This article was originally published in Vol. 6 No. 1 of our print edition.

Selective Criticism and the Reality of Russian Imports

In recent decades, Europe’s energy discourse has largely revolved around capriciously changing morals and arbitrarily shifting political agendas. This has been particularly evident in the oversimplified debate over the juxtaposition of fossil fuels against all the other energy carriers. There was a time when we used to speak about the oil and gas market, then it became the gas and oil market, and now there is little desire to mention either, especially in Europe.

After the start of the full-scale invasion of Ukraine, there was intensified political pressure at the EU level to accelerate the ‘inevitable’ abandonment of fossil fuels, above all Russian oil and gas, often blurring the line between strategic necessity and political signalling. Following the adoption of successive European sanctions packages targeting Russian energy imports, as well as a growing set of complementary energy market regulations and policy instruments, increasingly harsh criticism has been levelled at Hungary (and Slovakia) for their continued purchase of Russian crude oil and pipeline gas. The narrative is always the same: it is the recalcitrant Hungarians with their persistent addiction to Russian energy who are preventing the EU from completing its departure from Russian energy. As the war approaches its fourth anniversary, and new sanctions as well as complementary policy instruments are deployed against Russian energy, a fundamental question becomes unavoidable: is the prevailing narrative actually true? Has Hungary really become the last European customer of Russian oil and gas? Or, much like in the debate over restrictive migration policies, are we once again witnessing another case of selective criticism and EU hypocrisy?

Hungary as a Case Study in Selective Criticism

In recent years, Hungary has frequently been criticized at the EU level for its heavy reliance on Russian energy supplies. For one thing, these criticisms tend to overlook the structural conditions that primarily define Hungary’s energy choices. In addition, broader European energy import patterns suggest that Hungary’s situation is far from unique. While direct pipeline dependence has decreased, substantial volumes of Russian energy continue to enter the European Union through alternative—i.e. less visible and less easily identifiable—channels. In practice, energy import dependence has not vanished from the European system. It has simply been pushed out of sight, only to re-emerge through indirect routes and increasingly complex market arrangements. The uneven criticism levelled at Hungary illustrates that the central issue at the EU level is not whether dependence exists, but the extent to which it is acknowledged or concealed.

It is not the aim of this article to provide a comprehensive technical or policy assessment of Europe’s energy system; nor to recount the myriad reasons why it is challenging, time-consuming, and expensive for a country like Hungary to completely wean itself off Russian energy; nor to list all the projects, initiatives and investments that have been embarked upon for the sake of energy diversification. Instead, we seek to highlight a number of overlooked—and sometimes uncomfortable—structural and political realities that underscore the selective nature of the criticism levelled at Hungary. We aim to highlight that while criticism of Hungary is framed as indisputable, the country’s energy dependencies are rarely examined in a comparable context. At the same time, the broader landscape of the European debate seldom seeks to address similar dependencies and inconsistencies elsewhere in the European Union. In this context, what mainly distinguishes Hungary (and Slovakia) from much of Europe is not necessarily the existence of dependence itself, but the fact that it is neither concealed nor obscured behind often empty virtue signalling.

The Official Narrative: Decoupling at All Costs

The adoption of the Paris Agreement in 2015 signalled an expected decline in the long-term role of fossil fuels, yet investment patterns after 2015 tell a different story. According to the International Energy Agency (IEA), fossil fuels are set to remain a core part of the global energy mix for decades, with oil and natural gas demand expected to grow into the 2030s.1 Alongside the expansion of renewables, capital flows into coal, oil, and gas have remained substantial. Additionally, between 2010 and 2020, global energy demand increased by nearly one fifth, while greenhouse gas emissions rose at a comparable rate. This underlines a basic structural reality: despite rising climate ambition, economic growth has remained closely tied to fossil energy consumption globally.2

‘In practice, energy import dependence has not vanished from the European system’

Despite these factors, the EU has increasingly framed the rapid phase-out of fossil fuels, and particularly decoupling from Russian energy, as both a strategic necessity and a political priority after the start of the full-scale invasion of Ukraine, the EU’s most ambitious energy policy response to the events of the global technology and energy transition. The direction was later formalized on 6 May 2025 with the publication of the REPowerEU Roadmap,3 which set out concrete measures to end the dependency on Russian energy, including a timeline to phase out Russian gas imports, while addressing oil and nuclear product dependencies as a subsequent, differentiated policy objective. In official communication, the strategy suggests that Europe is both politically unified and technically capable of rapidly redesigning its energy system. In practice, however, the narrative rests on fragile assumptions about substitution, market flexibility, and regulatory dependability, treating Russian energy less as a market input than a systematic risk to be managed administratively. At the same time, the gap between long-term energy system realities and policy expectations remains blurred and has become a tool for political blackmail.

What the Numbers Actually Say: Russia Still in the Mix

Gas

According to data from the IEA and the European Commission, the share of Russian pipeline gas in EU gas imports fell from roughly 40 per cent in 2021 to an estimated 11 per cent by 2024.4 This shift has been presented as evidence of successful decoupling, but the reality is more complex. As pipeline imports fell, the EU shifted to LNG, which today predominates in the bloc’s gas supply—including from sources that are partly Russian or arrive from Russia indirectly.

Although a political decision was reached as early as 2022 to completely phase out Russian gas, a specific roadmap was only published in May 2025,5 and it was not until the autumn of 2025 that the EU moved against Russian LNG by formally sanctioning it in its 19th sanctions package.6 At the same time, the phase-out of pipeline gas was handled through regulatory and energy-security instruments in December 2025, and entered into force on 1 January 2026.7 This latter process remains contested by several member states.

The EU has set a gradual timeline for the phasing out of Russian LNG and pipeline gas, with the implementation of these bans depending on the type and duration of existing supply contracts. For short-term supply contracts concluded before 17 June 2025, the prohibition on LNG imports will come into effect on 25 April 2026. For long-term contracts, the prohibition will enter force on 1 January 2027. For pipeline gas, the prohibition will be enforced starting from 17 June 2026 for short-term contracts, while long-term contracts are scheduled to end on 30 September 2027. Finally, a ‘safeguard provision’ allows member states to extend this deadline until 1 November 2027 in cases where security-of-supply risks, including gas storage filling constraints, cannot be adequately mitigated.8

The passage of the 19th sanction package in October 2025—primarily covering LNG— was hailed as transformative. If we look at the growing appetite of Western and Southern European countries for Russian LNG since the start of the full-scale invasion, we can understand why. In 2024, the EU increased its imports of Russian gas by 18 per cent on a yearly basis, from 38 to 45 billion cubic meters (bcm). This expansion was mainly driven by an increasing demand for Russian LNG. The top three countries fuelling this growth were Italy, the Czech Republic, and France, augmenting their imports of Russian gas by 4, 2 and 1.7 bcm respectively.9 One wonders why two major economies—whose governments are vocal supporters of Ukraine—with easy access to the global energy market are increasing their imports of a product that they had not previously needed, and which is supposed to be phased out as soon as possible. But the hypocrisy surrounding Russian gas does not stop here.

SOURCE: own edit based on CREA, ‘Payments to Russia for Fossil Fuels since 24 February 2022’, Russia Fossil Tracker, https://www.russiafossiltracker.com/, accessed 30 January 2026.

SOURCE: own edit based on CREA, ‘Payments to Russia for Fossil Fuels since 24 February 2022’, Russia Fossil Tracker, https://www.russiafossiltracker.com/, accessed 30 January 2026.

SOURCE: own edit based on CREA, ‘Payments to Russia for Fossil Fuels since 24 February 2022’, Russia Fossil Tracker, https://www.russiafossiltracker.com/, accessed 30 January 2026.

SOURCE: own edit based on CREA, ‘Payments to Russia for Fossil Fuels since 24 February 2022’, Russia Fossil Tracker, https://www.russiafossiltracker.com/, accessed 30 January 2026.

Germany, for example, banned the direct import of Russian LNG, but this does not mean that the country stopped purchasing and using gas from Russia altogether. Firstly, once gas molecules are injected into the European network, it becomes difficult to trace their origin. Secondly, the global LNG market is driven by competition, so in many cases, the cheapest or most readily available LNG is purchased, regardless of its place of origin. The difficulties of tracing the origins of LNG entering the European network are also exacerbated by a burgeoning fleet of shadow vessels. These loopholes and lack of transparency in the European system enable some countries—including the biggest economy in Europe—to ‘whitewash’ their statistics and show a reduced proportion of ‘Russian gas’ in their books, while in reality they are buying Russian-produced LNG on the market.

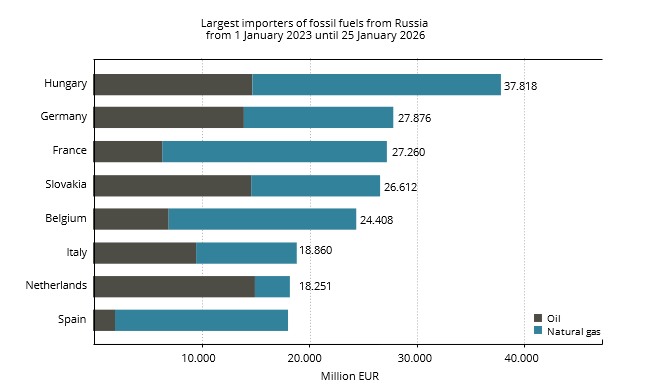

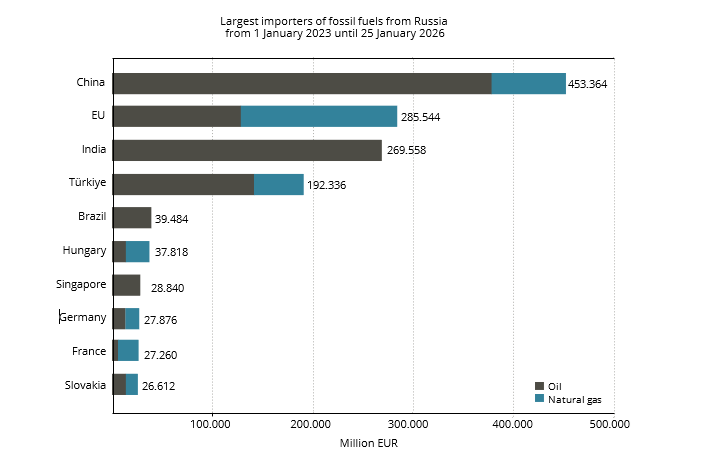

While several major European economies have increased their imports of Russian gas in 2024, Hungary and Slovakia—two countries, often labelled the ‘black sheep’ of Europe for their reliance on Russian energy—have actually reduced their import volumes year-on-year. As a result of these reductions, Italy surpassed Hungary in 2024 to become the largest importer of Russian gas within the EU, with France following close behind in third position.

At the time of writing, fully consolidated annual datasets for 2025 are not yet available from the principal statistical authorities, but it is worth highlighting one data point. In spite of committing to a complete exit from Russian LNG by 2027, imports reached record levels by value last year. According to a recently published Urgewald report, the EU imported a record €7.2 billion worth of LNG from the Kremlin’s Yamal LNG project—the latter being responsible for the overwhelming majority of Russian LNG imports into the bloc. This figure is a staggering 14 per cent year-on-year increase from the €6.3 billion in 2024. It seems that Western Europe is trying to squeeze out as many Russian gas molecules as it can before the successive bans kick in.10 In the case of Hungary, Russian pipeline gas imports also reached elevated levels in 2025, representing the highest volumes in the post-invasion period. Yet, considering the abovementioned broader European LNG trends, the small European country appears far less of an outlier. Yet Hungary remains the target of the majority of international criticism.11

Oil

Since mid-2022, the EU has formally banned most seaborne imports of Russian crude oil as part of its sanctions regime. However, this ban has never been comprehensive. Pipeline deliveries via the Druzhba (Friendship) Pipeline were explicitly exempted for a group of landlocked Central European countries, including Hungary. Additionally, while a prohibition was introduced on the direct import of Russian petroleum products in 2023,12 refined oil products derived from Russian crude continued to enter the EU through global trade channels as late as January 2026.

In January 2022, Russia earned €30.7 billion from global fossil-fuel exports, with more than half of that revenue coming from the EU. By January 2025, monthly revenues had fallen to €18.4 billion, and the EU’s share declined to around 9 per cent.13 By late 2025, the EU’s remaining exposure was concentrated in fewer, more visible channels on the crude side, while on the product side volumes increasingly shifted into less visible routes, creating two distinct layers.

The most visible channel remains the Druzhba Pipeline exemption for Hungary and Slovakia. The Centre for Research on Energy and Clean Air (CREA) estimates that since the invasion, this route has delivered approximately 39 million tonnes of Russian crude to the EU, worth €19 billion. In the third year of the war alone, Hungary and Slovakia imported 10.8 million tonnes, valued at €4.9 billion14—a source of severe criticism. However, a second layer of less visible exposure sits downstream. CREA finds that in the third year of the Russia–Ukraine War, G7+ countries imported €18 billion worth of oil products from six refineries in India and Türkiye that process Russian crude, with an estimated €9 billion of those products refined from Russian-origin crude.15 At the end of the day, both routes are revenue streams from the Kremlin’s perspective, yet there is a significant difference in how these are viewed from the outside. Direct pipeline crude remains politically salient and controversial, while refined-product pathways allow Russian crude to be transformed and reintroduced through global trade channels where public visibility and political scrutiny are less robust.

‘Russian energy has not disappeared from Europe, it has merely been redistributed’

The EU’s January 2026 measure significantly altered the above picture, targeting the refined-product channel by prohibiting imports of certain petroleum products.16 This is a significant regulatory step, and its effectiveness will remain uncertain for some time. The measure addresses a legal category rather than a physical flow, and its implementation will unfold throughout 2026. However, several structural limitations are already apparent in market and compliance discussions:

First, traceability is documentary rather than chemical. The origin of refined products cannot be verified through physical testing; enforcement relies on paperwork, supply-chain declarations, and compliance procedures, all of which are vulnerable to manipulation and misreporting. This is because the ban is enforced through customs paperwork rather than through any physical verification of origin. At the end of the day, what matters is how a product is classified on paper, not where its molecules actually come from.17 As a result, companies apply different risk thresholds, producing uneven outcomes across markets, which increases opacity rather than transparency.18

This phenomenon is already observable in practice. By December 2025, sanctions evasion in global oil markets had evolved into a well-structured parallel system at sea. According to CREA, by the end of last year, 93 shadow vessels were operating under false flags, transporting Russian crude oil and oil products,19 revealing systemic vulnerabilities rather than isolated loopholes.20

‘At the end of the day, both routes are revenue streams from the Kremlin’s perspective, yet there is a significant difference in how these are viewed from the outside’

What has become increasingly evident in the EU’s approach to oil is a persistent tendency to treat a fundamentally physical and systemic challenge as primarily a legal one. It seems that the EU has exchanged a politically visible dependency for an invisible one, at least as far as the market is concerned. This may satisfy regulatory objectives in the short term, but it weakens Europe’s ability to manage real supply shocks and ultimately erodes the credibility of the energy transition itself.

Conclusion

In the words of the widely respected economist John Maynard Keynes, ‘when the facts change, I change my mind’. Sound conclusions—those which most closely correspond to the truth—rarely present themselves easily, and without careful observation it is easy to remain trapped in the same rhetorical positions, perhaps with a little rebranding. For a long time, technical reality was treated as a secondary consideration by many, but recent crises have shattered this illusion. The COVID-19 pandemic, the subsequent economic shocks, and the war in the immediate neighbourhood of the EU have demonstrated with ruthless clarity that the geopolitical landscape moves faster than previously assumed, and that energy is inseparable from statecraft.

The evasion of sanctions in global energy markets has evolved into a structured parallel system. Rather than disappearing, sanctioned energy flows adapted, changing routes and legal forms. The issues did not vanish; they simply changed shape. This process of adaptation does not only apply to oil, but is equally visible in the natural gas market, revealing the unintended consequences of partial sanctions. The EU’s ban on the transhipment of Russian LNG highlights how limited measures can misdirect rather than resolve systemic dependence. What was presented as enforcement became misdirection: the routes changed, the legal form shifted, but the molecules kept moving. A similar reluctance to confront reality is visible in the nuclear sector, where several member states remain dependent on Russian technology, fuel, or services, and where diversification is slow, costly, and politically constrained.

By the end of 2025, it was evident that Hungary and Slovakia were not the only EU member states still importing Russian energy. Russian gas and oil continue to enter the EU as LNG shipments, pipeline exemptions, refined products, and indirect trade routes. While these flows are expected to change from 2026 onward as new restrictions take effect, the present reality is clear: Russian energy has not disappeared from Europe, it has merely been redistributed. The EU may aim to eliminate Russian fossil fuels by 2027, but treating the situation in 2025 as a uniquely Hungarian or Slovak problem misrepresents the facts.

NOTES

1 ‘World Energy Outlook 2025’, International Energy Agency (12 November 2025), www.iea.org/reports/world-energy-outlook-2025.

2 ‘The Energy World Is Set to Change Significantly by 2030 Based on Today’s Policy Settings Alone’, International Energy Agency (24 October 2023), www.iea.org/news/the-energy-world-is-set-to-change-significantly-by-2030-based-on-todays-policy-settings-alone.

3 ‘REPowerEU Roadmap’, European Commission (6 May 2025), https://energy.ec.europa.eu/strategy/repowereu-roadmap_en.

4 ‘Where Does the EU’s Gas Come From?’, Council of the European Union (13 November 2025), www.consilium.europa.eu/en/infographics/where-does-the-eu-s-gas-come-from/.

5 ‘REPowerEU Roadmap’.

6 ‘EU Adopts 19th Package of Sanctions Against Russia’, European Commission (23 October 2025), https://finance.ec.europa.eu/news/eu-adopts-19th-package-sanctions-against-russia-2025-10-23_en.

7 ‘EU Agrees on Level of Price Caps for Russian Petroleum Products’, Council of the European Union (3 December 2025), https://ec.europa.eu/commission/presscorner/detail/en/ip_25_2860.

8 ‘EU Regulation Banning Imports of Russian Natural Gas Expected in Early 2026’, CMSLaw-Now(8 January 2026), eu-regulation-banning-imports-of-russian-natural-gas-expected-in-early-2026#:~:text=in%20early%20 2026-, EU%20Regulation%20banning%20imports%20of%20Russian%20natural%20gas%20expected%20in,apply%20from%2025%20April%202026.

9 ‘Russian Gas Imports to the EU Jump by 18% in 2024 Despite Plan for 2027 Phase-Out’, Ember Energy (27 March 2025), https://ember-energy.org/latest-updates/russian-gas-imports-to-the-eu-jump-by-18-in-2024-despite-plan-for-2027-phase-out/.

10 Malte Humpert, ‘EU Spent €72 Billion on Russian LNG in 2025, Maximizing Imports Before 2027 Ban’, High North News (19 January 2026), www.highnorthnews.com/en/eu-spent-eu72-billion-russian-lng-2025-maximizing-imports-2027-ban#:~:text=%E2%80%9CThe%20EU’s%20ban%20on%20transshipments, Too%20many%20loopholes.

11 ‘EU Imports from the Kremlin’s Flagship Yamal LNG Project Hit €72 billion’, Urgewald (8 January 2026), www.urgewald.org/en/media/2025-eu-imports-kremlins-flagship-yamal-lng-project-hit-eu72-billion.

12 ‘Sanctions Against Russia Explained’, Council of the European Union, www.consilium.europa.eu/en/policies/sanctions-against-russia-explained/#:~:text=non%2DEU%20 countries-, What%20does%20the%20oil%20ban%20 mean%20in%20practice?,of%20Russian%20vacuum%20gas%20oil.&text=The%20impact%20of%20the%20oil,substantially%20on%20this%20oil%20revenue, accessed 26 January 2026.

13 ‘December 2025: Monthly Analysis of Russian Fossil Fuel Exports and Sanctions’, CREA (Centre for Research on Energy and Clean Air) (13 January 2025), https://energyandcleanair.org/ december-2025-monthly-analysis-of-russian-fossil-fuel-exports-and-sanctions/.

14 ‘December 2025: Monthly Analysis of Russian Fossil Fuel Exports and Sanctions’; ‘EU Imports of Russian Fossil Fuels in Third Year of Invasion Surpass Financial Aid Sent to Ukraine’, CREA (24 February 2025), 2–3, https://energyandcleanair.org/publication/eu-imports-of-russian-fossil-fuels-in-third-year-of-invasion-surpass-financial-aid-sent-to-ukraine/.

15 ‘EU Imports of Russian Fossil Fuels in Third Year of Invasion Surpass Financial Aid Sent to Ukraine’, 2.

16 ‘Regulation amending restrictive measures concerning petroleum products derived from Russian crude, Council of the European Union, adopted January 2026’, Eur-Lex, https://eur-lex.europa.eu/legal-content/EN/TXT/?-qid=1769423848855&uri=CELEX%3A62024TJ0174, accessed 26 January 2026.

17 ‘Commission Implementing Regulation (EU) 2026/14’, The European Commission (14 January 2026), https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:L_202600124.

18 ‘New EU Oil Sanctions Spark Spiralling Complexity’, Argus (20 January 2026), www.argusmedia.com/.

19 ‘113 Vessels Flying a False Flag Transported EUR 4.7 Bn Russian Oil in First Three Quarters of 2025’, CREA (27 November 2025), https://energyandcleanair. org/publication/flags-of-inconvenience-113-vessels-flying-a-false-flag-transported-eur-4-7-bn-russian-oil-in-first-three-quarters-of-2025/; ‘December 2025: Monthly Analysis of Russian Fossil Fuel Exports and Sanctions’.

20 ‘December 2025: Monthly Analysis of Russian Fossil Fuel Exports and Sanctions’.

Related articles: