The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 index closing lower due to weak trade data from China, highlighting concerns over global economic recovery. In such an environment, identifying undervalued stocks can be crucial for investors seeking opportunities amidst broader market uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

Name

Current Price

Fair Value (Est)

Discount (Est)

Transense Technologies (AIM:TRT)

£0.585

£1.09

46.1%

Skillcast Group (AIM:SKL)

£0.47

£0.93

49.3%

RHI Magnesita (LSE:RHIM)

£27.25

£52.84

48.4%

Mitie Group (LSE:MTO)

£1.717

£3.26

47.3%

M&G (LSE:MNG)

£3.054

£5.71

46.5%

James Fisher and Sons (LSE:FSJ)

£4.89

£9.18

46.7%

GB Group (LSE:GBG)

£2.149

£3.96

45.7%

FDM Group (Holdings) (LSE:FDM)

£1.08

£2.14

49.5%

Eurocell (LSE:ECEL)

£1.015

£2.00

49.3%

Advanced Medical Solutions Group (AIM:AMS)

£2.40

£4.43

45.8%

Here we highlight a subset of our preferred stocks from the screener.

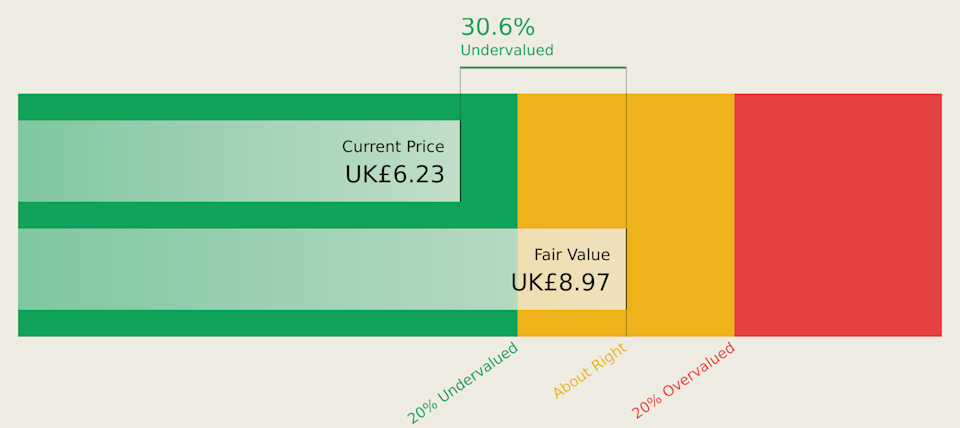

Overview: Polar Capital Holdings plc is a publicly owned investment manager with a market cap of £656.66 million.

Operations: The company’s revenue is primarily derived from its Investment Management Business, totaling £228.77 million.

Estimated Discount To Fair Value: 24%

Polar Capital Holdings is trading at £6.89, significantly below its estimated future cash flow value of £9.07, indicating it may be undervalued based on cash flows. The stock is 24% below its fair value estimate and earnings are projected to grow significantly by 21.67% annually over the next three years, outpacing the UK market’s growth rate of 12.2%. However, its dividend yield of 6.68% isn’t well covered by earnings or free cash flows.

AIM:POLR Discounted Cash Flow as at May 2026

Overview: Bridgepoint Group plc is a private equity and private credit firm focusing on middle market to small cap investments, including growth capital and buyouts, with a market cap of approximately £2.26 billion.

Operations: The company’s revenue segments consist of £84.50 million from Credit, £17.80 million from Central, £178 million from Infrastructure, and £311.80 million from Private Equity.

Estimated Discount To Fair Value: 39.4%

Bridgepoint Group is trading at £2.57, significantly below its estimated future cash flow value of £4.24, suggesting potential undervaluation based on cash flows. Despite a recent decline in profit margins to 6.6% from 15.2%, earnings are forecast to grow significantly by 38.7% annually, surpassing the UK market’s growth rate of 12.2%. However, the dividend yield of 3.66% is not well covered by earnings, and return on equity is expected to remain low at 19.5%.