Narrative")

- In early April 2026, Caesars Entertainment reported quarterly revenue that exceeded analyst forecasts but fell short on adjusted operating income and EPS, while also celebrating the grand opening of Harrah’s Oklahoma, its first managed casino in the state developed with the Iowa Tribe of Oklahoma.

- This combination of stronger-than-expected sales and expansion into a new tribal partnership market along the Route 66 corridor adds a fresh dimension to Caesars’ growth and diversification efforts.

- Next, we’ll examine how Caesars’ revenue beat and the opening of Harrah’s Oklahoma influence the company’s existing investment narrative.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

Caesars Entertainment Investment Narrative Recap

To own Caesars, you have to believe it can turn a large, mostly U.S. bricks and mortar footprint plus digital gaming into consistent, profitable cash flows while working down its debt. The latest quarter’s revenue beat, alongside a miss on operating income and EPS, keeps the near term earnings trajectory in focus, while leverage and interest costs remain the central risk. The stock’s strong move after results suggests sentiment is improving, but the core risk profile has not materially changed.

Against that backdrop, the opening of Harrah’s Oklahoma stands out because it fits the push toward asset light management contracts that can add revenue with less capital at risk. This tribal partnership along Route 66 may help diversify away from dependence on Las Vegas leisure customers, tying directly into the existing catalyst of higher margin, fee based growth. How efficiently Caesars layers in similar management deals could matter as much as what happens in any single earnings quarter.

Yet even with these positives, investors should not overlook the pressure that heavy debt and rising interest costs can place on future flexibility and returns…

Read the full narrative on Caesars Entertainment (it’s free!)

Caesars Entertainment’s narrative projects $12.3 billion revenue and $227.3 million earnings by 2029. This requires 2.4% yearly revenue growth and a $729.3 million earnings increase from -$502.0 million today.

Uncover how Caesars Entertainment’s forecasts yield a $31.96 fair value, a 19% upside to its current price.

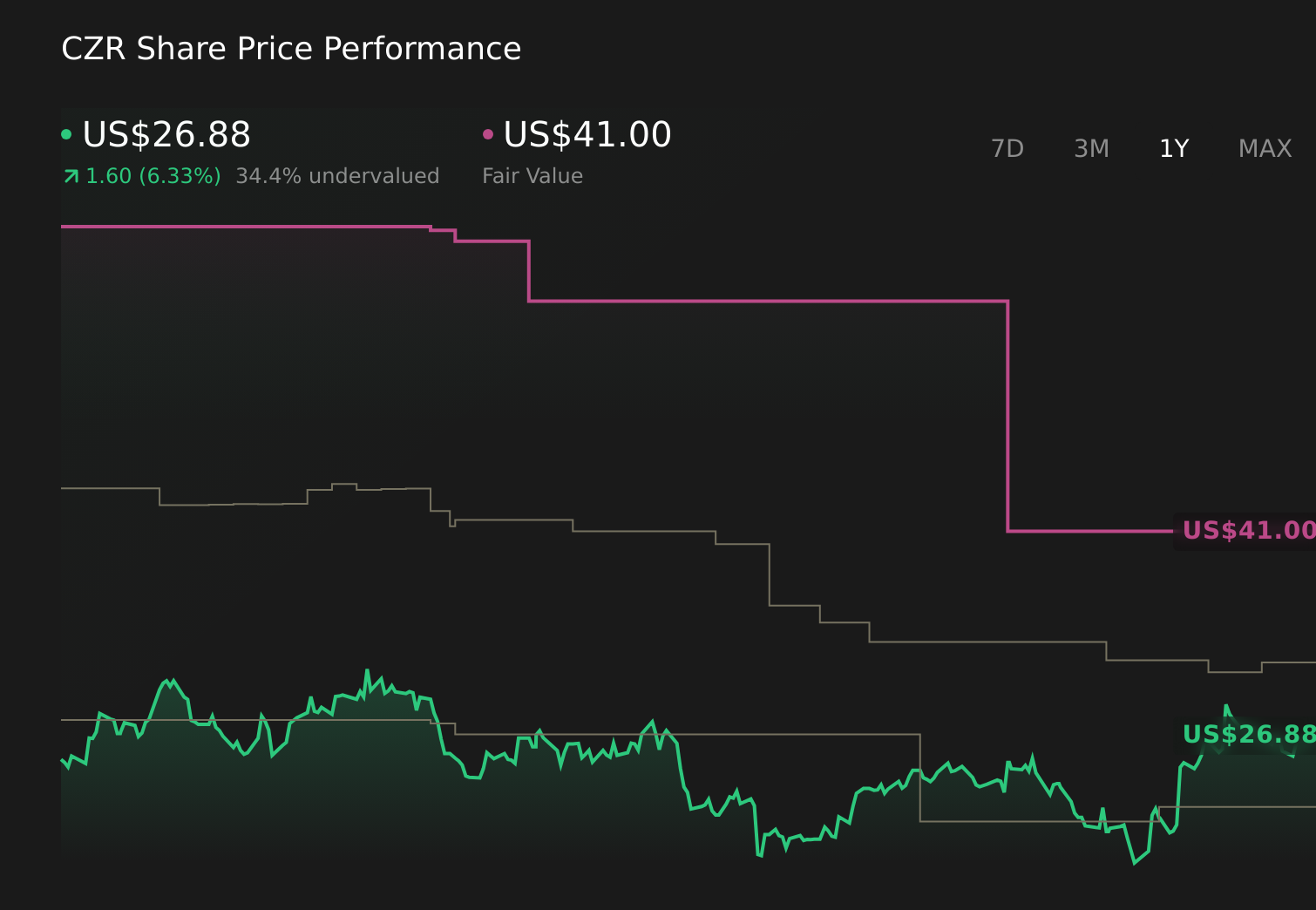

Exploring Other Perspectives CZR 1-Year Stock Price Chart

CZR 1-Year Stock Price Chart

Some of the lowest ranked analysts were assuming only about 1.1 percent annual revenue growth and roughly US$87.2 million of earnings by 2028, which is far more cautious than the consensus narrative that emphasizes digital growth and asset light deals like Harrah’s Oklahoma. For you as a shareholder, that gap in expectations is a reminder that this latest revenue beat and expansion could push forecasts higher, or reinforce the more pessimistic view, depending on how the next few quarters unfold.

Explore 5 other fair value estimates on Caesars Entertainment – why the stock might be worth just $31.96!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Caesars Entertainment research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Caesars Entertainment research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Caesars Entertainment’s overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com