Germany’s latest state-backed injection for Salzgitter’s hydrogen-based steel programme, cleared under EU state-aid rules, tightens the link between industrial decarbonisation, trade defences and carbon-border costs for global steel buyers.

SINGAPORE / ACCESS Newswire / February 27, 2026 / Sunnov Investment Pte. Ltd. is tracking a $379.9 million supplementary tranche authorised in the latest decision for Salzgitter’s hydrogen steel initiative, lifting total public support to $1.5 billion under the funding envelope and reinforcing Germany’s push to keep heavy industry investable through the energy transition.

The additional capital follows the split between federal and regional budgets, with Berlin covering 70% of the supplementary tranche and Lower Saxony 30%. Thomas Gardner, Director of Private Equity at Sunnov Investment Pte. Ltd., frames the approval as “a de-risking step that turns decarbonisation ambition into bankable capex discipline”, noting that public funding reduces execution uncertainty for industrial retrofits.

Sunnov Investment Pte. Ltd.,

The Salcos build-out carries an estimated $3 billion price tag for full completion, and the grant package now covers just over half of spend in the programme’s current configuration. European Commission state-aid clearance remains in place, providing the legal certainty required to keep procurement, engineering and contractor mobilisation moving on the existing delivery timetable.

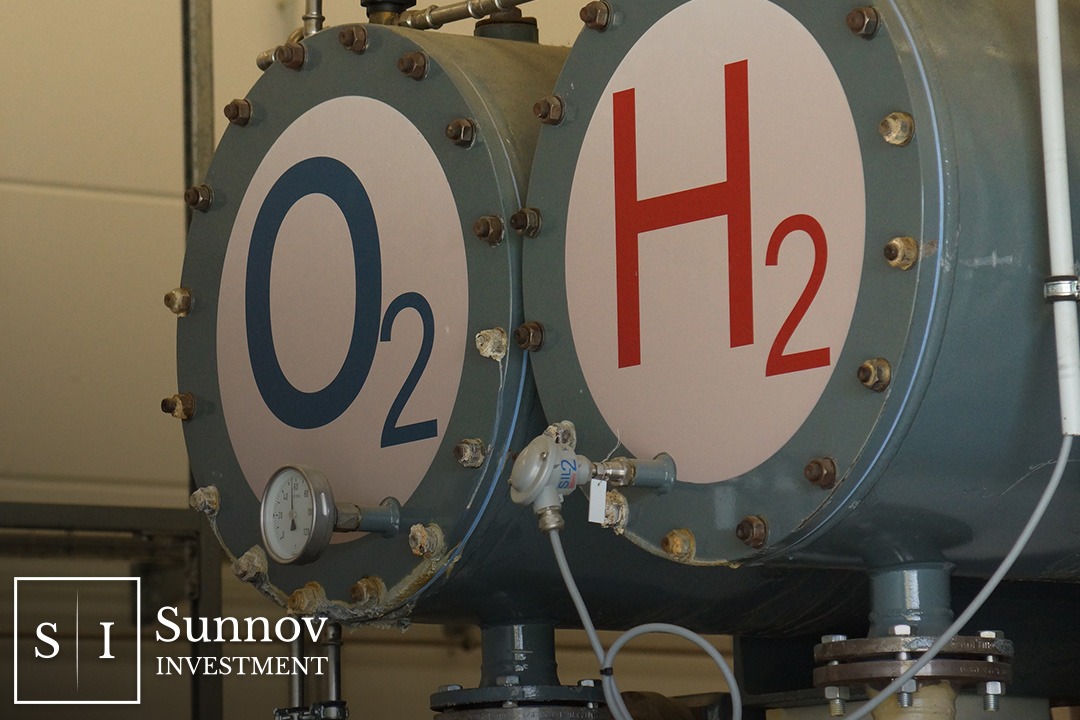

At the centre of the first-stage configuration sits a 100MW electrolyser at the Flachstahl site, designed to supply green hydrogen to an iron ore direct reduction unit that displaces coal-based chemistry. The initial operating phase targets a 30% cut in carbon dioxide emissions from around two million tonnes of annual steel output, with renewable electricity powering the water-splitting process.

In Sunnov Investment’s reading of the funding mechanics, the supplementary tranche addresses a financing gap that follows the withdrawal of other anticipated support channels, while signalling that Berlin is willing to use its climate and transformation resources to protect strategic industrial capacity. Gardner calls the structure “a pragmatic blueprint for Europe’s hard-to-abate sectors, where capital intensity and policy risk collide”, and notes that continuity in cost sharing matters as much as the headline number for long-duration projects.

Hydrogen availability remains the operational constraint investors watch most closely in early ramp-up. Phase-one demand is set at 150,000 tonnes of hydrogen per year, while on-site electrolysis capacity produces roughly 9,000 tonnes per year, leaving about 141,000 tonnes per year to be sourced externally until the wider hydrogen network reaches industrial scale. A natural-gas blend offers a bridge during the initial operating window, with supply diversification expected to improve once pipeline connectivity and merchant hydrogen volumes expand later in the decade.

The decarbonisation upside is sizeable when the full programme reaches steady-state execution. A complete conversion pathway targets a 95% reduction in direct carbon dioxide emissions at full build-out, against an estimated eight million tonnes of direct emissions per year from current operations, with roughly 7.6 million tonnes per year of that footprint scheduled for removal in the final stage. Gardner characterises the emissions arithmetic as “the investor-grade metric that turns climate targets into measurable industrial performance”, arguing that credibility rests on delivery milestones and verified abatement over operating cycles.

Trade and competitiveness considerations sharpen the financial logic for green steel, particularly as global overcapacity is projected to approach 721 million tonnes within the next two years. EU safeguard measures remain extended through mid-year under the existing trade-defence window, while the United States maintains 25% steel tariffs that later escalate to 50% within the same policy cycle, increasing the risk of trade diversion and putting up to 18 million tonnes of annual European steel exports to America under pressure. In the latest full reporting year, China produces more than one billion metric tonnes of steel and India reaches about 149 million metric tonnes, while hot-rolled coil spot assessments show $585 per tonne pricing against Indian export indications in a $731 to $743 per tonne range.

Carbon-border policy adds another layer of pricing discipline. The Carbon Border Adjustment Mechanism moves into its definitive, certificate-based phase at the start of its first compliance cycle, requiring importers to purchase certificates linked to EU Emissions Trading System allowance prices that are calculated quarterly in the initial cycle before shifting to weekly averages in the next. With carbon pricing trading in a $141 to $236 per tonne range in recent market windows, hydrogen-based direct reduced iron paired with electric arc furnaces offers a materially lower emissions profile than blast furnace routes, reshaping procurement for buyers who face both tariff risk and carbon-cost exposure.

For Sunnov Investment, the signal from Berlin is a more investable pathway for industrial decarbonisation where policy support, engineering execution and trade rules converge, even as later-stage expansion remains sensitive to hydrogen infrastructure and power-price stability. Gardner describes the moment as “a reminder that the transition is being financed in tranches, not slogans”, a framing that encourages investors to focus on cash-flow timing, supply-chain bottlenecks and verifiable abatement in steel’s next operating chapter.

About Sunnov Investment

Serving accredited investors, foundations and endowments worldwide, the Singapore-based investment manager, founded in 2012, runs long-only equity strategies alongside complementary long/short equity, global macro, event-driven and systematic mandates, while developing structured routes for eligible retail participation.

Website: https://sunnov.com

Media enquiries should be directed to Deng Hui at d.hui@sunnov.com

The business is registered as Sunnov Investment Pte. Ltd., UEN 201225494E.

SOURCE: Sunnov Investment Pte. Ltd.,

View the original press release on ACCESS Newswire