The Central Balkans are positioning themselves as Europe’s premier construction hub. The residential construction boom in Albania and Montenegro, along with large-scale infrastructure projects in Serbia and North Macedonia, are the main drivers of steel sales. Significant changes are on the horizon for this market.

Market profile

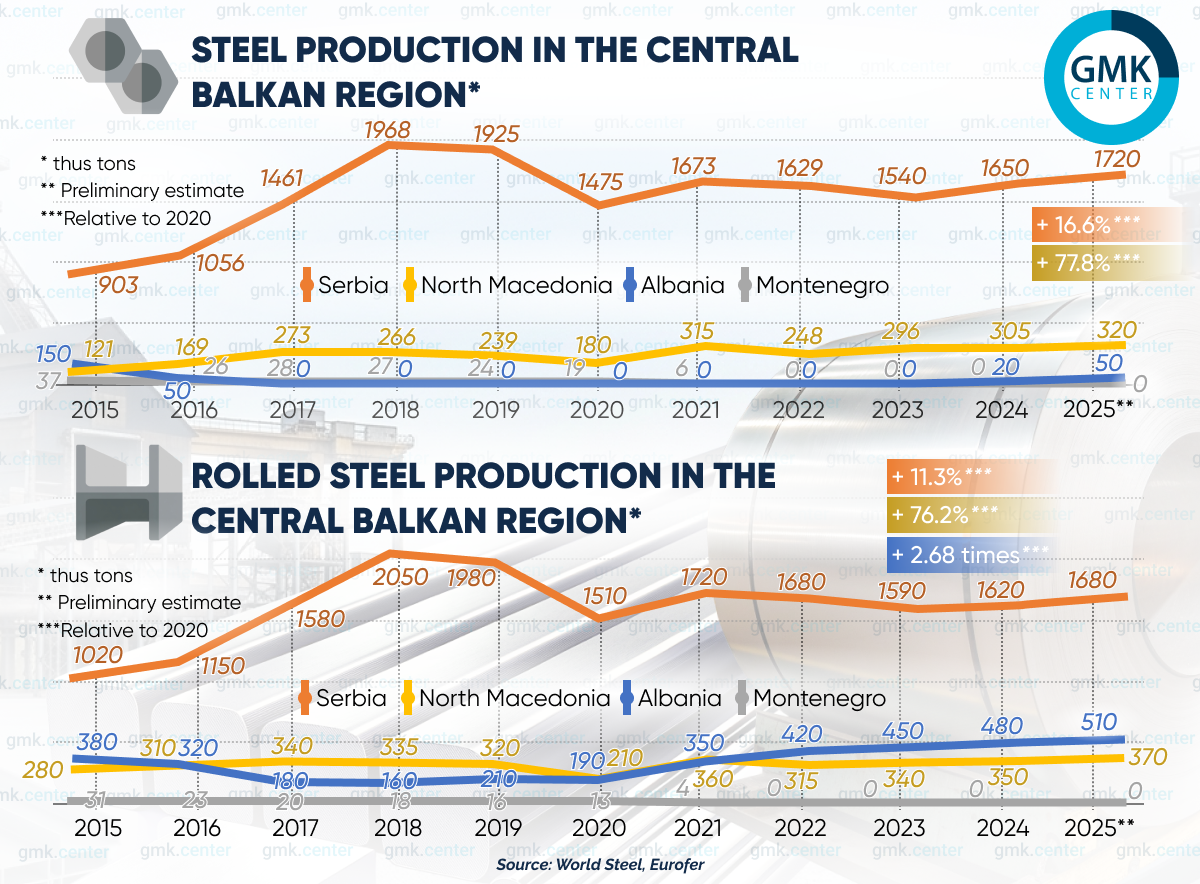

The main local player is the Serbian integrated steel mill Zelezara Smederevo (part of the Chinese HBIS Group). It is a major producer of cold-rolled and hot-rolled coil with an annual capacity of 2.2 million tons. Long products are produced by electric arc furnace plants: North Macedonian Makstil (owned by the Swiss Duferco Group) in Skopje and Albanian Kurum International in Elbasan. Their capacities are 1.35 million tons and 0.7 million tons, respectively.

Zelezara Smederevo and Makstil have been steadily increasing steel production in recent years in response to rising demand. Kurum’s steelmaking facilities are largely idle for various reasons. The company focuses on rolling imported billets.

Two pure rolling mills that do not have their own steelmaking operations are the Serbian steel mill Metalfer Steel Mill in Sremska Mitrovica and Liberty Skopje. The former produces long products and rebar, while the latter produces cold-rolled coils and galvanized steel. Both operate at high capacity. Their design capacities are 0.5 million tons and 0.75 million tons, respectively.

The Montenegrin integrated steel mill Zelezara Niksic, managed by the Turkish Tosyalı Holding, operated until spring 2021, after which production was halted. It is now owned by the state-owned energy company EPCG. The plant requires significant modernization of its steelworks, which the new owner is unable to finance. A restart in the near future is not expected. Annual capacity is 0.25 million tons.

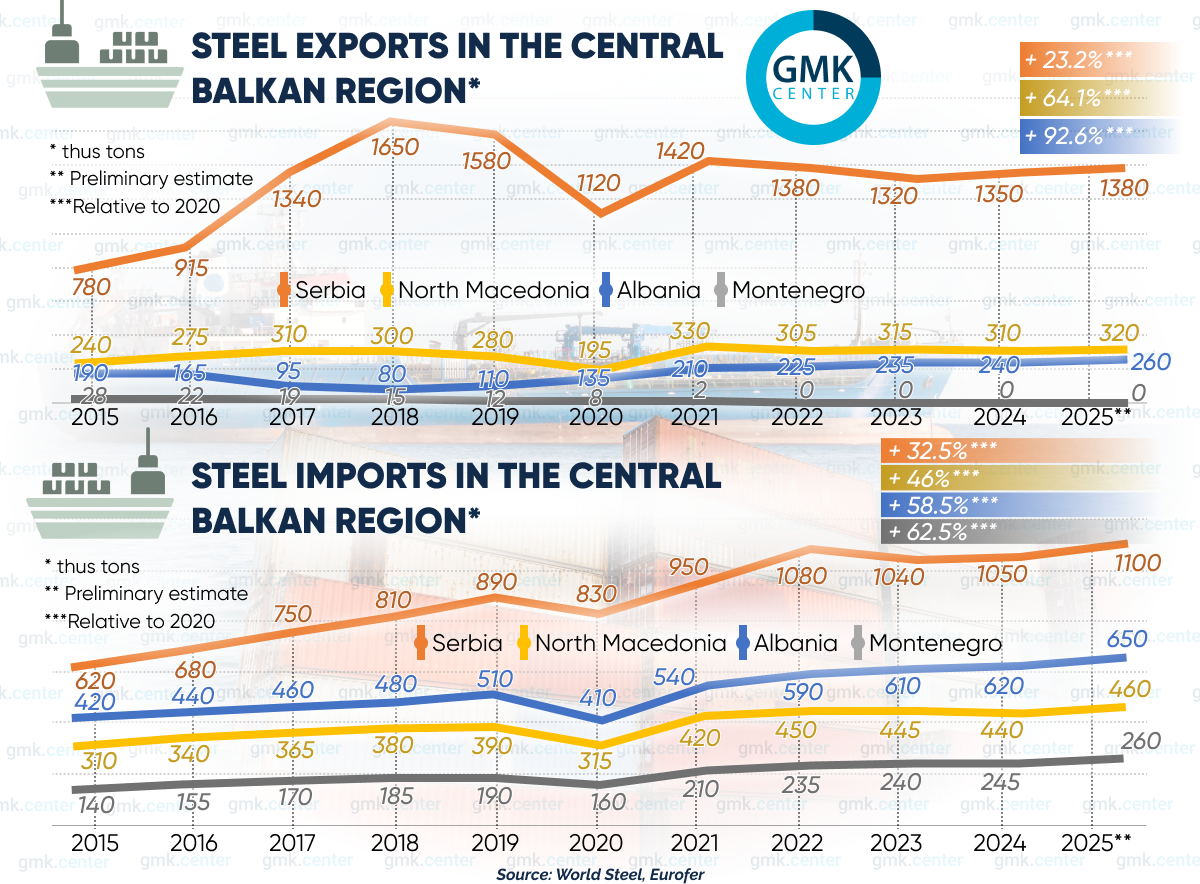

Serbia is the only net exporter in the region, thanks to Zelezara Smederevo. In North Macedonia, a significant portion of imports consists of steel slabs for Liberty Skopje. Montenegro’s import statistics include shipments of finished rolled steel that Zelezara Smederevo ships to customers via the Montenegrin port of Bar.

The situation in Albania is particularly interesting. Despite huge domestic demand, Kurum exports most of its production. The main destinations are Italy and Serbia. There are specific reasons for this:

- Foreign currency revenue is more advantageous for Kurum International, as part of its expenses are denominated in euros (primarily the purchase of scrap).

- Dumping from Turkey due to economies of scale. Turkish giants Erdemir and Kardemir often dump their stockpiles of rebar onto the Albanian market at prices below market rates.

- Price-to-quality ratio. Albanian developers most often need only rebar. The plant in Elbasan is certified to EU quality standards. It is more profitable for it to sell to Italy or for complex infrastructure projects in Serbia, where buyers are willing to pay a premium for certification and compliance with Eurocodes.

As a result, the Albanian market is dominated by long products from Turkey. The Serbian company Metalfer ships most of its production to Montenegro (over 40% of total imports there). In Serbia itself, structural steel and rebar are also mostly of foreign origin.

Demand for flat steel

The machinery manufacturing sector—the main consumer of flat steel—exists only in Serbia and North Macedonia. The largest Serbian consumers of sheet steel are:

- The automobile plant in Kragujevac, owned by the global Stellantis Group. Previously, the main model assembled here was the Fiat 500L; now it is the Fiat Grande Panda electric vehicle.

- The Siemens Mobility railcar plant in Kragujevac. It manufactures trams, most of which are exported to Germany.

- The FMP Agromehanika machine-building plant—a manufacturer of tractors and agricultural attachments.

- The Gorenje plant in Valjevo (part of the Chinese Hisense Group), which produces a wide range of home appliances.

In North Macedonia, these include, first and foremost, the bus factory in Skopje, owned by the Belgian Van Hool Group, and the diversified machine-building plant Brako in Veles.

Steelworking — the second-largest consumer of flat-rolled steel—is the most developed sector in North Macedonia. The largest steel structure plants, Fakom and Rade Končar, manufacture bridges, frames for thermal power plants, wind towers for wind farms, and mine structures. The majority of their products are exported to Germany and Austria. The main supplier of rolled steel is Makstil.

Wind energy has limited potential in mountainous terrain, but it does exist. The largest wind farm, Čibuk 1, with a capacity of 158 MW, is located in Serbia. The total capacity of Serbian wind farms is 262 MW. The 66-MW Kostolac wind farm is under construction, commissioned by the state-owned energy company EPS.

The combined capacity of the Montenegrin wind farms Krnovo and Možura is 118 MW, and the 54-MW Gvozd wind farm is under construction. In North Macedonia, the Bogoslovec and Bogdanci wind farms, with a combined capacity of 73 MW, have been commissioned. All of these facilities were commissioned in 2024–2025, influencing demand dynamics. The sector’s current steel consumption capacity is approximately 12,000 tons. There are currently no wind farms in Albania, but there are plans to build them.

Demand for long products

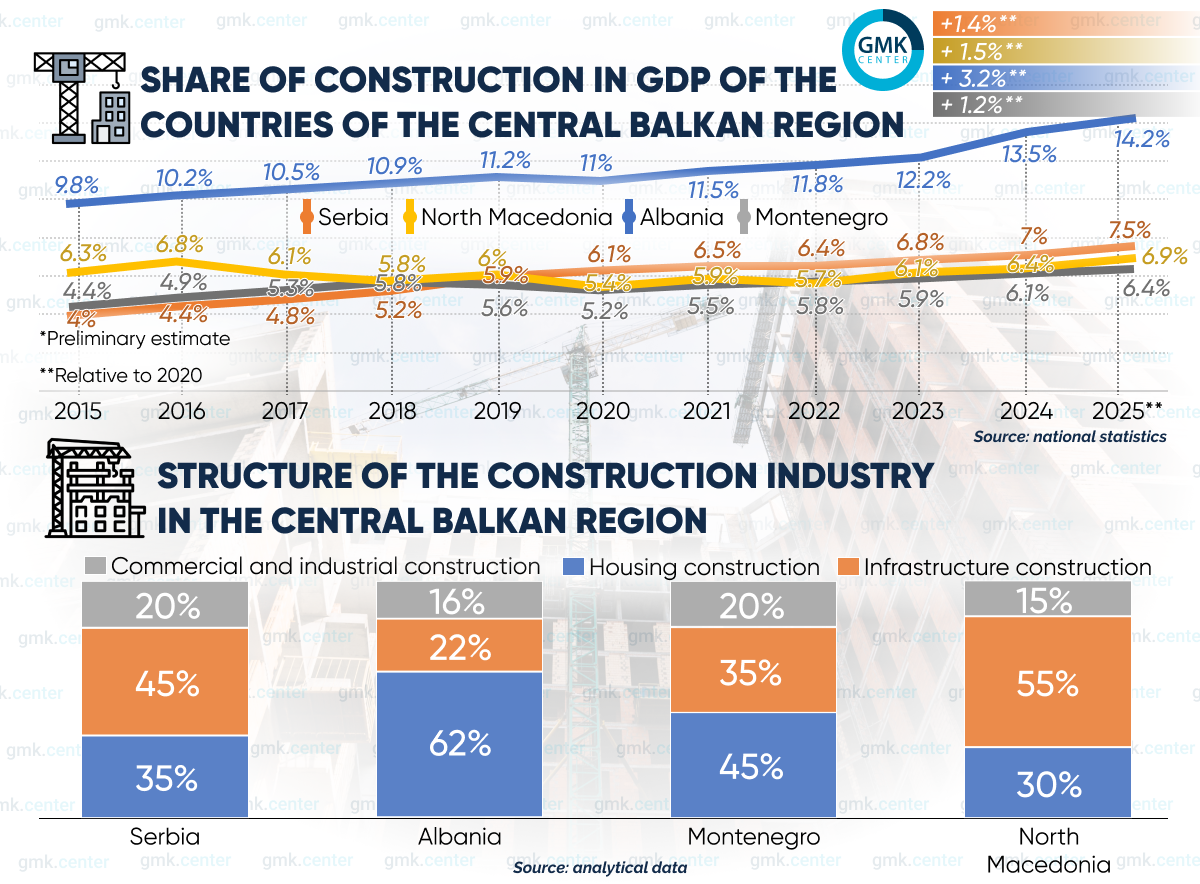

The construction industry — the main consumer of long products and rebar — is the driving force behind the regional economy. In Serbia and North Macedonia, demand is primarily driven by infrastructure projects funded by the EU and China. In Montenegro and Albania, residential construction dominates, fueled by a tourism boom.

The region has one of the highest levels of steel consumption in Europe per €1 million of the construction sector’s contribution to GDP. This is due to the mountainous terrain — any building or road requires massive retaining walls and deep pile foundations. The construction of just one bridge, the “Moracica” in Montenegro on the “Bar–Boljari” highway, required approximately 15,000 tons of rebar.

Construction GDP in Serbia reached a historic high by the end of 2025 — over 108 billion RSD per quarter. Key projects are related to preparations for the EXPO-2027 World’s Fair in Belgrade:

- construction of a national exhibition complex;

- construction of a residential complex in Surčin (intended to house exhibition participants and guests; after the exhibition, it will become part of the housing stock);

- modernization of the railway station and airport in Belgrade.

Another landmark project, completed in the fall of 2025, was the construction of the high-speed (up to 200 km/h) “Belgrade–Subotica” railway. This is the Serbian section of the new “Belgrade–Budapest” route, financed by Chinese state-owned banks as part of the “Belt and Road” initiative.

In North Macedonia, the construction sector’s 19% growth in 2025 was almost entirely driven by work on transport corridors 8d and 10d, which connect Albania with Bulgaria and Greece with Austria. This includes 109 km of new highways and a new railway line on the “Kriva Palanka – Bulgarian border” section. Large volumes of steel structures are being used here for bridges and interchanges.

In Montenegro and Albania, the main driver of demand for finished steel is residential construction. As in Greece, this is stimulated by foreign investment in tourism real estate. Villas and mini-hotels are registered as residential buildings.

Buyers believe that after integration into the European Union, prices for these properties in Albania and Montenegro will match those in Croatia and Greece, so they are rushing to invest in the “last cheap gems of the Adriatic.”

A likely significant increase in tourist traffic to Albania is also anticipated following the opening of the new airport in Vlora, scheduled for late June 2026.

Outlook for 2026

Industrial demand for flat-rolled products will remain stable. Balkan-quality products are comparable to German and Italian ones but at lower production costs, which is why Serbian and Macedonian mills often win tenders to supply products to Germany and Italy. This ensures the stability of their market positions.

Plans to develop wind energy could drive demand growth. The pace of their implementation depends not so much on market conditions as on local bureaucracy.

- Serbia plans to increase its wind power capacity to 3 GW by 2030. The first auctions under the government program were held in 2023–2024.

- Montenegro has announced plans to export green electricity to Italy, which involves the construction of new wind farms. The announced projects are estimated at 100 MW.

- In North Macedonia, plans for new wind farms totaling 150 MW are on paper. The client is the state-owned energy company ESM.

- In Albania, construction of the first 150 MW wind farms in mountainous regions is expected to begin.

In total, these projects will require 120,000–140,000 tons of rolled steel. Part of this volume will likely go to Makstil, which is certified to supply sheets up to 100 mm thick for wind turbine tower sections.

Demand for long products will continue to grow. The construction boom in the region is ongoing. This is indicated by statistics on new permits issued for 2025.

- In Serbia, the figure fell by 2.4% – to 31,027, but this follows a record-breaking 2024. Construction permits were issued for over 40,000 apartments in high-rise buildings, 5,705 of which were issued in December alone.

- In Albania, construction permits were issued for projects with a total value of €1.07 billion and a total area of 2.47 million m² — 19.5% and 14.3% more than in 2024. The number of permits issued rose by 4.6% to 1,684.

- In Montenegro, the slowdown in the first and second quarters (30 and 10 permits were issued, respectively) is attributed to regulatory changes. Authority was transferred to municipalities, and time was needed for adaptation. In the fourth quarter, the slump was offset—277 permits were issued, which is 4.7 times more y/y. By year-end, the construction of 2,283 apartments is planned.

- In North Macedonia, the number of permits decreased by 11%, to 3,621, also following a record-breaking 2024. The second reason is developers’ shift toward more expensive and larger-scale projects. Approximately 70% of all permits are for high-rise buildings (residential buildings and office centers), and nearly 12% are for road infrastructure projects. The construction of over 8,000 apartments is planned.

This year, a new large-scale infrastructure project will begin in Belgrade — the construction of the first metro line. Tunnel boring is scheduled to begin in the second half of 2026. A significant amount of structural steel will be required to complete the work.

In Albania, construction of the 84.3-km-long Vlora–Rogozina railway will begin in the second half of the year. It will connect the airport to the main transport network.

Taking this into account, an increase in regional steel consumption can be expected in 2026: in Serbia — up to 1.52 million tons, in Albania — up to 0.95 million tons, in North Macedonia — up to 0.56 million tons, and in Montenegro — up to 0.29 million tons.

Market developments

Effective January 1, 2026, the Serbian government has imposed import quotas on flat steel, rebar, and wire rod for a period of six months (with the possibility of extension). Shipments exceeding the quota are subject to a 50% tariff.

Metalfer’s own production capacity is insufficient to meet domestic demand. Imports will continue, but prices will rise. Local producers will raise their selling prices. This could affect demand from private developers in addition to the impact of the SVA.

The main foreign suppliers are Turkish steel mills. They will likely attempt to redirect the volumes of long products they can no longer sell in Serbia to neighboring Montenegro, Albania, and North Macedonia. There, excess supply will drive down prices, encouraging additional purchases.