Fairly Priced After Its AI Infrastructure Driven Share Price Run?")

- Investors may be wondering if Marvell Technology at around US$87.91 is offering fair value or stretching expectations, especially after its recent run and the heightened attention on chips and AI infrastructure.

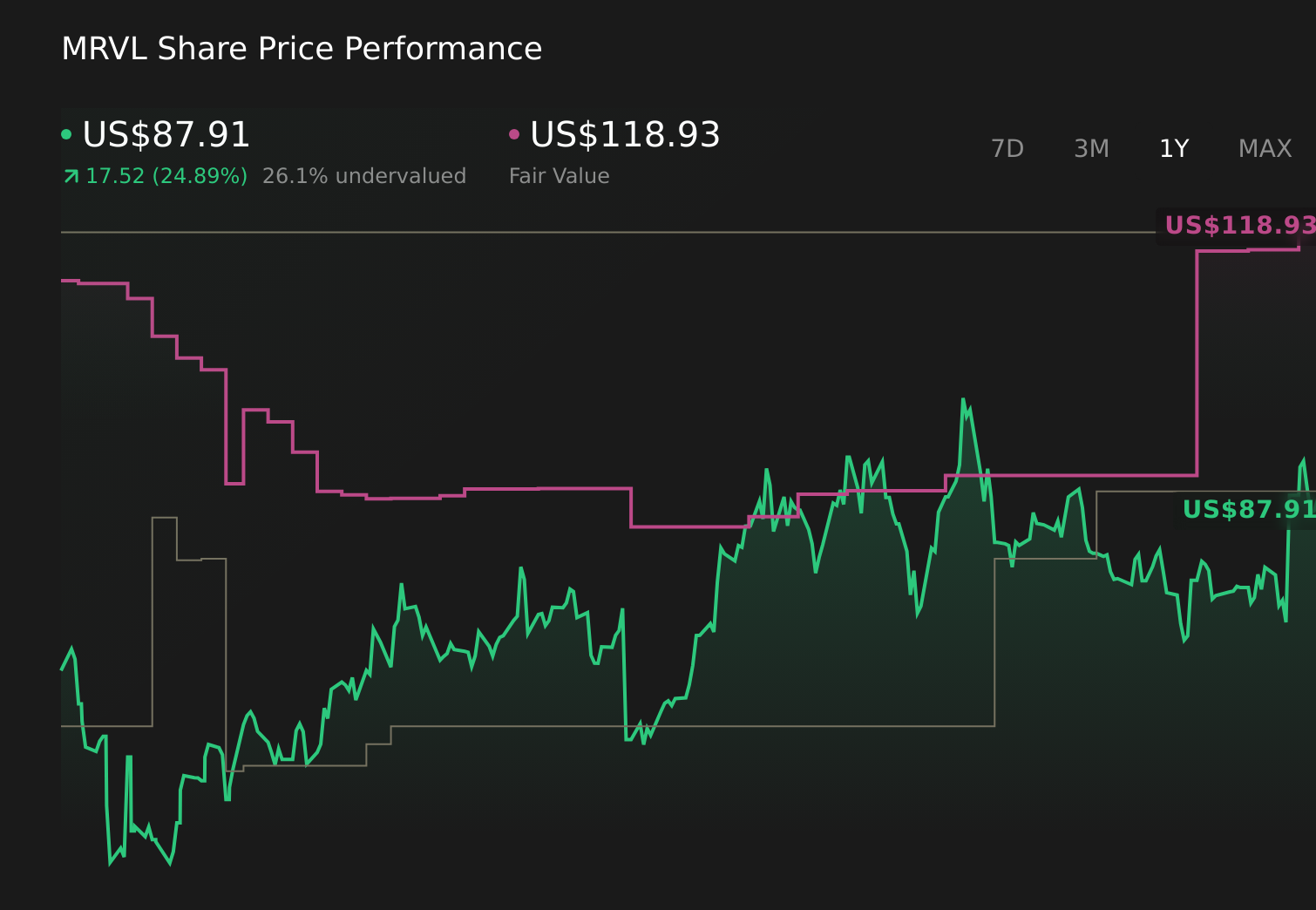

- The stock price sits near US$87.91, with a 0.1% return over 7 days, 11.2% over 30 days, a 1.7% decline year to date, 25.3% over 1 year, 116.4% over 3 years, and 91.0% over 5 years. This performance raises the question of how much of this is already reflected in today’s valuation.

- Recent coverage has kept Marvell in the spotlight as investors reassess semiconductor names, with attention on how companies tied to networking, storage, and AI infrastructure are being priced. This backdrop helps explain why Marvell’s share moves have been closely watched as part of a broader reassessment of chip related opportunities and risks.

- On Simply Wall St’s 6 point valuation checklist, Marvell currently scores a 4. The next sections will break down what different valuation methods say about that number and hint at a more complete way to think about value that goes beyond any single model.

Find out why Marvell Technology’s 25.3% return over the last year is lagging behind its peers.

Approach 1: Marvell Technology Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth today by projecting its future cash flows and then discounting those back into present dollars.

For Marvell Technology, the model used is a 2 Stage Free Cash Flow to Equity approach, based on last twelve months free cash flow of about $1.33b. Analysts provide explicit forecasts for several years, and Simply Wall St then extends those projections further out to build a 10 year cash flow path.

In this case, projected free cash flow rises to $6.38b by the 2031 financial year, with interim years stepping up through the $1b to $5b range. Each of those future cash flows is discounted back to today using an appropriate rate, and then summed to get an estimated equity value.

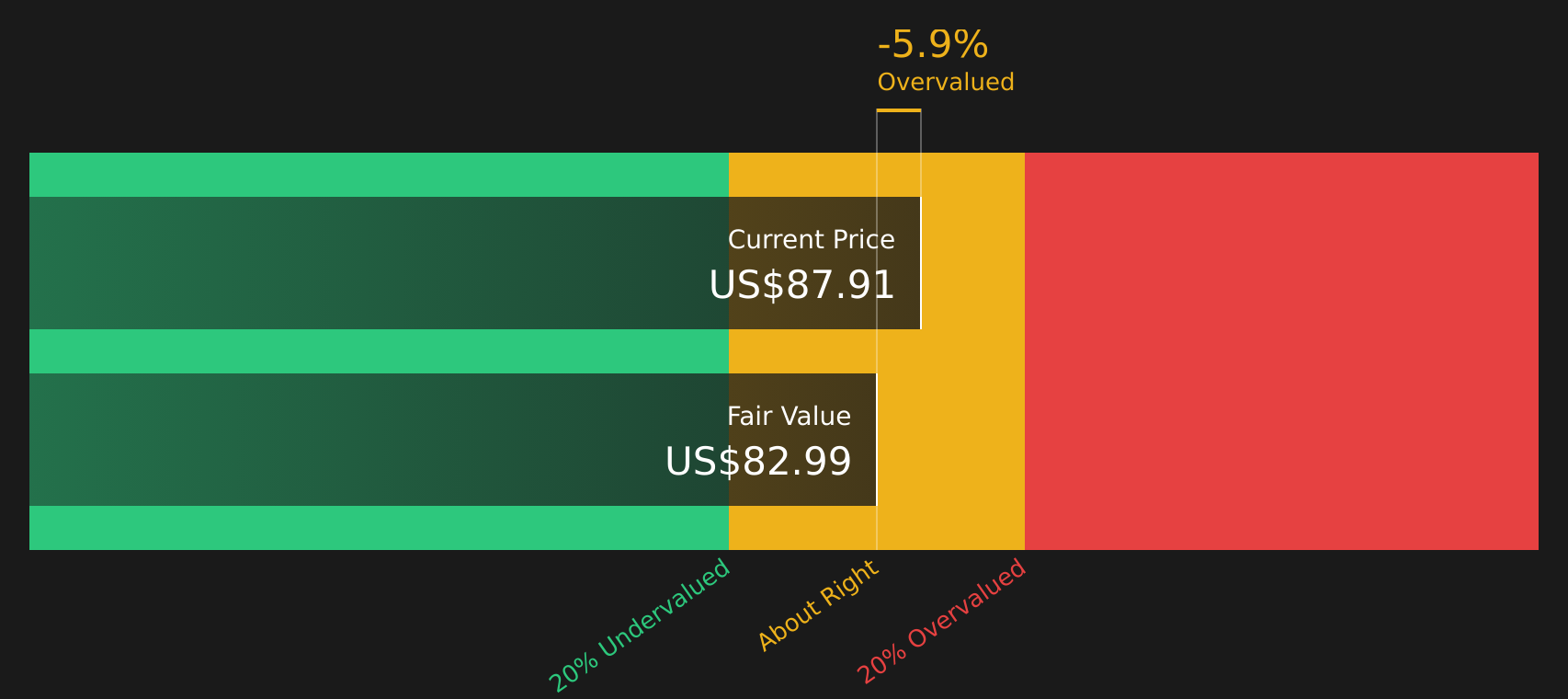

That process results in an intrinsic value estimate of about $82.99 per share, compared with the recent price around $87.91. On this DCF view, Marvell screens as roughly 5.9% overvalued, which is a relatively small gap.

Result: ABOUT RIGHT

Marvell Technology is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment’s notice. Track the value in your watchlist or portfolio and be alerted on when to act.

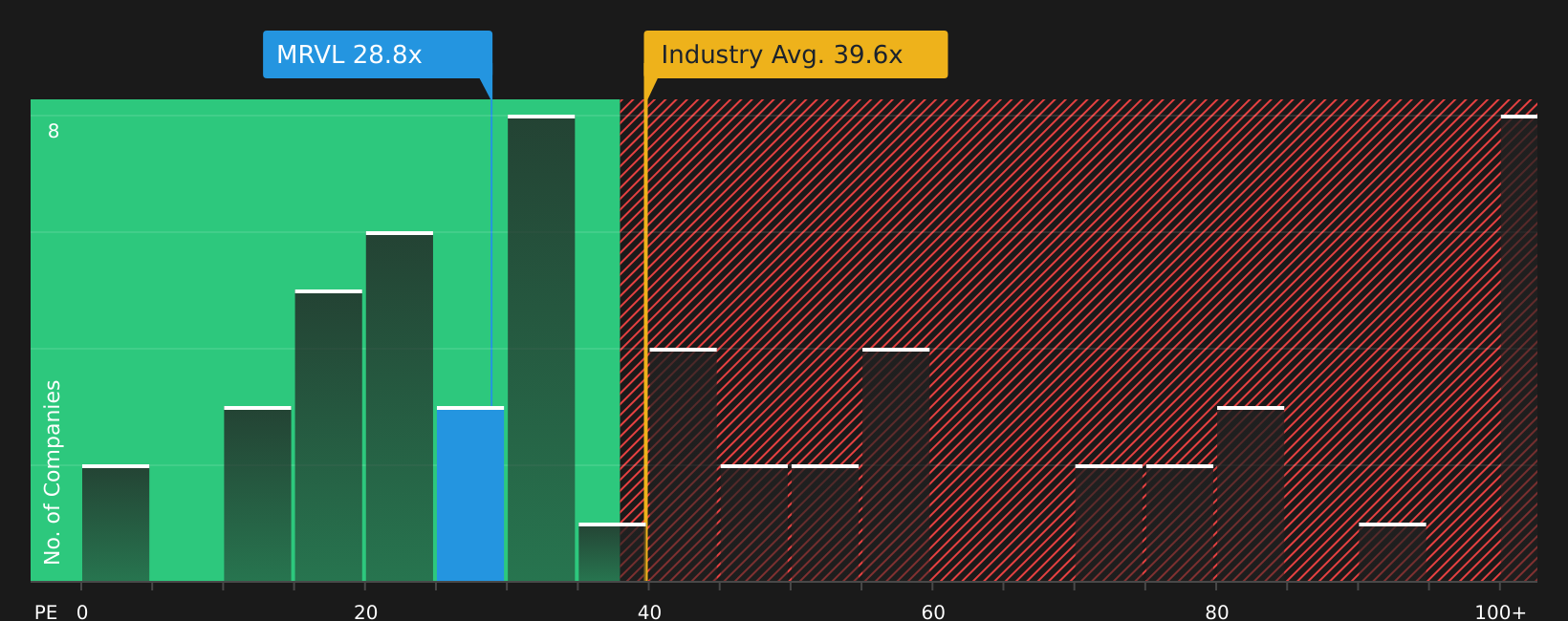

Approach 2: Marvell Technology Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand because it links what you pay for the stock to the earnings the business is already generating. It gives a quick sense of how many dollars investors are currently willing to pay for each dollar of earnings.

What counts as a “normal” or “fair” P/E depends on how fast earnings are expected to grow and how risky those earnings are. Higher expected growth and lower perceived risk can justify a higher P/E, while lower growth or higher risk usually call for a lower multiple.

Marvell Technology currently trades on a P/E of 28.79x. That compares with a Semiconductor industry average P/E of about 39.59x and a peer group average of 77.43x. Simply Wall St also calculates a proprietary “Fair Ratio” of 47.69x, which reflects factors such as Marvell’s earnings growth profile, margins, industry, market cap and risk characteristics. This Fair Ratio is designed to be more tailored than a simple peer or industry comparison because it adjusts for company specific factors instead of assuming all semiconductor names deserve the same multiple. On this view, Marvell’s actual P/E sits below its Fair Ratio, which indicates that the shares may screen as undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Marvell Technology Narrative

Earlier it was mentioned that there is an even better way to think about value, so this is where Narratives come in, giving you a simple way to attach a clear story about Marvell Technology to your own numbers on fair value, future revenue, earnings and margins.

On Simply Wall St’s Community page, Narratives let you connect three pieces in one place: the company story, the forecast that flows from that story, and the fair value that drops out of those assumptions, so you can see in plain sight how your view translates into a number.

Because each Narrative continuously compares its Fair Value to the current share price and refreshes when new information such as news or earnings arrives, it becomes a living reference point that can help you decide whether the stock looks more attractive, less attractive, or somewhere in the middle based on your own framework.

For Marvell, one investor might publish a Narrative that treats it as an “AI data infrastructure architect” with a Fair Value around US$155 per share, while another might share a far more cautious view closer to US$59. Seeing those side by side helps you quickly understand how different assumptions about data center dependence, custom ASIC demand and profitability lead to very different conclusions about what the shares are worth today.

Do you think there’s more to the story for Marvell Technology? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com