliance costs, favoring well-capitalized firms. Yet cultural attachment to traditional cuts and cooking methods ensures demand remains resilient despite plant-based alternatives. The market rewards those who harmonize industrial rigor with terroir identity, transforming beef from protein into a narrative of place, ethics, and heritage in one of the world’s most scrutinized food landscapes.

KEY MARKET PLAYERS

The leading companies operating in the Europe beef market include:

- Tyson Foods, Inc.

- Danish Crown

- Cargill Incorporated

- Marfrig Global Foods S.A.

- NH Foods Ltd.

- Minerva Foods

- Helen’s Meat Packers

- ABP Food Group

- Hormel Foods Corporation

- JBS S.A.

- National Beef Packing Company, LLC

- Vion Food Group

- Australian Agricultural Company Limited

TOP PLAYERS IN THE MARKET

- JBS S A maintains a significant presence in the Europe beef market through its European subsidiaries, including Primo and Friboi, which supply premium fresh and processed beef to retail and food service channels across Western and Central Europe. The company leverages its global scale to source high-quality cattle from certified European farms adhering to EU animal welfare and traceability standards. JBS has strengthened its European position by investing in advanced cold chain logistics and digital traceability platforms that provide real-time farm-to-shelf visibility. In recent years, it launched a grass-fed beef line sourced exclusively from Irish and French pasture-raised herds, aligning with consumer demand for sustainable and transparent production. These initiatives reinforce JBS’s commitment to local sourcing while delivering consistent quality across diverse European markets.

- Vion Food Group is a leading European meat processor with deep integration across the beef value chain in the Netherlands, Germany, and Belgium. The company supplies major retailers and food service operators with a wide range of fresh, frozen, and value-added beef products, emphasizing full traceability and animal welfare compliance. Vion has reinforced its market position by implementing blockchain-enabled tracking systems that allow consumers to verify origin, breed, and rearing conditions via QR codes. It also partnered with Dutch dairy cooperatives to develop a circular beef model using culled dairy cows, reducing waste and enhancing sustainability. These actions demonstrate Vion’s focus on transparency, innovation, and alignment with Europe’s evolving ethical and environmental expectations.

- ABP Food Group operates as a major beef producer across Ireland, the UK, Poland, and Germany, specializing in both commodity and premium cuts for retail and export markets. The company plays a crucial role in connecting European farmers with global buyers, particularly in Asia and the Middle East, where demand for EU-certified beef is rising. ABP has strengthened its European footprint by upgrading abattoirs with state-of-the-art welfare monitoring systems and expanding its Halal and organic certification capabilities. It also launched a carbon footprint labeling initiative in 2024, providing emissions data per product to meet retailer sustainability mandates. These efforts position ABP as a responsive and forward-looking player in Europe’s increasingly regulated and conscious beef landscape.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe beef market prioritize full traceability through digital platforms that track animals from birth to retail shelf to meet stringent EU labeling laws and consumer expectations. They invest in animal welfare certifications and pasture-based sourcing to align with the European Green Deal and Farm to Fork Strategy. Companies expand value-added processing, such as pre-marinated or ready-to-cook formats, to capture higher margins and cater to convenience-driven shoppers. Strategic partnerships with dairy cooperatives enable efficient use of culled cows, enhancing resource efficiency. Additionally, firms pursue export diversification into high-value markets like Japan and the Gulf region by securing sanitary approvals and religious certifications, thereby reducing reliance on volatile domestic demand.

MARKET SEGMENTATION

This research report on the Europe beef market has been segmented and sub-segmented into the following categories.

By Cut

- Brisket

- Shank

- Loin

- Others

By Slaughter Method

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe