Europe Peptide Market Size

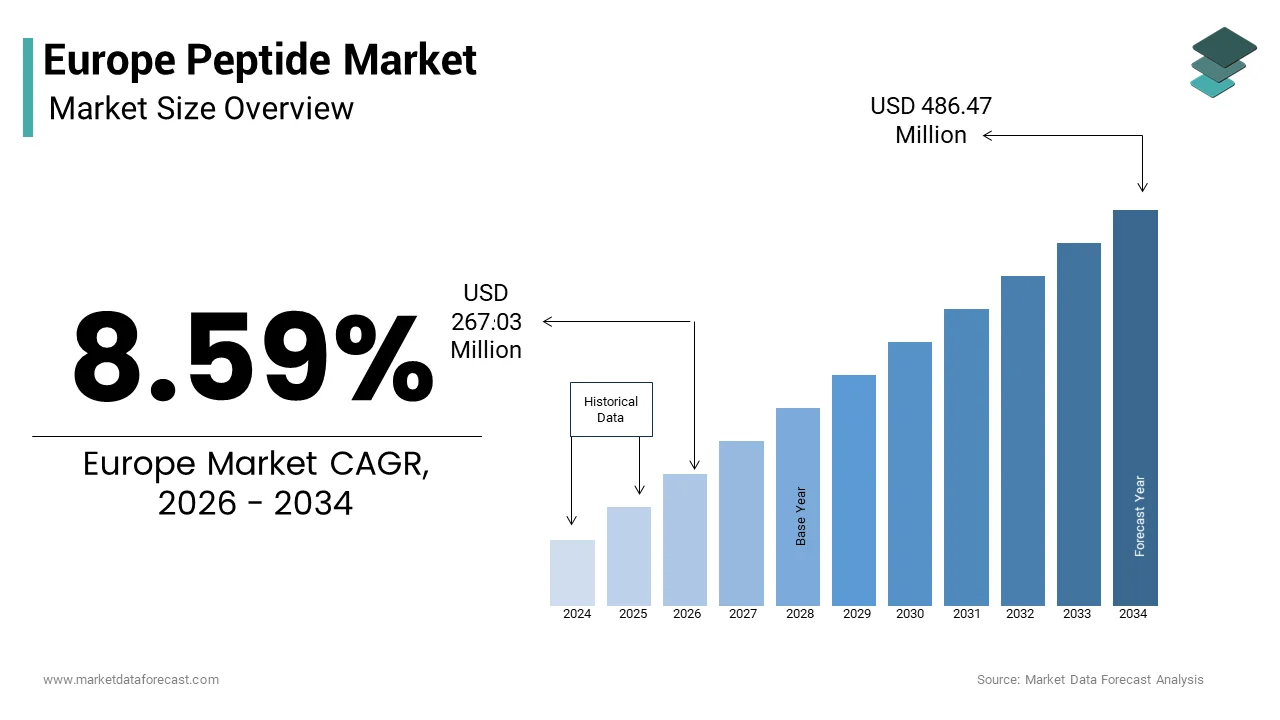

The Europe peptide market size was valued at USD 245.87 million in 2025 and is anticipated to reach USD 267.03 million in 2026 to reach from USD 486.47 million by 2034, growing at a CAGR of 8.59% during the forecast period from 2026 to 2034.

Current introduction of the Europe Peptide Market

Peptides are short chains of amino acids (the “building blocks” of proteins) linked together by chemical bonds called peptide bonds. This domain has evolved from simple synthetic processes to complex biologics manufacturing utilizing advanced recombinant DNA technologies and solid phase synthesis. The fundamental shift in therapeutic paradigms toward targeted molecular medicine defines the current landscape as traditional small molecule drugs face limitations in specificity and efficacy. The European Union is experiencing a consistent rise in the proportion of elderly residents, resulting in a larger demographic segment that frequently requires long-term, specialized healthcare management. The penetration of high level research infrastructure supports this growth. In addition, the European Commission is actively promoting the strengthening of biotechnology and biomanufacturing sectors to improve collaboration between research institutions and industry, aiming to enhance Europe’s competitive position in the global market. Regulatory frameworks shaped by the European Medicines Agency influence how these molecules are approved and monitored making compliance a central operational requirement. This market functions as a primary engine for innovation in treating metabolic disorders and cancer while enabling the cosmetics industry to develop non-invasive anti-aging solutions. The region benefits from a strong tradition of chemical engineering and pharmaceutical excellence ensuring high quality standards.

PRIMARY DEMAND DRIVERS Rising Prevalence of Chronic Metabolic Disorders Drives Therapeutic Demand

The escalating incidence of diabetes, obesity, and related metabolic syndromes is a major factor for the surge in peptide therapeutic adoption across the region and the growth of the Europe peptide market. Consequently, this growing health crisis is driving the increased use of these treatments across the continent. These conditions require highly specific treatments that peptides provide through mechanisms such as insulin mimicry and appetite regulation which small molecules cannot replicate effectively. The number of adults living with diabetes in Europe is experiencing a steady upward trajectory, which is driving an increased need for advanced therapeutic interventions. This ubiquity ensures that pharmaceutical companies prioritize peptide pipelines to address the unmet medical needs of millions of patients. The rollout of long acting peptide formulations has further accelerated this trend by improving patient compliance through reduced injection frequency. Prescription rates for GLP-1 receptor agonists in Europe are rising sharply due to their efficacy in managing both type 2 diabetes and obesity. Healthcare systems specifically capitalize on these therapies due to their ability to prevent costly complications such as cardiovascular disease and kidney failure. The shift is evident in research funding where public and private sectors allocate billions toward peptide drug discovery. As lifestyle factors continue to contribute to metabolic health issues the dependency on these biological agents becomes absolute for effective disease management. This structural change in disease burden guarantees that therapeutic demand will remain the dominant driver for market expansion.

Expansion of Biotechnological Research Infrastructure Fuels Innovation

Biotechnology hubs and research institutions form a robust network that drives primary demand and the expansion of the Europe peptide market. As a result, there is a continuous push for investment in peptide synthesis and modification technologies. Laboratories now require sophisticated platforms to design and test novel peptide sequences efficiently. This need is driven by the increasing complexity of biological targets. The European biotech landscape is growing, with a rising number of firms focusing on peptide-based therapeutics, driven by investment in peptide manufacturing capacity. This concentration of expertise fosters an environment where innovation thrives through collaboration between universities and commercial entities. The rise of contract development and manufacturing organizations has further intensified activity by providing scalable production capabilities for smaller firms lacking internal infrastructure. Public funding in the European Union supports broad life science research, including investments in drug delivery technologies and peptide stability. This cross border dynamic encourages the adoption of cutting edge techniques such as flow chemistry and enzymatic synthesis. The need for rapid prototyping ensures that equipment suppliers and reagent manufacturers experience consistent growth. Consequently, the health of the peptide market is inextricably linked to the vitality of the regional scientific ecosystem and its capacity to translate basic research into commercial applications.

CRITICAL MARKET RESTRAINTS High Manufacturing Costs and Complexity Limit Accessibility

Peptide synthesis and purification are highly intricate, which creates a major barrier for the Europe peptide market. This difficulty limits manufacturers’ capacity to match the low production costs of traditional small molecule drugs. The requirement for specialized equipment stringent quality control and complex supply chains fundamentally alters the economic landscape forcing companies to charge premium prices. As per studies, the production cost of peptide APIs remains high compared to small molecules, primarily driven by complex, low-yield synthetic processes (e.g., solid-phase peptide synthesis) and expensive raw materials. This financial pressure has led to limited availability of certain life saving treatments in healthcare systems with tight budgets. Major producers have followed suit by consolidating operations to achieve economies of scale which reduces competition and keeps prices elevated. A study found that high R&D costs, including manufacturing, present a significant barrier to commercialization for novel therapeutic modalities, with overall clinical failure rates often cited high for many drug classes. Developers now face higher barriers to entry and must invest heavily in process optimization to improve efficiency. The fragmentation of regulatory requirements across different member states adds complexity for pan European production requiring legal teams to constantly monitor compliance. These constraints reduce the overall addressable market and limit the granularity of patient access available to clinicians. The industry continues to grapple with balancing advanced therapeutic potential against the fundamental reality of high production expenses mandated by technical complexities.

Stability and Delivery Challenges Hinder Clinical Efficacy

The inherent instability of peptides in physiological environments and their poor oral bioavailability limit the expansion of the Europe peptide market. This leads to high attrition rates during clinical development and limiting administration routes. When peptides are exposed to digestive enzymes or extreme pH levels they rapidly degrade rendering them ineffective unless delivered via injection. Therapeutic peptide development is frequently hindered by limited metabolic stability and low permeability, leading to high failure rates during early clinical phases. This biological limitation leads to a reliance on invasive delivery methods which reduces patient compliance and increases the risk of infection. Large pharmaceutical companies which form the bulk of the European market fabric are particularly cautious and may deprioritize peptide programs in favor of more stable modalities. Data from various national health agencies indicates that the need for cold chain logistics further complicates distribution and increases costs significantly. The volatility makes it difficult for operators to forecast long term revenue as new delivery technologies can be introduced abruptly. Operators demand more robust formulation strategies which compresses margins and slows down time to market. Furthermore the fluctuating success rates impact the willingness of investors to fund early stage peptide ventures. This macro-biological headwind creates a cautious environment where innovation in delivery systems stagnates despite the underlying demand for non-invasive therapies.

EMERGING GROWTH OPPORTUNITIES Integration of Artificial Intelligence in Peptide Design

The rapid adoption of artificial intelligence and machine learning presents a lucrative opportunity for researchers, which is likely to promote the growth of the Europe peptide market. They can now design novel peptide sequences with enhanced stability and specificity that drive customer loyalty and lifetime value. Users today expect tailored solutions. To deliver this, AI algorithms analyze vast databases of protein structures to predict optimal amino acid arrangements instantly. According to research, artificial intelligence adoption is rapidly expanding within European life sciences as part of a strategic effort to enhance R&D efficiency, with a growing focus on AI-driven molecular modeling and drug discovery pipelines. This transition allows brands to create dynamic libraries of candidate peptides that evolve with the latest scientific insights significantly improving success rates compared to traditional trial and error models. The ability to provide instant feedback and customized design parameters enhances the relevance of research and improves outcomes for developers with varying capabilities. The adoption of smart data processing and AI-driven analytics is rising significantly across European biotech and pharmaceutical firms to enhance research, speed up drug discovery, and improve data management. Researchers are increasingly allocating portions of their technology budgets to these digital channels to capture deeper insights into structure activity relationships. The format supports adaptive testing environments that reduce anxiety and provide accurate assessments of competency bridging the gap between teaching and evaluation. As algorithms become more sophisticated the barrier to entry for high-quality personalized tutoring lowers enabling scalable solutions for mass education. This technological leap ensures that the European market remains at the forefront of educational innovation driving efficiency and effectiveness across all verticals.

Expansion of Peptide Based Cosmeceuticals

The growing consumer demand for non-invasive anti-aging solutions offers a transformative opportunity for cosmetic manufacturers to incorporate bioactive peptides into skincare formulations, which is predicted to contribute to the expansion of the Europe peptide market. These advanced ingredients help predict outcomes and automate customization without human intervention. Consumer interest in scientifically backed beauty solutions, particularly peptide-based anti-aging products, is growing in Europe as part of a broader shift toward proactive health-focused skincare. Generative data models allow for the creation of verified efficacy claims tailored to specific skin concerns such as wrinkles and loss of elasticity ensuring that each user sees the most relevant ethical options possible. This level of transparency was previously unattainable at scale and significantly boosts booking frequency among environmentally aware demographics while reducing idle time between searches. Predictive analytics help operators anticipate market trends and adjust their inventory proactively rather than reacting to historical data. The technology also improves fraud detection by identifying green claims more accurately thereby protecting brand integrity and revenue. Natural language processing facilitates better sentiment analysis allowing companies to gauge public perception and refine their sustainability messaging accordingly. Regulatory pressure for green reporting is increasing. Consequently, the barrier to entry for compliant operators is lowering, enabling responsible businesses to thrive. This technological leap ensures that the European market remains at the forefront of sustainable tourism driving efficiency and ethics across all verticals.

PERSISTENT MARKET CHALLENGES Stringent Regulatory Pathways Complicate Approval Processes

The region’s regulatory landscape is highly fragmented and rigorous, which impedes the growth of the Europe peptide market. This poses a significant challenge for developers attempting to gain approval for new peptide-based therapies across multiple borders. The continent comprises numerous distinct legal frameworks cultures and enforcement mechanisms which necessitates localized strategies that complicate unified reporting and analysis. According to sources, national health technology assessment bodies continue to exhibit significant variation in cost-effectiveness and clinical benefit criteria, causing persistent,,,fragmented, market access across the European region. Developers often struggle with disparate data reporting obligations where information formats from different countries do not integrate seamlessly leading to incomplete pictures of regional performance. The lack of a single European pricing mechanism means that reimbursement decisions are scattered across countless jurisdictional boundaries diluting the impact of broad commercial campaigns. Cross border clinical trial coordination remains problematic especially with the rise of data protection directives that limit patient data sharing between regulated and unregulated markets. Pharmaceutical executives in Europe continue to report that regulatory inconsistencies and divergent national requirements create significant hurdles to operational efficiency and timely, medicine, access. This fragmentation increases the cost and complexity of running pan European operations requiring specialized local knowledge and multiple technology stacks. The inability to harmonize standards accurately undermines confidence in digital channels and hampers strategic decision making. Overcoming this disjointed ecosystem requires substantial investment in legal counsel and harmonized compliance frameworks.

Intensifying Competition for Raw Materials Elevates Costs

The saturation of the global supply chain with an ever increasing number of peptide manufacturers holds back the expansion of the Europe peptide market. This creates intense competition for limited high quality raw materials driving up the cost of goods significantly. As more brands vie for the same protected amino acids and resins on popular platforms the auction dynamics of procurement result in inflated input prices. The European chemical industry is experiencing sustained, high-cost pressure alongside declining demand, leading to continued, challenges in maintaining profit margins. This bidding war disproportionately affects small and medium sized enterprises that lack the deep pockets of multinational corporations to sustain high acquisition costs. The sheer volume of production schedules displayed to suppliers daily leads to capacity constraints where manufacturers subconsciously prioritize larger contracts reducing overall effectiveness. Regulators continuously update their guidelines to restrict aggressive sourcing practices forcing brands to spend more on supply chain verification just to maintain visibility. The competition extends beyond traditional sectors as industries previously slow to adopt peptide technologies now flood the space adding to the congestion. Attention spans are shrinking. The, average duration, of viewer, engagement, on, digital platforms, is, decreasing, as content consumption becomes, faster, and more, ephemeral. Advertisers must therefore invest more in high quality creative production to break through the noise which further escalates campaign budgets. This relentless upward pressure on costs threatens the sustainability of customer acquisition models for many digital native travel businesses.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

8.59%

Segments Covered

By Offering, Method, Application, End-User, and Region.

Various Analyses Covered

Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities

Regions Covered

North America, Europe, APAC, Latin America, Middle East & Africa

Market Leaders Profiled

Agilent Technologies Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), Merck KGaA (Germany), GenScript (U.S.), Bachem AG (Switzerland), Waters Corporation (U.S.), Danaher (U.S.), PolyPeptide Group (Switzerland), Bio-Synthesis Inc. (U.S.), CordenPharma (U.S.)

SEGMENTAL ANALYSIS By Offering Insights

The Products segment dominated the Europe peptide market and accounted for a 62.6% share in 2025 because of the fundamental necessity of specialized hardware and consumables for the continuous synthesis and purification of peptides across research and industrial settings. A further reason for this growth is the widespread installation of automated peptide synthesizers and high-performance liquid chromatography systems which are essential for maintaining the high purity standards required by regulatory bodies. As per sources, European chemical production faced significant declines, with major capacity reductions announced and a shift in manufacturing to Asian regions. The recurring need for reagents and consumables such as protected amino acids and resins creates a steady revenue stream that sustains the segment leadership. The European pharmaceutical industry faces pressure, with R&D spending growth in Europe being outpaced by the US and China, causing a slow decline in Europe’s share of global innovation. Institutions favor product purchases because they provide long-term asset value and control over the manufacturing process compared to outsourcing. The integration of advanced detection systems within these instruments empowers researchers to identify impurities early and optimize yields proactively. Furthermore the ability to integrate third-party software for process monitoring creates a comprehensive ecosystem that locks in user dependency. These structural advantages ensure that Products remain the backbone of the European peptide supply chain.

The services segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 16.8% from 2026 to 2034 due to the increasing tendency of pharmaceutical companies to outsource non-core synthesis activities to specialized Contract Research Organizations to reduce capital expenditure and accelerate time to market. In addition, this segment is supported by the complexity of custom peptide synthesis which requires niche expertise and flexible production scales that internal teams often lack. According to sources, the pharmaceutical CDMO market in Europe is expanding, driven by increasing R&D and a trend toward regional, rather than global, supply chains to ensure reliability. The rise of library synthesis services has further intensified activity by providing researchers with vast collections of diverse sequences for high-throughput screening without internal resource allocation. Pharmaceutical companies are increasing their use of technology and outsourcing to improve efficiency and reduce costs, with a focus on AI and digital tools to enhance supply chain resilience. Providers are increasingly offering end-to-end packages that include sequence design optimization and analytical validation. The flexibility to scale production up or down based on clinical trial phases appeals strongly to emerging biotech firms. The rise of white-label solutions enables niche players to enter the market with professional-grade capabilities quickly. This convergence of expertise flexibility and cost-efficiency ensures the Services segment will outpace product sales in growth velocity.

By Method Insights

The Solid-Phase Peptide Synthesis segment led the Europe peptide market and captured a substantial share in 2025. The leading position of the segment is attributed to the superior efficiency automation potential and scalability of the method which allows for the rapid assembly of long peptide chains with high purity. Also, this sector is boosted by the widespread adoption of automated synthesizers that utilize solid supports to facilitate easy washing and removal of excess reagents minimizing side reactions. Peptide manufacturing is trending toward greater automation and larger solid-phase reactors to support the growing GLP-1 and metabolic disease landscape. The ability to synthesize multiple peptides simultaneously using parallel synthesis reactors significantly reduces turnaround times for drug discovery projects. Institutions favor this method because it reduces solvent consumption and labor costs associated with manual purification steps compared to traditional liquid-phase approaches. The integration of microwave-assisted heating within solid-phase protocols further accelerates reaction kinetics enabling the synthesis of difficult sequences. Furthermore the compatibility of this method with high-throughput screening platforms creates a seamless workflow from design to testing. These factors collectively ensure that Solid-Phase Peptide Synthesis remains the cornerstone of the European peptide industry.

The Liquid-Phase Peptide Synthesis segment is expected to exhibit a noteworthy CAGR of 12.4% during the forecast period owing to the renewed interest in producing large quantities of specific therapeutic peptides where solution-phase chemistry offers better cost-efficiency and environmental sustainability than solid-phase methods. Additionally, the segment is helped by the advancement in continuous flow chemistry technologies which allow for precise control over reaction parameters and improved safety profiles for large-scale manufacturing. As per studies, European chemical manufacturers are increasingly adopting continuous flow-based synthesis to improve process sustainability and yield. The rise of green chemistry initiatives has further accelerated adoption by minimizing the use of hazardous solvents and reducing overall energy consumption. Chemical companies are increasing investment in greener manufacturing technologies to improve environmental, social, and governance (ESG) compliance. Providers are increasingly optimizing crystallization techniques to purify intermediates without chromatography thereby lowering production costs. The flexibility to recycle solvents and reagents makes this method highly attractive for producing blockbuster peptide drugs at metric ton scales. The integration of real-time monitoring sensors enhances process control and ensures consistent quality. This alignment with industrial scale-up needs and environmental regulations ensures the liquid-phase segment will experience sustained double-digit growth.

By Application Insights

In 2025, the Therapeutics application held the majority share of 55.3% of the Europe peptide market. The dominance of the segment is driven by the critical role peptides play in treating chronic diseases such as diabetes obesity and cancer where they offer high specificity and low toxicity compared to small molecules. A major factor that aids this segment is the approval and commercialization of numerous peptide-based drugs including glucagon-like peptide-1 agonists which have become standard of care for metabolic disorders. The European Union is seeing a consistent rise in the approval of innovative biological and peptide-based therapies due to targeted research in orphan and metabolic diseases. The aging population across Europe creates a massive addressable patient base requiring long-term management of age-related conditions. Globally, the adoption of GLP-1 peptide hormone treatments is increasing sharply in response to rising diabetes and obesity prevalence. Hospitals favor these therapies because they often result in fewer hospitalizations and complications improving overall healthcare economics. The ability to engineer peptides for extended half-lives allows for less frequent dosing enhancing patient compliance significantly. Furthermore the expansion of indications for existing peptide drugs into new therapeutic areas drives continued revenue growth. These structural advantages ensure that Therapeutics remain the primary revenue engine for the peptide industry.

The Diagnostics segment is predicted to witness the highest CAGR of 19.3% over the forecast period. This rapid expansion is fueled by the increasing demand for highly sensitive and specific biomarkers for early disease detection and personalized medicine. One more point that adds strength is the development of peptide-based assays and imaging agents that can detect molecular signatures of diseases like Alzheimer’s and various cancers at earlier stages than traditional methods. According to research, Peptide-based diagnostic technologies are becoming more prevalent in European laboratories as part of growing precision medicine workflows. The rise of theranostics which combines therapy and diagnostics has further intensified activity by requiring paired peptide agents for targeted treatment monitoring. Peptide mass spectrometry is increasingly being integrated into clinical diagnostics as hospitals move toward personalized medicine. Providers are increasingly collaborating with research institutes to validate novel peptide biomarkers for rare diseases. The flexibility to modify peptide sequences for binding affinity makes them ideal for developing next-generation imaging probes. The integration of artificial intelligence in data analysis enhances the interpretation of complex diagnostic results. This convergence of technological innovation and clinical need ensures the Diagnostics segment will outpace other applications in growth velocity.

By End User Insights

The Pharmaceutical and Biotechnology Companies segment was the largest segment in the Europe and occupied a 48.7% share in 2025. The supremacy of the segment is credited to the massive scale of drug development programs and the need for large quantities of high-quality peptides for clinical trials and commercial manufacturing. Added support for this segment comes from the strategic focus of major pharmaceutical firms on expanding their biologics portfolios to address unmet medical needs in oncology and metabolic diseases. As per studies, the pharmaceutical pipeline in Europe is increasingly shifting towards biologic and peptide therapeutics, moving away from a traditional small-molecule dominance. The removal of geographical barriers enables these companies to source materials globally while maintaining strict quality controls. European R&D expenditure in the pharmaceutical sector is growing, with a significant, increasing share dedicated to biotech and specialized therapies. The flexibility of internal production facilities allows for rapid iteration and optimization of lead compounds. Governments are actively supporting this trend through funding initiatives that subsidize innovation in biomanufacturing. The integration of vertical supply chains ensures reliability and security of supply for critical medicines. This convergence of corporate strategy and scientific demand ensures the pharmaceutical sector remains the primary revenue engine for the peptide industry.

The Contract Research Organizations and Contract Development and Manufacturing Organizations segment is estimated to register the fastest CAGR of 17.6% between 2026 and 2034. This swift acceleration is propelled by the increasing trend of outsourcing among biotech startups and large pharma companies to leverage specialized expertise and flexible capacity without heavy capital investment. Along with this, the segment is driven by the complexity of peptide synthesis which requires niche skills and equipment that many internal teams lack or wish to avoid maintaining. According to sources, pharmaceutical companies are increasing their outsourcing of peptide projects to CDMOs to manage capacity, reduce risks, and accelerate development timelines. The rise of virtual biotech companies that operate without internal manufacturing facilities has further intensified demand for comprehensive CDMO services. Investment in CDMO infrastructure for peptide production is rising significantly to address backlogs and meet growing market demand. Providers are increasingly offering integrated services from sequence design to commercial supply creating sticky customer relationships. The flexibility to scale production based on clinical success rates appeals strongly to risk-averse investors. As the pipeline of peptide drugs expands the reliance on external partners for efficient execution will continue to grow rapidly.

COUNTRY LEVEL ANALYSIS Germany Peptide Market Analysis

Germany outperformed other countries in the European peptide market and accounted for a 25.1% share in 2025. The primary driver of this dominance is the strong tradition of organic chemistry and engineering excellence which provides a robust foundation for advanced peptide synthesis and manufacturing. This preeminent position is also supported by its status as the largest economy in Europe with a world-class chemical industry and a dense network of pharmaceutical research hubs. As per sources, Germany is experiencing a strong, record-setting upward trajectory in overall research and development investment across public and private sectors, with a major focus on industrial production. The country serves as a key testing ground for new synthesis technologies due to its sophisticated regulatory environment and high quality standards. A well-developed infrastructure of universities and technical institutes ensures a steady supply of skilled chemists and biologists. The German chemical industry is facing significant economic challenges and restructuring, with production in the specialty and fine chemicals sector experiencing a downward trend due to high production costs. The presence of major global pharmaceutical headquarters contributes significantly to the depth of available content and localized marketing strategies. Strict environmental regulations have forced the industry to adopt green chemistry practices enhancing long-term sustainability. This combination of economic strength technological readiness and regulatory maturity ensures Germany retains its top rank.

United Kingdom Peptide Market Analysis

The United Kingdom was the second largest player in the Europe peptide market and occupied a 18.4% share in 2025. The expansion of the segment is attributed to its world-renowned academic institutions and vibrant biotechnology startup scene. The nation benefits from a rich history of scientific discovery producing globally acclaimed research that fuels the peptide pipeline. Beyond that, the segment is influenced by the concentration of talent in cities like Cambridge and London which fosters continuous innovation in peptide drug design and delivery mechanisms. According to research, the UK biotechnology sector is experiencing rapid expansion, with strong growth in synthetic biology and peptide services, particularly in the Southeast and London areas. The presence of major contract research organizations facilitates early access to new features and beta tests for British researchers. There is a strong, upward trend in government-backed funding for innovative, sustainable, and AI-driven pharmaceutical manufacturing in the UK, creating a favorable environment for peptide innovation. The post-Brexit regulatory environment has led to unique opportunities for tailored collaborations and streamlined approval pathways for innovative therapies. High digital literacy rates among the population facilitate rapid adoption of new laboratory technologies. The strength of the English language research output also allows UK-based campaigns to serve as templates for broader international rollouts. This blend of creative prowess financial muscle and technological infrastructure cements the UK as a pivotal market.

France Peptide Market Analysis

France remains significant in the Europe peptide market because of its aggressive government initiatives to digitize the national education system and promote lifelong learning. The country has strong state involvement in developing public platforms and subsidizing access to digital resources for students and workers alike. A further driving factor is the “France 2030” investment plan which allocates billions of euros to transform education through technology and reduce inequalities in access. As per research, digital tool integration in French schools continues to grow, with a focus on AI integration and strengthened digital skills. The popularity of MOOCs hosted by prestigious institutions like Sorbonne University drives significant traffic to national platforms during academic terms. Online professional training and certification usage is increasing in France. The existence of strong labor unions that negotiate digital training rights for employees adds a unique dynamic to the corporate learning segment. Cross-border collaborations within the EU allow French learners to access a wider range of international titles seamlessly. The focus on protecting French language content ensures that local providers thrive alongside global giants. This strategic balance between state support and market innovation ensures France remains a key growth engine.

Italy Peptide Market Analysis

Italy is moving ahead steadfastly in the Europe peptide market by leveraging its rich academic heritage and growing tech sector to sustain steady demand for both academic and professional digital learning solutions. The market saw a rapid catch-up in digital adoption as traditional institutions increasingly recognize the necessity of online channels to reach broader demographics. Internet access in Italian households is becoming almost universal, particularly in homes with children, with a sharp increase in usage among older populations. A key driving factor is the government’s National Recovery and Resilience Plan which includes substantial funding for digitalizing schools and universities to modernize the education infrastructure. The tourism and hospitality sectors contribute significantly to demand for specialized online training programs to upskill workers in these vital industries. The use of mobile devices and digital platforms for educational purposes is increasing in Italy, with a strong focus on incorporating AI into learning. The fragmented nature of the small business landscape creates opportunities for scalable online training solutions that offer cost-effective compliance and skills development. The fusion of cultural wealth with modern digital tools positions Italy for sustained growth as connectivity improves in the south.

Spain Peptide Market Analysis

Spain is anticipated to expand in the Europe peptide market during the forecast period due to its strategic role as a bridge between European and Latin American educational landscapes. The nation has come to light as a critical hub for Spanish-language digital content serving millions of speakers globally through its online platforms. The market status exhibit a rapid growth in corporate training and language learning sectors as young demographics embrace flexible learning formats. Spanish companies are actively increasing investments in digitalization and training, partly driven by European financial support and a focus on sustainability. A primary driving factor is the intense popularity of language learning apps and platforms where Spain serves as a content creation center for global audiences. The government has implemented policies to promote digital literacy and access to culture which has boosted online course consumption in rural areas. Internet usage in Spain is nearing saturation among the general population, with a strong, rising trend in online shopping and daily usage. The rise of university partnerships with Latin American institutions drives cross-border enrollment in joint online degree programs. Urban centers like Madrid and Barcelona are becoming hubs for ed-tech startups attracting talent and investment from across the Spanish-speaking world. This dynamic environment ensures Spain plays an increasingly important role in the regional digital economy.

COMPETITIVE LANDSCAPE

The competition in the Europe peptide market is intensely fierce characterized by a constant battle for technological leadership and manufacturing capacity among specialized pure play manufacturers and diversified life science giants. Dominant players leverage vast chemical libraries and advanced process engineering capabilities to offer superior purity and scalability that smaller competitors struggle to match without significant capital investment. However niche operators thrive by focusing on specific difficult sequences or rare modifications where they can offer tailored expertise and flexibility that multinational corporations often lack due to standardized protocols. The landscape is further complicated by stringent environmental regulations and Good Manufacturing Practice standards across nations which forces all participants to maintain robust compliance frameworks and sustainable practices. New entrants from the contract development sector are disrupting traditional models by offering flexible scalable solutions that align closely with the needs of emerging biotech firms. Price wars occasionally erupt in commoditized reagents but differentiation increasingly relies on technical success rates speed to market and supply chain reliability. Mergers and acquisitions remain common as companies seek to consolidate capabilities and expand their geographic footprint efficiently. This dynamic environment ensures rapid evolution where adaptability technological prowess and operational excellence determine long term survival and success in the region.

KEY MARKET PLAYERS

A few of the market players that are in the Europe peptide market are

- Agilent Technologies Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Merck KGaA (Germany)

- GenScript (U.S.)

- Bachem AG (Switzerland)

- Waters Corporation (U.S.)

- Danaher (U.S.)

- PolyPeptide Group (Switzerland)

- Bio-Synthesis Inc. (U.S.)

- CordenPharma (U.S.)

Top Players In The Market

- Thermo Fisher Scientific operates as a foundational pillar within the Europe peptide ecosystem by providing comprehensive instruments reagents and services essential for synthesis and analysis. The company leverages its vast global supply chain to ensure consistent availability of high purity amino acids and advanced synthesizers across the continent. Recent actions focus heavily on expanding manufacturing capacity in key European hubs to mitigate supply chain disruptions and meet surging demand for therapeutic peptides. Thermo Fisher has launched next generation liquid chromatography systems specifically optimized for complex peptide purification enhancing resolution and speed for researchers. The firm continues to invest in digital solutions that integrate laboratory data management with synthesis workflows improving efficiency. Globally Thermo Fisher sets benchmarks for quality control and regulatory compliance in life sciences. Their commitment to supporting both academic discovery and commercial scale up ensures that clients from diverse backgrounds can access world class tools without logistical barriers.

- Merck KGaA maintains a massive presence in the Europe peptide market by utilizing its deep expertise in chemistry and materials science to deliver innovative synthesis solutions. The company excels in providing specialized resins protecting groups and custom synthesis services that resonate deeply with pharmaceutical developers seeking novel therapeutic candidates. Recent strategic moves include heavy investment in green chemistry initiatives to develop sustainable peptide production methods that reduce environmental impact. Merck has enhanced its portfolio with automated flow chemistry platforms that enable safer and more efficient large scale manufacturing for clients. The firm actively develops partnerships with biotech startups to accelerate the translation of research into viable drug candidates. Globally Merck drives innovation in process intensification and continuous manufacturing technologies. Their commitment to sustainability and scientific excellence helps align operations with modern European regulatory values while maintaining robust growth for stakeholders.

- Bachem Holding remains a dominant force in the Europe peptide market renowned for its unparalleled expertise in custom peptide synthesis and large scale commercial manufacturing. The company distinguishes itself through vertical integration controlling every step from gram scale research to multi ton production which allows for rapid deployment of complex molecules. Recent actions include significant investments in new production facilities in Switzerland and Germany to expand capacity for growing clinical and commercial pipelines. Bachem has expanded its portfolio of proprietary linker technologies and building blocks to address challenging sequences that competitors cannot synthesize efficiently. The firm continues to refine its quality assurance systems to maintain integrity in highly regulated therapeutic ecosystems which is crucial for retaining major pharmaceutical partners. Globally Bachem influences the sector by setting high standards for purity and scalability in peptide drug substance manufacturing. Their dedication to long term partnerships fosters strong brand loyalty. This independent approach allows them to adapt quickly to changing regulatory landscapes while maintaining profitability across diverse international regions.

Top Strategies Used By Key Market Participants

Key players in the Europe peptide market primarily focus on capacity expansion to address the growing backlog of orders for clinical and commercial peptide manufacturing. Companies heavily invest in green chemistry and continuous flow technologies to improve sustainability and reduce production costs associated with traditional batch processes. Strategic partnerships with biotechnology startups help secure early stage projects and build long term relationships as candidates progress through clinical trials. Major participants are expanding their service portfolios to include end-to-end solutions ranging from sequence design to final drug product formulation. Development of proprietary building blocks and linker technologies ensures competitive advantage in synthesizing complex and difficult peptide sequences. Firms also prioritize regulatory compliance and quality assurance to build trust with global pharmaceutical clients and navigate strict European guidelines. Continuous localization of support teams addresses the diverse linguistic and cultural needs of different European countries. These strategies collectively aim to maximize operational efficiency while navigating complex regulatory landscapes effectively.

MARKET SEGMENTATION

This research report on the Europe peptide market is segmented and sub-segmented into the following categories.

By Offering

- Peptide Synthesizers

- Lyophilizers

- Chromatography Systems

- Others

- Custom Research-Grade Peptide Synthesis

- Peptide Library Synthesis

- Others

By Method

- Liquid-Phase Peptide Synthesis

- Solid-Phase Peptide Synthesis

- Others

By Application

- Therapeutics

- Diagnostics

- Research & Development

By End-User

- Pharmaceutical & Biotechnology Companies

- CROs & CDMOs

- Academic & Research Institutes

- Others

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe