Narrative")

- In late February 2026, Diamondback Energy reported a very large US$3.65 billion impairment, a fourth-quarter 2025 net loss, and updated 2026 production guidance alongside a higher base dividend and continued buybacks.

- The company paired this accounting hit with strong capital returns and an expanded Barnett Shale program, signaling an emphasis on long-term resource depth and shareholder payouts despite near-term earnings pressure.

- We’ll now examine how the Barnett Shale expansion and continued capital returns affect Diamondback Energy’s existing investment narrative.

We’ve uncovered the 15 dividend fortresses yielding 5%+ that don’t just survive market storms, but thrive in them.

Diamondback Energy Investment Narrative Recap

To own Diamondback Energy today, you need to be comfortable with a Permian-focused producer that is pairing heavy non-cash impairments and a Q4 2025 net loss with continued high production, disciplined capex, and sizable cash returns. The key near term catalyst remains execution on its 2026 production and capex plan, while the biggest risk is that weaker commodity prices could strain free cash flow and pressure dividends and buybacks. The latest impairment and guidance do not materially change that near term setup.

Against this backdrop, the decision to lift the base dividend to US$1.05 per share, alongside ongoing buybacks that have retired nearly 19% of the share count since 2021, is particularly relevant. It reinforces that management is prioritizing capital returns even as impairments weigh on reported earnings, tying the current news to the longer running catalyst of FANG’s commitment to return at least half of adjusted free cash flow to shareholders through dividends and repurchases.

But investors should also be aware that if oil prices weaken and free cash flow tightens, the sustainability of these elevated capital returns could…

Read the full narrative on Diamondback Energy (it’s free!)

Diamondback Energy’s narrative projects $15.6 billion revenue and $4.5 billion earnings by 2028.

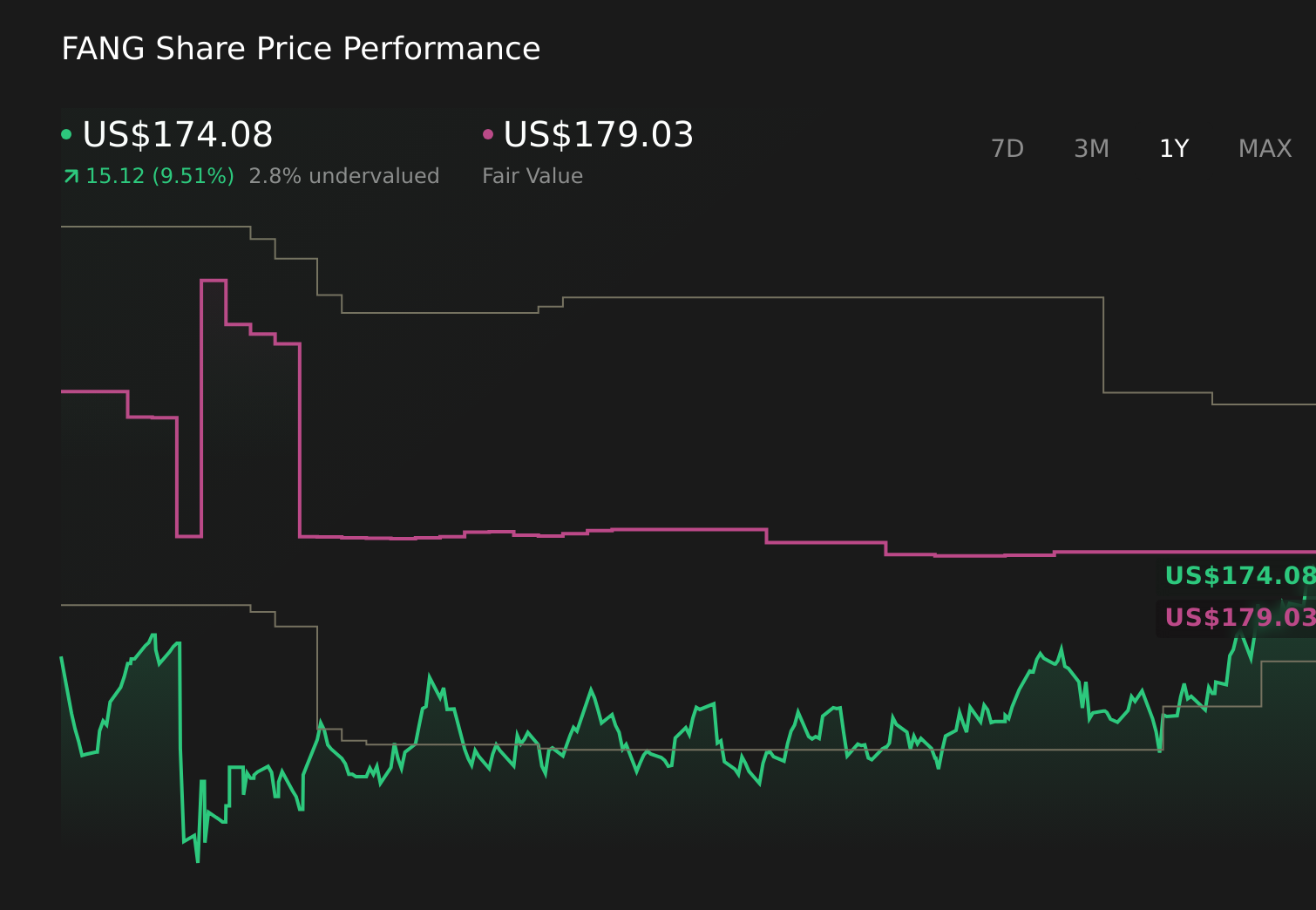

Uncover how Diamondback Energy’s forecasts yield a $179.03 fair value, a 3% upside to its current price.

Exploring Other Perspectives FANG 1-Year Stock Price Chart

FANG 1-Year Stock Price Chart

Some of the most optimistic analysts were assuming revenues near US$17.3 billion and about US$5.6 billion in earnings by 2028, which is a far more bullish story than the baseline. You can see how their view of expanding margins and heavy capital returns might be challenged or reinforced by a US$3.65 billion impairment and updated 2026 guidance, so it is worth weighing that more aggressive outlook against the concentrated Permian exposure risk before deciding which narrative you find more realistic.

Explore 6 other fair value estimates on Diamondback Energy – why the stock might be worth 9% less than the current price!

The Verdict Is Yours

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Searching For A Fresh Perspective?

The market won’t wait. These fast-moving stocks are hot now. Grab the list before they run:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com