Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

-

Wondering if Uranium Energy at around US$15.59 is still offering value or if the easy gains are behind it? This article focuses squarely on what the current price might be implying.

-

The stock has seen strong moves recently, with returns of 4.7% over 7 days, 18.9% over 30 days, 18.9% year to date and 179.4% over the past year, while the 3 year and 5 year returns are both very large.

-

These moves sit against a backdrop of ongoing interest in uranium and nuclear related assets, with investors paying close attention to policy developments, project updates and capital allocation across the sector. For Uranium Energy, this context is key to understanding why sentiment around the stock has shifted over different time frames.

-

On Simply Wall St’s 6 point valuation framework, Uranium Energy currently scores 2 out of 6. The rest of this article will walk through the key valuation approaches investors often use, then finish by highlighting a broader way to think about what this price might be telling you.

Uranium Energy scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Uranium Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and discounting them back to today using a required return. It is essentially asking what Uranium Energy’s future cash generation might be worth in today’s dollars.

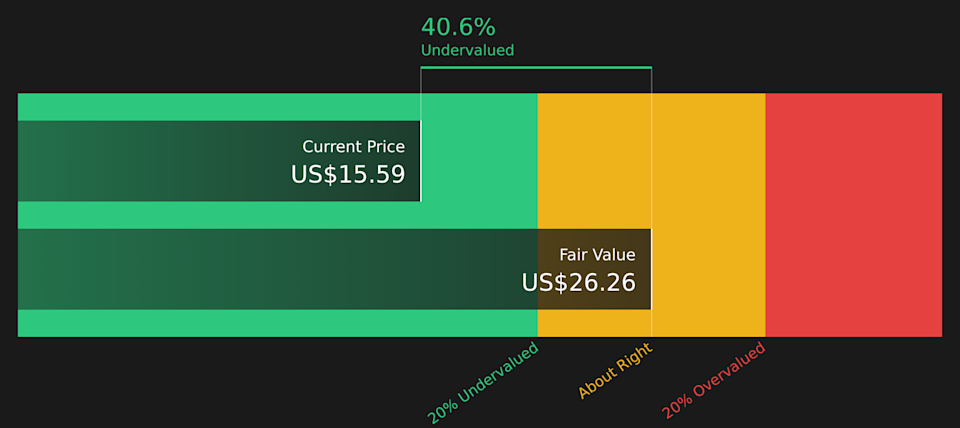

For Uranium Energy, the 2 Stage Free Cash Flow to Equity model starts from last twelve months free cash flow of a loss of $118.2 million, then uses analyst and extrapolated estimates to map a potential path to positive cash flow. The projections move to $153 million of free cash flow in 2028, with a broader ten year path that reaches around $729.5 million by 2035, all in $ and all discounted back to today in the model.

On this basis, the model arrives at an estimated intrinsic value of about $26.26 per share. Versus a current share price of around $15.59, the DCF implies Uranium Energy trades at a 40.6% discount, which indicates the stock may be undervalued on these cash flow assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Uranium Energy is undervalued by 40.6%. Track this in your watchlist or portfolio, or discover 51 more high quality undervalued stocks.

UEC Discounted Cash Flow as at May 2026

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Uranium Energy.

Approach 2: Uranium Energy Price vs Book

For companies where current earnings are less informative, investors often look at the price to book, or P/B, ratio because it compares the market value of the equity to the accounting value of net assets. It is a way of asking how much you are paying for each dollar of book value on the balance sheet.

Expectations for growth and the level of risk influence what might be seen as a typical P/B ratio, with higher growth and lower perceived risk often lining up with higher multiples. Uranium Energy currently trades on a P/B of 5.41x, compared with the Oil and Gas industry average of 1.62x and a peer average of 2.29x, so the stock is priced well above these broad reference points.

Simply Wall St also uses a proprietary “Fair Ratio” for P/B, which estimates the multiple that might be reasonable given factors such as earnings growth, profit margins, industry, market cap and risk profile. This can offer a more tailored yardstick than simple industry or peer comparisons, which treat very different companies as if they were the same. In this case, there is no Fair Ratio available, so it is not possible to draw a firm conclusion from this approach.

Result: ABOUT RIGHT

NYSEAM:UEC P/B Ratio as at May 2026

P/B ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your Uranium Energy Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives on Simply Wall St give you a clear story behind your numbers by linking your view on Uranium Energy’s future revenue, earnings and margins to a forecast and a fair value, then comparing that fair value to the current price to help you decide whether to act, all while updating automatically as new news or earnings arrive. An optimistic Uranium Energy Narrative might lean toward the high fair value of about US$21.91 based on assumptions such as earnings of roughly US$312.6 million by 2029 and a P/E of 50.8x. A more cautious Narrative might sit closer to US$16.64 with earnings of about US$120.8 million by 2028 and a P/E of 99.8x. This gives you a simple way to see how different assumptions about the same stock lead to very different conclusions.

Do you think there’s more to the story for Uranium Energy? Head over to our Community to see what others are saying!

NYSEAM:UEC 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include UEC.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

After Its 179% One-Year Surge?")