Valuation As Mixed Returns And DCF Signals Draw Attention")

Recent trading in OGE Energy (OGE) has brought the stock back into focus, with short term returns mixed across the past week and month while longer periods show different patterns for shareholders.

See our latest analysis for OGE Energy.

At a share price of US$47.54, OGE Energy has recently seen a mix of short term moves and stronger medium term momentum, with a 90 day share price return of 10.82% alongside a 1 year total shareholder return of 8.61% and a 5 year total shareholder return of 81.74%.

If you are looking beyond utilities for what is working in the market right now, it could be a good time to scan for 26 power grid technology and infrastructure stocks

With OGE Energy trading near analysts’ price targets and an intrinsic value estimate that sits well below the current share price, the key question is whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 1.4% Undervalued

OGE Energy’s most followed valuation narrative pegs fair value at about $48.23 per share, only slightly above the last close of $47.54, which keeps expectations tight.

Ongoing and planned investments in generation capacity and transmission infrastructure, with legislative and regulatory support (e.g., CWIP and PISA mechanisms), enable accelerated asset deployment with minimized lag in rate recovery, supporting consistent future earnings and improved return on equity. Federal and state policies focused on grid modernization and reliability, as well as incentives for infrastructure investment, underpin OGE’s ability to secure cost recovery on capital projects, enhancing long-term profitability and margin stability.

Want to know what keeps that fair value so close to today’s price? The narrative leans on steady revenue expansion, firmer margins, and a future earnings multiple that has to stretch just enough to make the math work.

Result: Fair Value of $48.23 (ABOUT RIGHT)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, this story can change quickly if industrial and oilfield demand stays weak, or if higher interest costs on new projects start to pressure margins.

Find out about the key risks to this OGE Energy narrative.

Another View: Cash Flows Paint A Tougher Picture

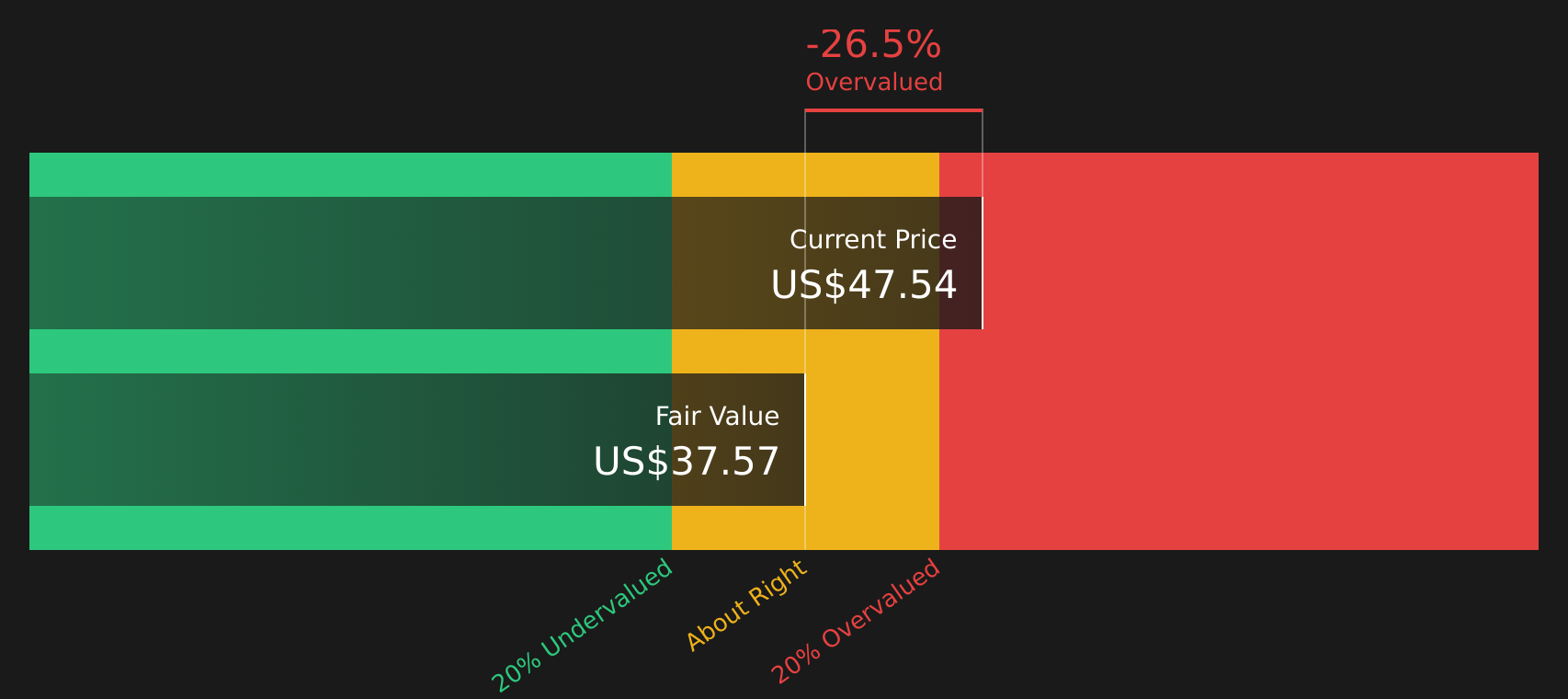

While the prevailing narrative sits near a fair value of about $48.23 per share, the Simply Wall St DCF model points in a different direction. On that cash flow view, OGE Energy’s estimated value is $37.57, which makes the current $47.54 price look expensive rather than slightly undervalued. When the gap is this wide, which yardstick do you trust more?

Look into how the SWS DCF model arrives at its fair value.

OGE Discounted Cash Flow as at Mar 2026

OGE Discounted Cash Flow as at Mar 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OGE Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

Mixed messages on value can create hesitation. Check the numbers yourself and make a call that fits your approach by weighing the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

Do not stop with a single stock. Apply the same discipline across the market and identify opportunities that fit your goals before others focus on them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com