- Liberty Energy (NYSE:LBRT) reported quarterly revenue that exceeded analyst expectations by 16.3%, the largest beat in the oilfield services group.

- Management linked the result to technology driven service offerings and strong operational execution across its fleet.

- The performance marks a fresh operational milestone that has not been addressed in earlier coverage focused on valuation and financing.

Liberty Energy operates in the oilfield services space, providing completion and related services to upstream producers that rely on efficient, technology supported operations. The latest quarter comes at a time when producers continue to focus on capital discipline and cost efficiency, which can put service providers that offer reliable execution and differentiated technology in a stronger competitive position.

For you as an investor, a central question is how repeatable this kind of outperformance may be, given industry cycles and customer spending patterns. The recent result adds another data point on Liberty Energy’s operating profile that can be weighed alongside factors such as balance sheet strength, contract visibility, and how its technology offering compares with other oilfield service peers.

Stay updated on the most important news stories for Liberty Energy by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Liberty Energy.

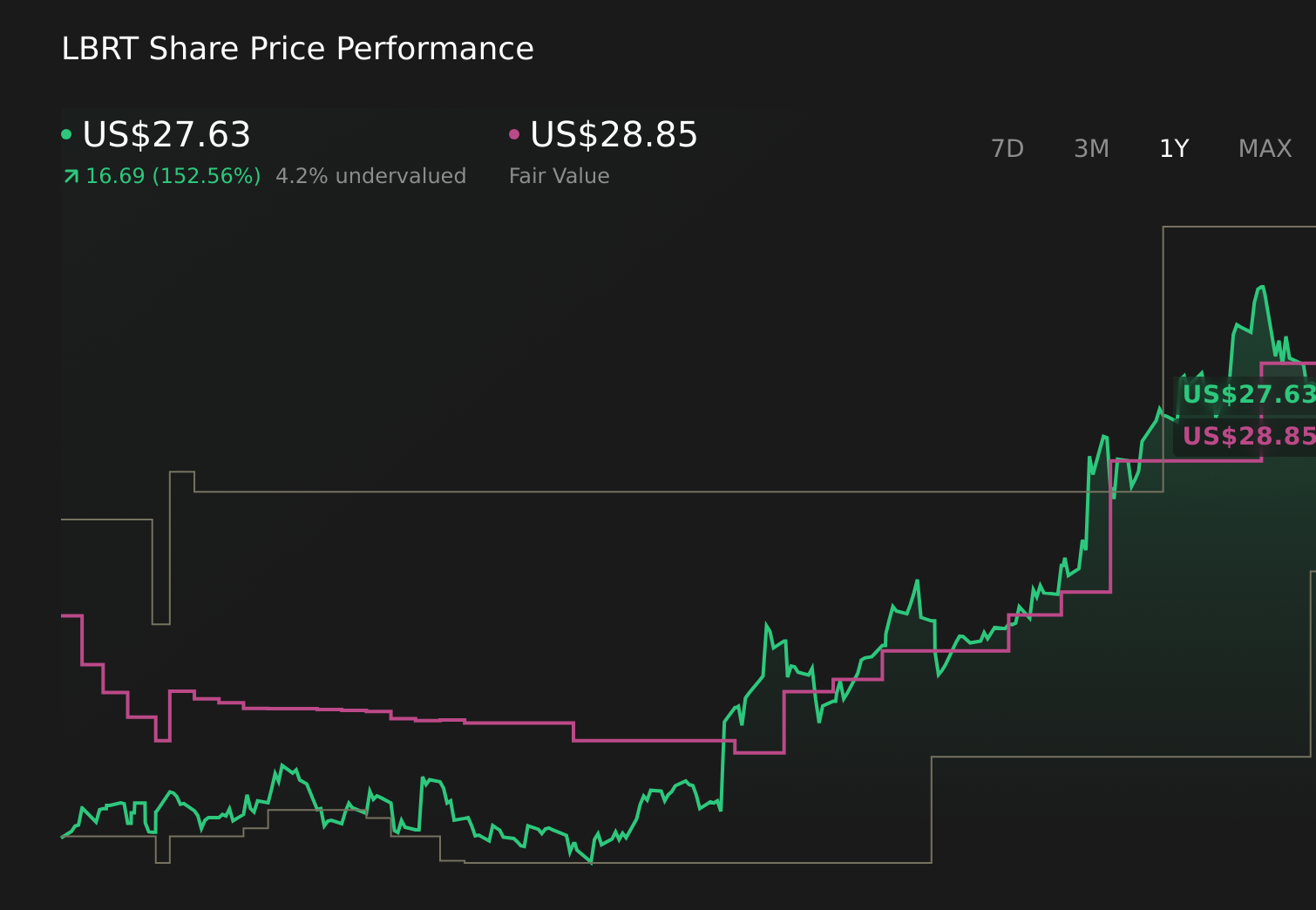

NYSE:LBRT 1-Year Stock Price Chart

NYSE:LBRT 1-Year Stock Price Chart

See which insiders are buying and buying and selling Liberty Energy following this latest news.

Quick Assessment

- ⚖️ Price vs Analyst Target: The current price of $27.63 is around 5% below the US$29.00 analyst target, so it sits inside the typical target range.

- ✅ Simply Wall St Valuation: Shares are flagged as trading at roughly 81.5% below one fair value estimate, which screens as materially undervalued.

- ❌ Recent Momentum: The 30 day return of about 7.7% decline shows recent price pressure despite the revenue beat.

There is only one way to know the right time to buy, sell or hold Liberty Energy. Head to Simply Wall St’s

company report for the latest analysis of Liberty Energy’s Fair Value.

Key Considerations

- 📊 The 16.3% revenue beat, tied to technology supported services and execution, gives you an extra data point on how the business is competing for completion work.

- 📊 Watch how margins evolve from the current 3.7%, especially given the earlier 7.3% level and the current P/E of about 30.3 versus the sector at roughly 25.8.

- ⚠️ Forecast earnings declines and recent insider selling sit alongside this strong quarter, so it is worth weighing whether the latest result is sustainable.

Dig Deeper

For the full picture including more risks and rewards, check out the

complete Liberty Energy analysis. Alternatively, you can check out the

community page for Liberty Energy to see how other investors believe this latest news will impact the company’s narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com