Europe Vegetarian Food Market Size

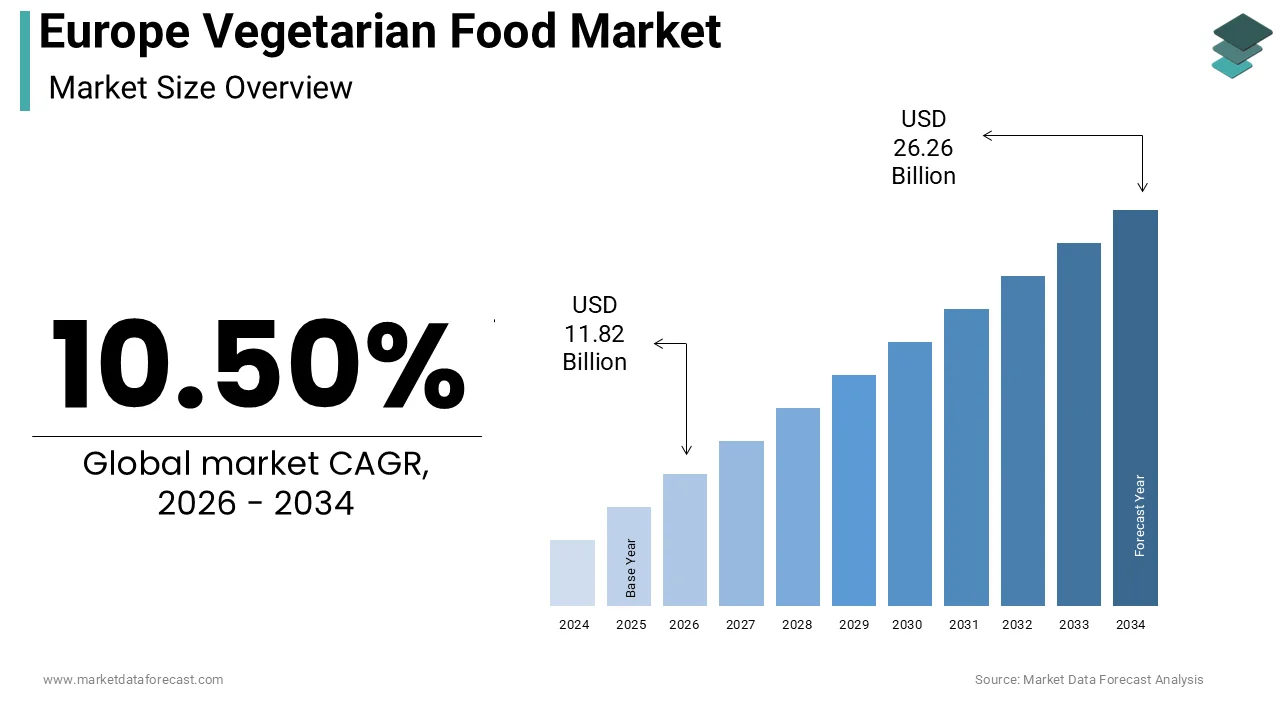

The Europe vegetarian food market size was calculated to be USD 10.69 billion in 2025 and is anticipated to be worth USD 26.26 billion by 2034, from USD 11.82 billion in 2026, growing at a CAGR of 10.50% during the forecast period.

The food products are explicitly formulated without meat, poultry, or fish, ranging from traditional plant-based staples like legumes and grains to sophisticated meat analogues and dairy alternatives. This sector represents a fundamental shift in the European dietary landscape, driven by a convergence of ethical concerns, environmental awareness, and health consciousness. According to the European Commission, the number of citizens identifying as vegetarian or vegan has risen significantly, with recent surveys indicating that approximately 10% of the EU population now adheres to a meat-free diet. The regulatory environment is also evolving, with the European Food Safety Authority establishing guidelines for labeling and nutritional claims to ensure consumer transparency. Furthermore, the European Green Deal emphasizes reducing the carbon footprint of food systems, indirectly bolstering the vegetarian sector, which typically requires fewer resources than animal agriculture.

MARKET DRIVERS Intensifying Environmental Consciousness and Climate Action

The escalating urgency regarding climate change and the environmental impact of animal agriculture is significantly enhancing the growth of Europe vegetarian food market. European consumers are increasingly aware that livestock farming contributes significantly to greenhouse gas emissions, land degradation, and water scarcity by prompting a deliberate shift towards plant-based diets as a form of individual climate action. According to the European Environment Agency, the agricultural sector accounts for nearly 10% of total EU greenhouse gas emissions, with livestock production being a major contributor, a statistic widely disseminated through media and educational campaigns. Data from a comprehensive survey by the European Consumer Organisation reveals that many European shoppers consider the environmental footprint of their food when making purchasing decisions, directly correlating with increased sales of vegetarian products. As per the World Resources Institute, shifting to plant-based diets could reduce food-related emissions by up to 70%, a fact that resonates deeply with the eco-conscious demographic in nations like Germany and Sweden. Retailers are responding by highlighting the carbon savings of vegetarian items on packaging, further validating the consumer choice.

Rising Prevalence of Lifestyle Diseases and Health Awareness

The growing incidence of lifestyle-related diseases such as obesity, cardiovascular conditions, and type 2 diabetes across Europe is driving a substantial surge in the demand for vegetarian food products perceived as healthier alternatives. Consumers are actively seeking diets rich in fiber, vitamins, and phytonutrients while avoiding saturated fats and cholesterol, often associated with red and processed meats. According to the World Health Organization Regional Office for Europe, more than 59% of adults in the European region are overweight or obese, a crisis that has spurred public health campaigns promoting plant-based nutrition as a preventive measure. Medical associations across the continent increasingly endorse vegetarian diets for their potential to lower blood pressure and improve metabolic health, lending scientific credibility to consumer choices. Supermarkets and food manufacturers are capitalizing on this trend by fortifying vegetarian products with essential nutrients like vitamin B12 and iron, addressing potential deficiencies and enhancing their health appeal.

MARKET RESTRAINTS High Cost of Processed Plant-Based Alternatives

The significantly higher price point of processed vegetarian meat and dairy alternatives compared to their conventional animal-based counterparts, among price-sensitive consumers, is restraining the growth of Europe vegetarian food market. Despite the long-term cost benefits of whole plant foods, the specialized processing, ingredient sourcing, and smaller scale of production for meat analogues result in premium retail prices that limit accessibility. According to the European Commission’s Joint Research Centre, the average price of plant-based meat substitutes remains approximately 40% higher than equivalent minced meat products, creating a financial barrier for widespread adoption during periods of economic uncertainty. The food inflation in the Eurozone has exacerbated this gap, with households prioritizing essential staples over premium alternative proteins as disposable incomes shrink. As per the European Consumer Organisation, respondents cited price as the main obstacle preventing them from purchasing vegetarian alternatives more frequently, even when they express a desire to reduce meat consumption. This cost disparity forces many consumers to revert to cheaper animal proteins or unprocessed vegetables by stalling the growth of the value-added vegetarian segment.

Sensory Limitations and Texture Dissatisfaction

The persistent issues regarding the sensory profile, specifically texture and taste, of certain vegetarian products continue to hinder repeat purchases and broader acceptance among mainstream consumers who are accustomed to the mouthfeel of animal meat. While technology has advanced, many plant-based alternatives still fail to perfectly replicate the juiciness, fibrous structure, and flavor complexity of real meat, leading to disappointment and skepticism among trial users. According to a study published by the European Journal of Clinical Nutrition, sensory dissatisfaction is reported by nearly 30% of flexitarian consumers who have tried plant-based meats, with texture being the most common complaint affecting their willingness to repurchase. As per the European Food Safety Authority, the challenge lies in mimicking the intricate protein matrix of animal muscle using plant proteins like pea or soy, which often results in a mushy or overly processed mouthfeel. This sensory gap is particularly pronounced in whole-cut analogues and traditional dishes where texture is paramount.

MARKET OPPORTUNITIES Innovation in Fermentation and Precision Protein Technologies

The advent of advanced fermentation techniques and precision fermentation to overcome current limitations in taste, texture, and nutritional profile is substantially creating new opportunities for the growth of Europe’s vegetarian food market. These cutting-edge technologies enable the production of specific proteins, fats, and enzymes that are identical to those found in animal products but derived from microbial cultures by allowing for the creation of superior meat and dairy analogues. According to the European Federation of Biotechnology, investment in fermentation-based food startups in Europe has surged in the last two years, signaling strong industry confidence in this technological pathway. As per the European Commission’s Horizon Europe program, significant funding is being allocated to research projects focused on scalable biomass fermentation to enhance the sustainability and efficiency of protein production. This innovation allows manufacturers to create products with cleaner labels, improved amino acid profiles, and textures that closely mimic animal muscle fibers, appealing to discerning consumers.

Expansion of Vegetarian Options in Food Service and Hospitality

The strategic expansion of vegetarian offerings within the food service sector, including restaurants, cafes, and institutional catering to normalize plant-based dining and drive mass adoption, is another attribute to pose new opportunities for the growth of Europe’s vegetarian food market. As dining out and convenience become central to modern European lifestyles, the availability of appealing vegetarian meals in these settings plays a crucial role in influencing consumer behavior and trial rates. Data from the Sustainable Restaurant Association indicates that venues offering diverse and creative vegetarian options see an increase in customer footfall among younger demographics, who prioritize ethical dining. As per the European School Meals Network, several countries are implementing policies to mandate at least one vegetarian meal option daily in school canteens, exposing millions of children to plant-based foods from a young age and shaping future preferences. This institutional integration not only drives volume but also helps dismantle the perception of vegetarian food as niche or inferior.

MARKET CHALLENGES Regulatory Ambiguity and Labeling Restrictions

The regulatory ambiguity and restrictive labeling laws that limit how plant-based products are described to consumers are a new challenge for the growth of Europe vegetarian food market. Ongoing debates and varying national interpretations regarding the use of dairy-related terms like “milk,” “cheese,” or “yogurt” for plant-based alternatives create confusion and hinder effective communication of product attributes. According to the European Court of Justice, rulings have strictly prohibited the use of protected designations of origin and dairy terms for purely plant-based products by forcing manufacturers to adopt less intuitive labeling that may dilute brand recognition. As per the inconsistent labeling regulations across member states complicate cross-border trade and strategies, increasing compliance costs for producers. As per the European Commission, proposed updates to food information regulations continue to spark contention between traditional livestock lobbies and the plant-based sector by creating an environment of uncertainty that discourages investment.

Supply Chain Vulnerability and Raw Material Volatility

The reliance on specific agricultural commodities such as peas, soy, and oats for vegetarian food production exposes it to supply chain vulnerabilities and price volatility driven by climate change and geopolitical instability. This factor is also expected to degrade the growth of Europe vegetarian food market. Extreme weather events, pests, and crop failures in key growing regions can disrupt the availability of high-quality plant proteins by leading to production delays and cost spikes for manufacturers. According to the Joint Research Centre of the European Commission, climate variability has already impacted yields of key protein crops in Europe, with some regions experiencing production drops in recent years. As per the European Farmers and Agri-Cooperatives Association, the lack of diversified domestic sourcing options forces many manufacturers to depend on imports, increasing exposure to logistical and trade barriers. This fragility complicates long-term planning and pricing strategies, making it difficult to maintain consistent product availability and affordability. Strengthening the resilience of the supply chain through localized farming initiatives and diversified sourcing strategies remains a critical hurdle for the industry to ensure stable growth and consumer trust.

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

10.50%

Segments Covered

By Product, Distribution Channel, And Region

Various Analyses Covered

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

Nestlé S.A., Unilever PLC, Danone S.A., Beyond Meat Inc., Impossible Foods Inc., Quorn Foods Ltd, Amy’s Kitchen Inc., Kellogg Company, The Hain Celestial Group Inc., Oatly Group AB, Alpro (Danone), Vivera BV, Garden Gourmet (Nestlé), Linda McCartney Foods Ltd, Meatless Farm Co.

SEGMENTAL ANALYSIS By Product Insights

The vegan meat and seafood segment was the largest by holding 32.1% of the Europe vegetarian food market share in 2025, with the ability to directly substitute animal protein in traditional European dishes, thereby appealing to the massive flexitarian demographic rather than just strict vegetarians. The rapid technological advancement in texturization that allows plant-based proteins to mimic the fibrous texture and juiciness of real meat by overcoming previous sensory barriers. According to the Good Food Institute Europe, sales of plant-based meat alternatives grew by 12% in volume despite economic headwinds, indicating a structural shift in consumer preference towards direct meat replacements. Data from the European Plant-Based Foods Association reveals that many plant-based meat buyers in Europe are flexitarians, who actively seek products that integrate seamlessly into familiar recipes like burgers, bolognese, and stews without requiring culinary adaptation. Furthermore, the extensive distribution of these products in mainstream butcher sections and freezer aisles of major supermarket chains has normalized their consumption. This deep integration into the core protein category ensures that vegan meat and seafood remain the revenue engine of the broader vegetarian market.

The protein liquids and powders segment is expected to witness the fastest CAGR of 9.8% during the forecast period, with the emergence of the sports nutrition industry with mainstream wellness trends, where consumers increasingly seek convenient, plant-based sources of protein for muscle recovery and general health. The rising awareness among European consumers is that plant proteins such as pea, rice, and hemp offer complete amino acid profiles comparable to whey, but with better digestibility and lower environmental impact. Data from Euromonitor International indicates that ready-to-drink protein shakes featuring plant-based ingredients have seen a volume growth, as busy urban professionals prioritize convenience and on-the-go nutrition. As per the European Food Safety Authority, the approval of specific health claims related to muscle mass maintenance for plant proteins has further legitimized these products in the eyes of health-conscious shoppers. The versatility of protein powders allows them to be incorporated into smoothies, baking, and oatmeal, expanding their usage occasions beyond post-workout recovery.

By Distribution Channel Insights

The offline retail segment was the largest by holding a significant share of the Europe vegetarian food market in 2025, with the entrenched habit of European consumers to purchase fresh and frozen food items through physical supermarkets, hypermarkets, and discount stores where they can inspect product quality and expiration dates personally. According to the European Retail Round Table, over 85% of grocery transactions in Europe still occur in physical stores, with large chains like Carrefour, Tesco, and Rewe dedicating significant shelf space to plant-based ranges to capture the growing flexitarian traffic. Data from the Sustainable Restaurant Association shows that in-store promotions and tasting events for new vegetarian products significantly boost trial rates, a marketing advantage that offline channels possess over digital platforms. As per the European Consumer Organisation, trust in food safety and freshness remains higher for physical retail, particularly for perishable items like plant-based meats and dairy alternatives, which require strict cold chain management that consumers prefer to verify visually.

The online retail segment is anticipated to grow at a CAGR of 14.5% during the forecast period wth the shifting consumer behavior towards digital grocery shopping, accelerated by pandemic habits and the increasing sophistication of e-commerce logistics offering same-day or next-day delivery. The ability of online platforms to offer a vastly wider assortment of niche, specialty, and international vegetarian products that are often unavailable in local physical stores, catering to specific dietary needs and culinary curiosities. According to Eurostat, the proportion of Europeans ordering food and groceries online has doubled in the last three years, with younger demographics leading this transition towards digital procurement. As per McKinsey and Company, personalized algorithms on grocery apps effectively recommend vegetarian alternatives to shoppers based on their purchase history, driving cross-selling opportunities that are difficult to replicate in physical aisles. The convenience of comparing prices, reading detailed ingredient lists, and accessing user reviews before purchasing also empowers consumers to make informed choices aligned with their ethical and health values.

REGIONAL ANALYSIS Germany Vegetarian Food Market Analysis

Germany was the largest contributor to the Europe vegetarian market by holding 26.3% of the market share in 2025, with a deeply ingrained culture of environmentalism and a high concentration of vegetarians and vegans. The strong influence of political and social movements advocating for sustainable agriculture, which has led to government subsidies for plant-based innovation and clear labeling standards, is a major factor in the growth of Europe’s vegetarian food market. According to the Federal Ministry of Food and Agriculture, the number of Germans identifying as vegetarian has reached nearly 8 million, representing one of the highest per capita rates globally. As per the study, sales of frozen plant-based meals have grown by 20% annually, reflecting the busy lifestyles of consumers seeking convenient, ethical options. The presence of major homegrown brands and a robust network of organic food stores further strengthens the ecosystem.

United Kingdom Vegetarian Food Market Analysis

The United Kingdom was ranked second by holding 21.2% of the Europe vegetarian food market share in 202,5 with a highly innovative food technology sector and a diverse multicultural population. Also, the aggressive commitment by major restaurant chains and fast-food outlets to include popular plant-based items on their core menus is normalizing vegetarian dining for the mass market. Data from the British Retail Consortium shows that the “Vegan Society” trademarked products have seen sales growth, indicating strong consumer trust in certified items. As per the Food Standards Agency, clear allergen and ingredient labeling regulations have boosted consumer confidence in trying new vegetarian formats. The rise of “flexitarianism” is particularly pronounced in the UK, with millions of consumers actively reducing meat intake without fully abandoning it, creating a massive addressable market.

France Vegetarian Food Market Analysis

France’s vegetarian food market is anticipated to have a significant growth opportunity in the coming years, which is slowly embracing plant-based interpretations of its rich gastronomic traditions. According to FranceAgriMer, the consumption of plant-based proteins in France has increased over the last four years, which is signaling a break from traditional meat-heavy eating habits. As per the French Agency for Ecological Transition, the link between meat consumption and climate change has resonated strongly with urban populations in Paris and Lyon. The emergence of local startups focusing on fermentation and high-quality ingredients is also reshaping the supply side.

Italy Vegetarian Food Market Analysis

Italy’s vegetarian food market growth is leveraging its historical reliance on Mediterranean vegetables, legumes, and grains, which naturally align with vegetarian principles. Italy is marked by a seamless integration of modern plant-based alternatives into a cuisine that already celebrates vegetables, making the transition easier for consumers compared to other regions. According to the Italian National Institute of Statistics, the sales of plant-based dairy alternatives, particularly oat and soy milks, are driven by high lactose intolerance rates in the population. Data from the Italian Association of Food Industries indicates that the pasta and pizza sectors are increasingly incorporating plant-based toppings and fillings to cater to changing consumer demands in both retail and food service. As per the Coldiretti farmers’ association, there is a growing movement to source ingredients locally for plant-based production, emphasizing sustainability and reduced food miles.

Spain Vegetarian Food Market Analysis

Spain’s vegetarian food market is likely to grow with a vibrant food service industry and a growing awareness of health and sustainability among its population. The massive tourism industry, which creates immense demand for diverse and inclusive dining options in hotels and restaurants along the Mediterranean coast, pushing chefs to innovate with plant-based ingredients, is also propelling the growth of the market in this country. According to the Spanish Ministry of Agriculture, Fisheries, and Food, the import and production of plant-based meat alternatives have doubled in the last three years to meet the rising domestic and tourist demand. As per the Spanish Nutrition Foundation, public health campaigns promoting the benefits of the Mediterranean diet, which is naturally plant-forward, have reinforced the validity of vegetarian choices. The warm climate also supports the year-round availability of fresh produce, complementing the processed vegetarian sector.

COMPETITION OVERVIEW

The competition in the Europe vegetarian food market is characterized by intense rivalry between established multinational food conglomerates and agile specialized startups, who are all vying for dominance in the rapidly expanding plant-based sector. The market landscape features a diverse array of competitors, ranging from traditional meat processors diversifying their portfolios to dedicated vegan brands innovating with novel ingredients like fungi and algae. Differentiation frequently hinges on the ability to deliver superior sensory experiences that closely mimic animal products while maintaining clean labels and sustainable sourcing practices. Price competition is becoming increasingly fierce as larger players leverage economies of scale to lower costs and challenge the premium pricing of niche brands. Supply chain reliability and the capacity to meet surging demand during promotional periods are also critical battlegrounds where companies strive to prove their operational excellence. The entry of private label, ranging from major supermarket chains, adds another layer of complexity by offering affordable alternatives that pressure branded manufacturers to justify their value propositions.

KEY MARKET PLAYERS

A few major players of the Europe vegetarian food market include

- Nestlé S.A

- Unilever PLC

- Danone S.A

- Beyond Meat Inc

- Impossible Foods Inc

- Quorn Foods Ltd

- Amy’s Kitchen Inc

- Kellogg Company

- The Hain Celestial Group Inc

- Oatly Group AB

- Alpro (Danone)

- Vivera BV

- Garden Gourmet (Nestlé)

- Linda McCartney Foods Ltd

- Meatless Farm Co

Top Strategies Used by Key Market Participants

Key players in the Europe vegetarian food market primarily employ strategies focused on product innovation and sensory enhancement to attract flexitarian consumers who demand taste and texture parity with animal-based foods. Companies are increasingly investing in research and development to utilize fermentation and extrusion technologies that improve the mouthfeel and flavor profiles of plant-based meats and dairy alternatives. Securing strategic partnerships with major fast food chains and restaurant groups is another critical strategy used to normalize vegetarian dining and reach mass audiences through familiar menu items. Expansion of production capabilities within Europe is also a common approach to reduce logistics costs, ensure supply chain resilience, and respond quickly to local market trends. Furthermore, participants are leveraging clean label initiatives and sustainability certifications to build trust and differentiate their brands in a crowded marketplace where environmental impact is a key purchasing driver for European shoppers.

Leading Players in the Europe Vegetarian Food Market

- The Vegetarian Butcher operates as a pioneering force in the Europe vegetarian food market with a specific focus on replicating the texture and taste of whole cut meats using plant-based ingredients. The company has made significant contributions to the global market by demonstrating that vegetarian options can satisfy hardcore meat eaters through its unique fermentation and texturization techniques. Recently, the brand strengthened its position by expanding its production capacity within the Netherlands to meet surging European demand and by launching new product lines such as plant-based chicken nuggets and beef mince in major retail chains across the continent. Their strategic partnership with quick-service restaurant giants has further solidified their presence in the food service sector, allowing them to introduce vegetarian burgers and sandwiches to millions of customers daily.

- Upfield stands as a global leader in the plant-based dairy alternative sector, particularly known for its extensive portfolio of spreads, cheeses, and cooking creams under various well-known brands. The company contributes significantly to the global market by driving innovation in fat technology to create dairy-free products that melt, spread, and taste like traditional cow milk derivatives without compromising on health benefits. Recent actions to strengthen their market position include the acquisition of specialized fermentation startups to enhance the flavor profiles of their cheese alternatives and the rollout of carbon-neutral labeling across their European product range to appeal to environmentally conscious shoppers. They have also invested heavily in marketing campaigns that highlight the lower saturated fat content of their offerings compared to dairy, thereby attracting health-focused demographics.

- Nestlé leverages its massive global resources and distribution network to play a pivotal role in the Europe vegetarian food market through its dedicated Garden Gourmet and Vemondo brands. The company contributes to the global landscape by utilizing its advanced research and development facilities to create high-quality plant-based meats and dairy alternatives that cater to diverse regional taste preferences across Europe. To strengthen its market position, Nestlé has recently expanded its manufacturing facilities in Germany and Switzerland to increase production output and reduce lead times for retailers. They have also launched innovative product formats such as plant-based fish sticks and whole cut steaks that address specific gaps in the current market offering. Furthermore, their commitment to sourcing sustainable raw materials and achieving net zero emissions aligns with European regulatory goals and consumer values. These strategic moves enable Nestlé to maintain a competitive edge by offering a wide variety of trusted and delicious vegetarian options that are readily available in virtually every corner of the European food retail and service sectors.

MARKET SEGMENTATION

This research report on the Europe vegetarian food market has been segmented and sub-segmented based on product, distribution channel & region.

By Product

- Vegan Meat & Seafood

- Creamer

- Yogurt

- Cheese

- Butter

- Meals

- Protein liquids and powders

- Protein Bars

By Distribution channel

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe