Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

-

Olin Corporation (NYSE:OLN) has restructured its Epoxy segment, including rationalizing high cost assets.

-

The company now positions itself as the last integrated epoxy producer in Europe.

-

Olin is relying on structural cost advantages from its U.S. Gulf Coast assets to support Epoxy segment profitability.

-

These steps come as the broader epoxy market faces volatility tied to geopolitical events and global supply chain disruptions.

Olin, a chemicals and ammunition producer, is putting fresh focus on its Epoxy segment at a time when global supply chains remain under pressure. By trimming higher cost assets and concentrating on integrated production in Europe, the company is reshaping how this business fits alongside its U.S. Gulf Coast operations. For investors, the Epoxy changes sit alongside Olin’s broader chemicals footprint, which is closely linked to industrial and construction activity.

With the company highlighting a return to profitability in Epoxy, attention now turns to how durable this improvement might be if supply disruptions ease or customer demand shifts. The mix of European integration and Gulf Coast cost structure gives investors specific areas to monitor, including operating rates, product mix, and capital allocation priorities across the portfolio.

Stay updated on the most important news stories for Olin by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Olin.

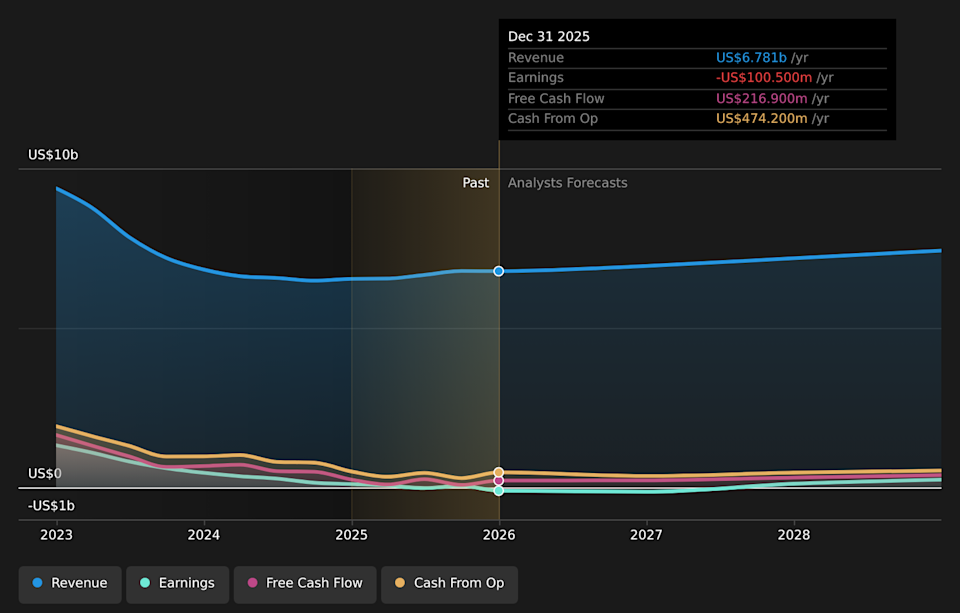

NYSE:OLN Earnings & Revenue Growth as at May 2026

We’ve flagged 2 risks for Olin. See which could impact your investment.

Quick Assessment

-

⚖️ Price vs Analyst Target: At US$26.76, Olin trades almost in line with the US$26.79 analyst target, sitting within the typical range of expectations.

-

✅ Simply Wall St Valuation: Shares are flagged as trading about 64.7% below an estimated fair value, suggesting a wide valuation gap.

-

❌ Recent Momentum: The 30 day return of about 11.2% decline shows recent weakness despite the Epoxy pivot.

There is only one way to know the right time to buy, sell or hold Olin. Head to Simply Wall St’s company report for the latest analysis of Olin’s Fair Value.

Key Considerations

-

📊 The Epoxy restructuring and focus on integrated assets could be important for restoring profitability in a segment exposed to supply chain volatility.

-

📊 Watch Epoxy margins, utilization of U.S. Gulf Coast facilities, and how management prioritizes capital between chemicals, ammunition and potential debt reduction.

-

⚠️ Interest payments are not well covered by earnings, so balance sheet strength and cash generation are key to how resilient this pivot really is.