Valuation After DOJ Antitrust Settlement And Analyst Support")

Live Nation Entertainment (LYV) has just resolved a U.S. Department of Justice antitrust lawsuit, accepting operational changes that remove the threat of a structural breakup and have helped support recent stock gains.

See our latest analysis for Live Nation Entertainment.

The DOJ settlement has come alongside a strong run in the stock, with a 9.9% five day share price gain reported recently and a 90 day share price return of 9.94% at a last close of $160.59. Over a longer horizon, the 1 year total shareholder return of 23.91% and 3 year total shareholder return of 132.87% point to sustained momentum, even though some recent commentary has questioned the valuation.

If this kind of regulatory and growth story has your attention, it can be helpful to see what else is moving in related areas. A useful starting point is 19 top founder-led companies

With Live Nation now past a major DOJ overhang, a market cap of about US$38.0b and the stock trading below the average analyst price target, the key question is clear: is there still upside, or is recent growth already priced in?

Most Popular Narrative: 12.7% Undervalued

Live Nation Entertainment’s most followed valuation story currently points to a fair value of $184.04 per share, compared with a last close of $160.59. This puts the DOJ settlement into context as just one piece of a broader growth and profitability thesis.

Continued focus on vertical integration, especially in global venue development and operation, allows Live Nation to capture a greater share of the event value chain, facilitates operational efficiency, and enhances ancillary revenues (e.g., sponsorships, food and beverage, VIP packages), directly benefiting net margins and overall earnings.

Curious what has to happen for that valuation to hold up? Revenue expansion, margin rebuild, and a demanding future earnings multiple all sit at the core. The full narrative lays out how those moving pieces fit together without assuming they all break right.

Result: Fair Value of $184.04 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the narrative can still be challenged if regulatory actions around Ticketmaster tighten further or if concert and venue investments fail to earn back their heavy capex.

Find out about the key risks to this Live Nation Entertainment narrative.

Another Angle on Valuation

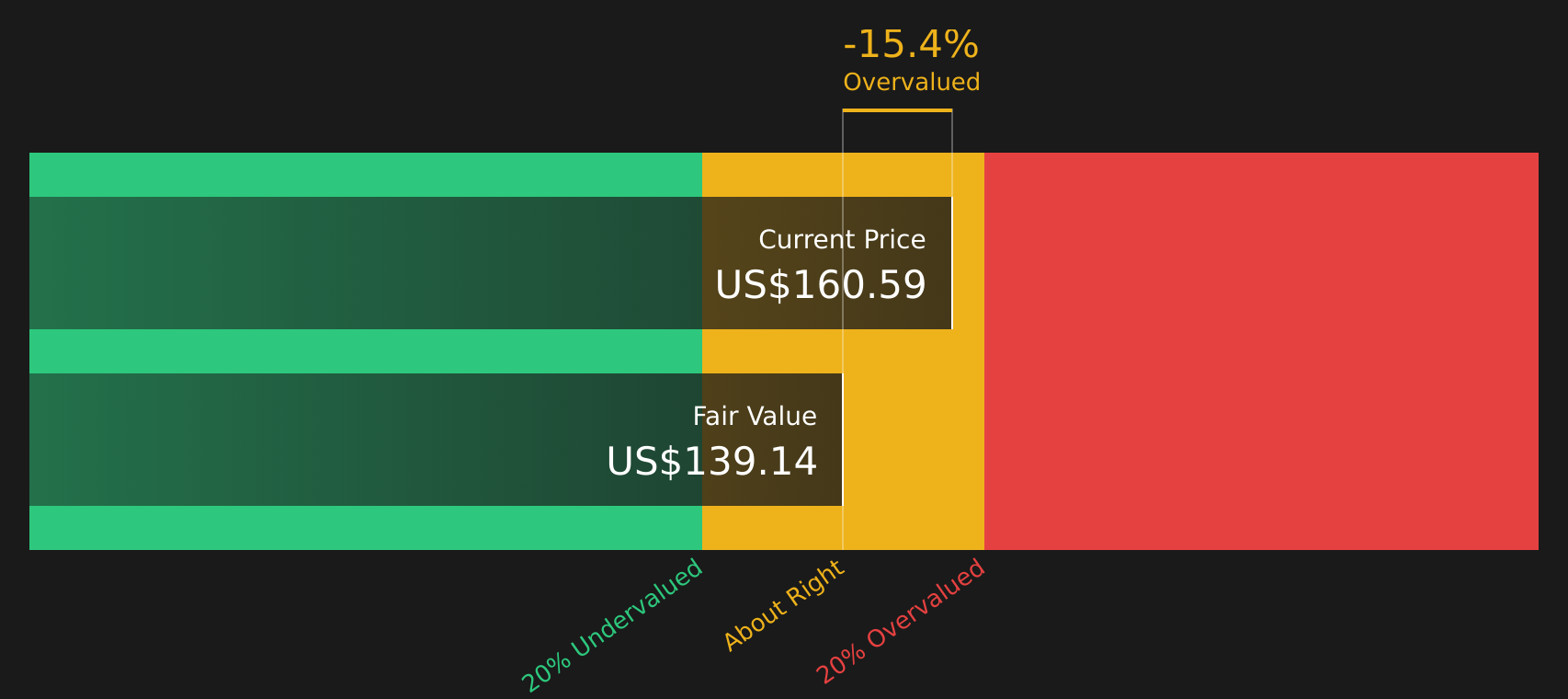

The popular story says Live Nation Entertainment is about 12.7% undervalued at $160.59 versus a fair value of $184.04. Our DCF model is more cautious, with a future cash flow value of $139.14, which points to an overvalued stock instead. Which set of assumptions do you think is closer to reality?

Look into how the SWS DCF model arrives at its fair value.

LYV Discounted Cash Flow as at Apr 2026Next Steps

LYV Discounted Cash Flow as at Apr 2026Next Steps

With all this in mind, are you leaning toward the optimistic side of the Live Nation story or staying cautious? If rewards are catching your eye, take a closer look at the 1 key reward.

Looking for more investment ideas?

If Live Nation has sharpened your focus, do not stop there. Cast a wider net across other stocks so you are not relying on a single story.

Use these targeted lists to quickly surface fresh ideas that match what you care about most.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com