The drop in South Korean industrial output in January doesn’t indicate weaker growth in the first quarter, as exports and investment remained strong through February. It’s likely a temporary slowdown. Yet higher oil prices and significant corrections in financial markets amid Middle East developments pose significant risks to a K-shaped recovery.

Industrial production unexpectedly contracted in January

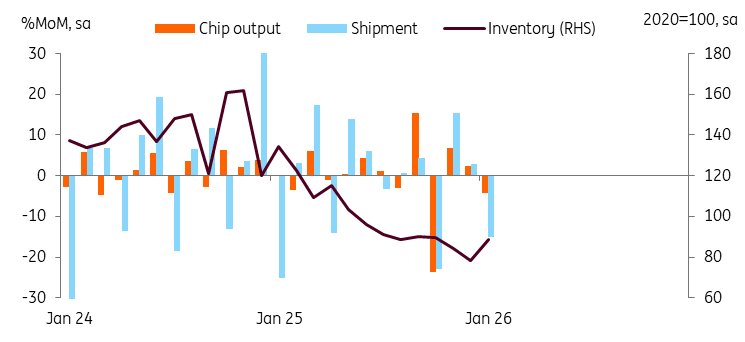

Although South Korean chip exports remained robust at the start of 2026—rising by 103% year-on-year in January and 161% in February—production actually declined. On a monthly comparison basis, chip output dropped by 4.4% month-on-month, seasonally-adjusted, in January. The discrepancy between the two data sets likely stems from strong price effects that boosted the value of chip exports, while actual production and export volumes probably remained relatively steady or declined slightly. With low inventories and a 41.1% surge in semiconductor equipment investment, we believe the decline is temporary and chip activity continues to be a main driver of growth. And while motor vehicles’ output rebounded 2.01% for the first time in three months, underlying momentum still remained weak.

Semiconductor output dropped in January, but expect to rebound

Source: CEICConstruction may remain a big drag to overall growth

All industry production dropped 1.3%, with construction down the most by 11.4%. We had expected construction activity to rebound after a five-year-long contraction. But today’s weak construction data posed downside risks to our construction outlook, especially as construction orders dropped for the second consecutive month. Meanwhile, service output remained flat. Information and communication technologies (ICT) related to software development and computer programming rose, but were fully offset by weak wholesale/retail sales.

Positive signs were found from solid Retail Sales and surge in equipment investment

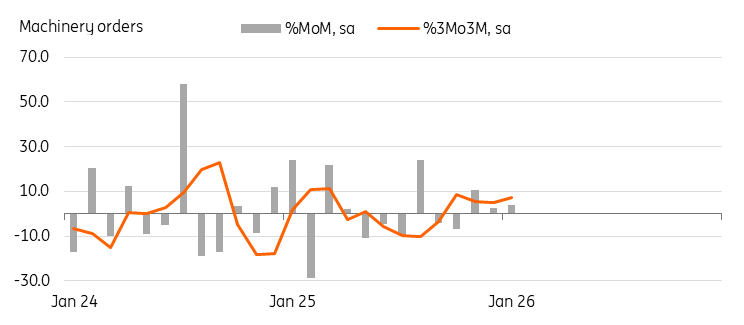

Retail sales rose 2.3% month-on-month, seasonally-adjusted, in January, following a 0.6% rise in December. Car sales dropped 3.8%, probably because government EV incentive programs haven’t resumed. Excluding car sales, other categories rose meaningfully. Equipment investment rebounded 6.8% for the first time in four months. Chip-making machinery (41.1%) and transportation equipment (15.1%) rose firmly. Today’s data support our view that private consumption and investment are likely to drive growth in 1Q26.

Machinery orders rose for three consecutive months

Source: CEIC

However, the recent developments in the Middle East posed a significant downside risk to Korean growth.

Higher Oil prices and uncertainty are negative for growth

As Korea depends heavily on external oil and gas, terms of trade should deteriorate with higher commodity prices. Yet thanks to strong exports of AI chips, ships, and machinery, the current account is expected to maintain a surplus.

The greatest risk to Korea’s economic growth may be that geopolitical uncertainty and rising oil prices, could slow AI investment globally. Since we have expected robust chip activity to drive growth, the sudden weakness of chip exports and facility investment could have a considerable negative impact. For now, we still don’t think this is a base case. However, corrections in Korean equity markets over the past two days might reduce consumer confidence and possibly spending in the near future. We are keeping our current GDP forecast of 2.2% YoY, but downside risks grew meaningfully.

The effects of rising Oil prices on Korean inflation are complex

Energy accounts for about 7.5% of the CPI basket, and a 10% change in oil prices generally increases the headline CPI by about 0.2 percentage points. Government subsidies and power companies can absorb some of these shocks. On the other hand, geopolitical risks often negatively affect the KRW, thereby amplifying upward pressure on overall import prices through currency effects. The USDKRW shot up above 1,500 overnight, but it came down to 1,480 level this morning. If USDKRW stabilises near the 1,450 level within a month, the currency impact should be limited. Taking these factors into account, along with ING’s updated global commodity outlook, we have raised our CPI forecast for 2026 from 2.0% YoY to 2.2%.

Government and BoK will focus on calming market anxiety

At this time, policymakers’ main priority should be calming market anxiety. In addition to the safe havens seeking, profit-taking and program trading may have contributed to sharp declines in local equity markets over two consecutive days. We don’t expect the current market jitters to trigger a rate cut by the BoK. Instead, while monitoring the market developments, the BoK is likely to increase market liquidity via its bond operations to stabilise the market. The government will also utilise its market stabilisation funds.

Read the original analysis: South Korean output unexpectedly declines amid growing geopolitical risks