Make better investment decisions with Simply Wall St’s easy, visual tools that give you a competitive edge.

-

Investors may be wondering whether GigaCloud Technology’s current share price reflects its true worth, or if the recent excitement has pushed it too far.

-

The stock last closed at US$46.74, with returns of 4.6% over 30 days, 20.6% year to date, and 250.9% over the past year. This comes alongside a 9.8% pullback in the last week that may have caught your eye.

-

Recent coverage has focused on GigaCloud Technology’s strong share price performance over the past 12 months and the attention this has drawn from both retail and institutional investors. Commentators have also highlighted that the current price level is prompting questions about whether the stock still offers value relative to its fundamentals.

-

Simply Wall St’s valuation model scores GigaCloud Technology a 4 out of 6 on its value checks. This sets up a closer look at metrics such as P/E, P/S, and DCF later in this article, along with a different way of thinking about valuation that can help pull everything together at the end.

GigaCloud Technology delivered 250.9% returns over the last year. See how this stacks up to the rest of the Retail Distributors industry.

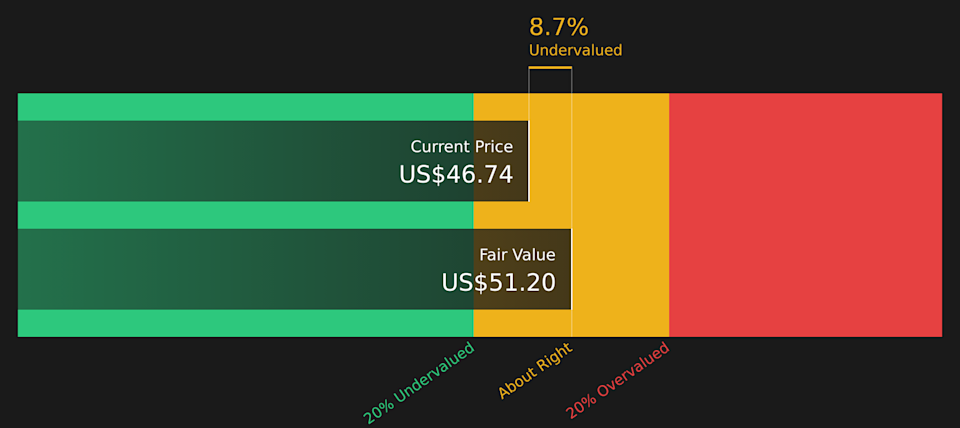

A Discounted Cash Flow, or DCF, model projects a company’s future cash flows and then discounts them back to today’s dollars to estimate what the business could be worth right now.

For GigaCloud Technology, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flows in $. The latest twelve month free cash flow is reported at about $179.30 million. Analyst input is available up to 2027, with free cash flow for 2027 of $104.45 million, and Simply Wall St then extrapolates cash flows out to 2035 using its own assumptions.

When those projected cash flows are discounted back, the model arrives at an estimated intrinsic value of US$51.20 per share. Compared with the recent share price of US$46.74, the DCF suggests the stock trades at an implied discount of roughly 8.7%, which is a relatively small gap.

This DCF view points to GigaCloud Technology being priced close to its modeled cash flow value, with only a modest margin either way.

Result: ABOUT RIGHT

GigaCloud Technology is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment’s notice. Track the value in your watchlist or portfolio and be alerted on when to act.

GCT Discounted Cash Flow as at Apr 2026

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for GigaCloud Technology.

For a profitable company, the P/E ratio is a useful shorthand for how much you are paying for each dollar of earnings, so it is a natural starting point when you are comparing valuation across similar businesses.

What counts as a “normal” or “fair” P/E depends on how quickly earnings are expected to grow and how risky those earnings are. Higher growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk usually points to a lower multiple.

GigaCloud Technology currently trades on a P/E of 12.46x. This sits below the Retail Distributors industry average P/E of 16.52x and also below the peer group average of 39.45x. Simply Wall St’s Fair Ratio for GigaCloud Technology is 14.03x. This is a proprietary estimate of the P/E that might be reasonable given factors such as the company’s earnings growth profile, industry, profit margins, market cap and risk characteristics.

Compared to simple industry or peer averages, the Fair Ratio can be more tailored because it adjusts for differences in growth, risk, profitability, sector and size. With the current P/E of 12.46x sitting below the Fair Ratio of 14.03x, this framework points to the shares trading at a discount on an earnings basis.

Result: UNDERVALUED

NasdaqGM:GCT P/E Ratio as at Apr 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Earlier it was mentioned that there is an even better way to understand valuation. Meet Narratives, a simple way for you to attach a clear story about GigaCloud Technology to hard numbers like your assumed fair value and your expectations for future revenue, earnings and margins.

A Narrative connects three pieces in one place: the company story you believe, the forecast that flows from that story, and the fair value that falls out of those numbers.

On Simply Wall St, Narratives sit inside the Community page and are used by millions of investors. You can quickly see different stories on GigaCloud Technology, such as a more cautious view with a Fair Value of about US$32.80 or a more optimistic view with a Fair Value of about US$73.00, instead of trying to reverse engineer every model yourself.

Once you have chosen or created a Narrative, the platform compares its Fair Value to the latest share price to help you decide whether the numbers line up with your own buy or sell thresholds. It also keeps that view current by updating the Narrative automatically when new earnings, guidance or news are added to the company profile.

For GigaCloud Technology, here are previews of two leading GigaCloud Technology Narratives:

🐂 GigaCloud Technology Bull Case

Fair value in this bullish Narrative: US$53.75 per share

Implied discount versus the last close of US$46.74: about 13.0% undervalued

Revenue growth assumption: 9.85% per year

-

Focuses on international expansion, especially in Europe, and integrated logistics as key supports for revenue and customer growth.

-

Highlights efficiency gains from acquisitions such as Noble House, SKU rationalization, and network scaling as drivers for margins and profitability.

-

Flags tariff exposure, European concentration, supply chain disruptions, and modest service revenue growth as the main risks to the thesis.

🐻 GigaCloud Technology Bear Case

Fair value in this more cautious Narrative: US$32.80 per share

Implied premium versus the last close of US$46.74: about 42.5% overvalued

Revenue growth assumption: 10.0% per year

-

Points to rapid GMV and revenue growth, acquisitions, and a large fulfillment footprint as positives, but questions how sustainable the current pace is at the current price.

-

Assumes meaningful long term revenue and margin expansion yet argues that execution risk in new regions and margin pressure from costs could limit earnings versus optimistic scenarios.

-

Notes competition from larger players and regulatory or tariff changes as potential constraints on growth that may not be fully reflected in a higher valuation.

These two Narratives frame the same set of facts in very different ways. The value for you is in deciding which story feels closer to how you see GigaCloud Technology, then checking whether the current price, your own assumptions, and your risk tolerance line up.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for GigaCloud Technology on Simply Wall St. Add the company to your watchlist or portfolio so you’ll be alerted when the story evolves.

Do you think there’s more to the story for GigaCloud Technology? Head over to our Community to see what others are saying!

NasdaqGM:GCT 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include GCT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

After Its 250% One-Year Surge?")