For Its Upcoming Dividend")

Readers hoping to buy Swiss Re AG (VTX:SREN) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is usually set to be two business days before the record date, which is the cut-off date on which you must be present on the company’s books as a shareholder in order to receive the dividend. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company’s books on the record date. Accordingly, Swiss Re investors that purchase the stock on or after the 14th of April will not receive the dividend, which will be paid on the 16th of April.

The company’s next dividend payment will be US$8.00 per share, on the back of last year when the company paid a total of US$8.00 to shareholders. Based on the last year’s worth of payments, Swiss Re stock has a trailing yield of around 4.8% on the current share price of CHF0132.60. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. As a result, readers should always check whether Swiss Re has been able to grow its dividends, or if the dividend might be cut.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Swiss Re is paying out an acceptable 51% of its profit, a common payout level among most companies.

When a company paid out less in dividends than it earned in profit, this generally suggests its dividend is affordable. The lower the % of its profit that it pays out, the greater the margin of safety for the dividend if the business enters a downturn.

See our latest analysis for Swiss Re

Click here to see the company’s payout ratio, plus analyst estimates of its future dividends.

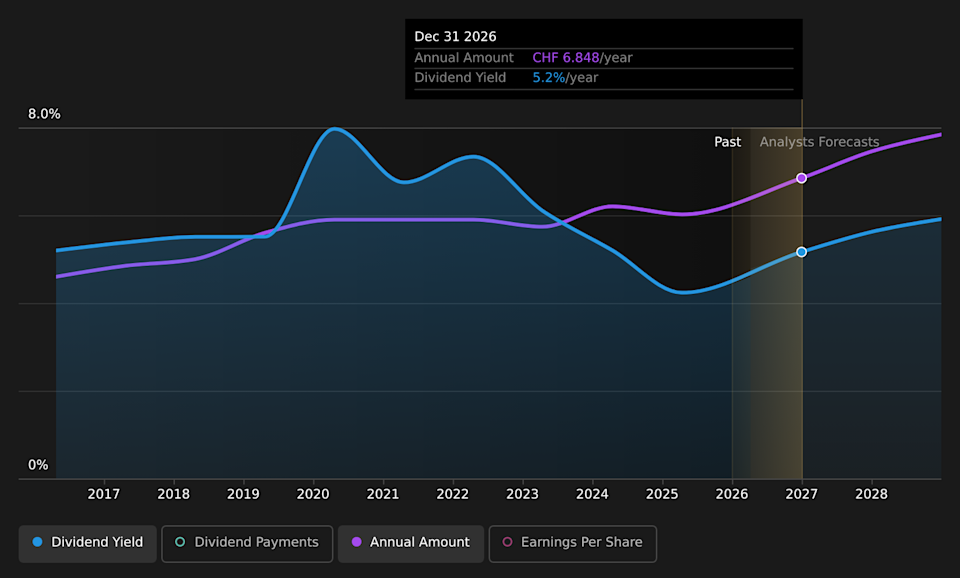

SWX:SREN Historic Dividend April 9th 2026

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. It’s encouraging to see Swiss Re has grown its earnings rapidly, up 43% a year for the past five years.

Many investors will assess a company’s dividend performance by evaluating how much the dividend payments have changed over time. In the past 10 years, Swiss Re has increased its dividend at approximately 5.7% a year on average. Earnings per share have been growing much quicker than dividends, potentially because Swiss Re is keeping back more of its profits to grow the business.