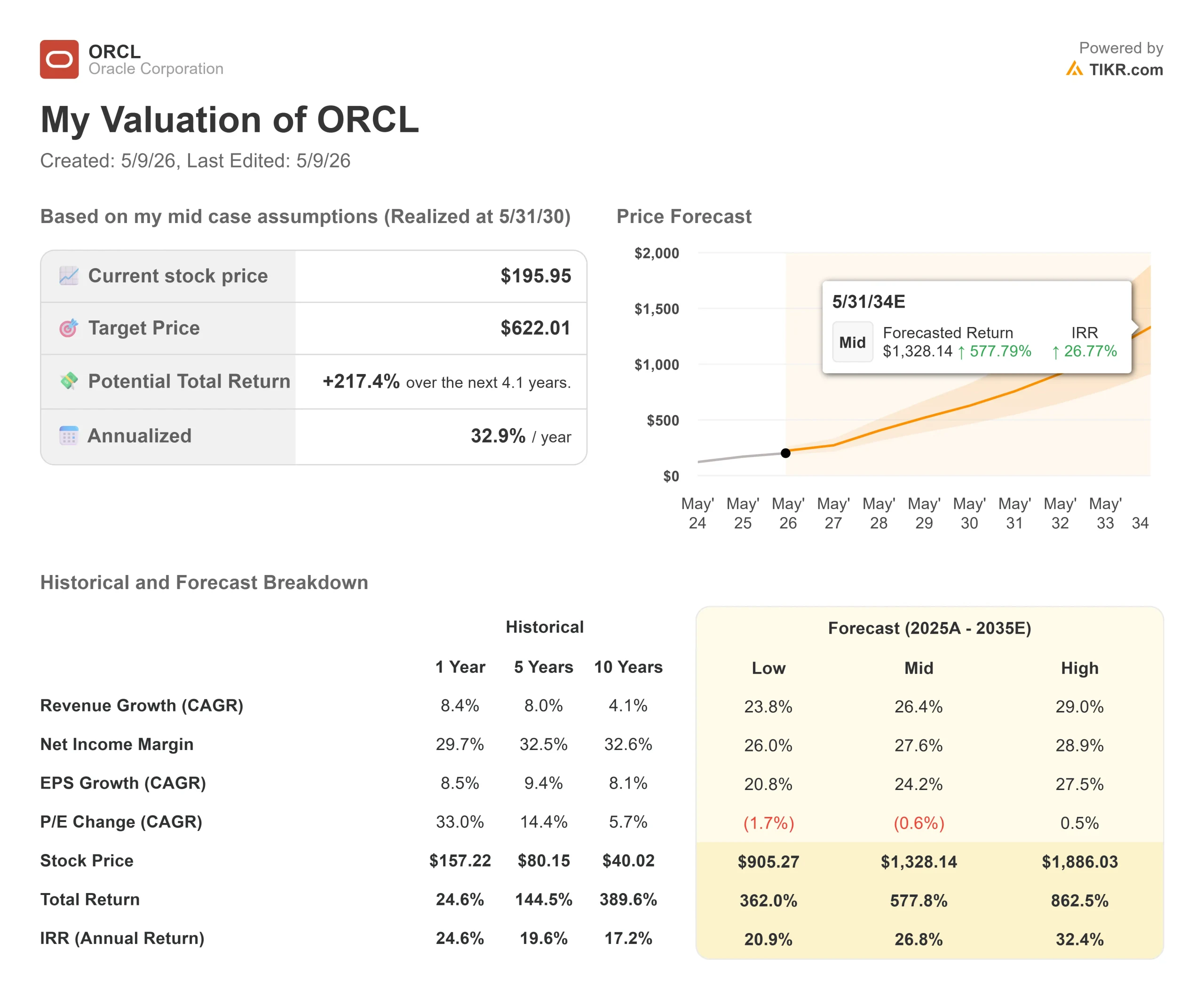

- Current Price: $195.95

- Target Price (Mid): ~$622

- Street Target: ~$242

- Potential Total Return: ~217%

- Annualized IRR: ~33% / year

- Earnings Reaction: +9.18% (3/10/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

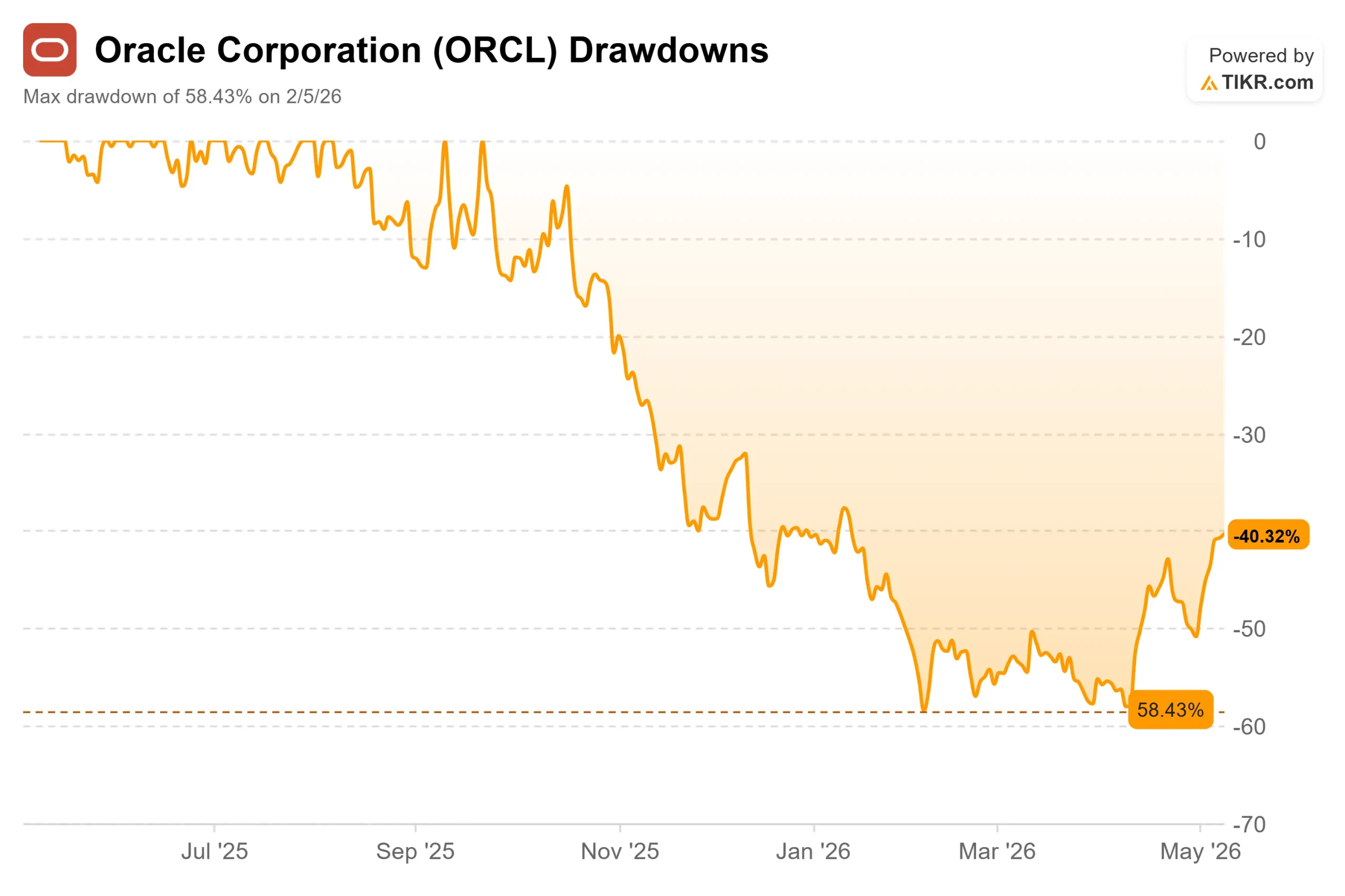

Oracle (ORCL) has rallied roughly 46% from its February 5 trough of $134.57, and Wall Street has shifted from debating whether Oracle is in trouble to debating whether the selloff was simply overblown. On May 1, the Department of Defense announced that Oracle joined seven other frontier AI companies, including Amazon Web Services, Microsoft, Google, and OpenAI, in formal agreements to deploy AI on the Pentagon’s classified networks, covering its most sensitive Impact Level 6 and Impact Level 7 environments. Shares rose more than 3% on the news.

The bear case hasn’t gone away. Oracle carries roughly $123 billion in net debt, is burning free cash flow through fiscal 2028, and faces a securities class action filed in March 2026. The bull case, now with a government stamp of approval, is that Oracle isn’t a legacy database company on defense. It’s a full-stack AI platform that enterprise and government customers increasingly can’t replace.

The central question is whether the $553 billion RPO (remaining performance obligations, meaning contracted future revenue not yet recognized) converts fast enough to justify the debt load before the market loses patience.

Oracle Drawdowns (TIKR)

Oracle Drawdowns (TIKR)

See historical and forward estimates for Oracle stock (It’s free!) >>>

What the DoD Deal Actually Signals

The strategic significance of this agreement goes beyond a single contract win.

Oracle already operates 10 cloud regions dedicated to U.S. government customers, supporting capabilities across DISA Impact Levels 2, 4, 5, and 6, as well as Top Secret and Special Access Programs environments, per the Department of War’s May 1 announcement. The new agreement extends that footprint into the Pentagon’s most sensitive IL7 environments reserved for the highest-classification national security data.

What makes this more than an infrastructure contract is that it validates Oracle’s full-stack positioning. On the Q3 FY2026 earnings call, CEO Mike Sicilia made clear that Oracle’s AI strategy isn’t about selling compute in isolation. It’s about embedding AI across the entire stack, OCI (Oracle Cloud Infrastructure, the company’s cloud platform), plus database, plus enterprise applications inside environments customers can fully control. The DoD agreement reflects that same architecture, applied at the most security-sensitive level in the U.S. government.

Oracle is one of eight companies cleared for this work. That list is not open-ended, and it includes every major hyperscaler Oracle is already partnered with on its multicloud database expansion.

The SaaS Business the Market Is Underweighting

Most Oracle coverage focuses on OCI and the RPO backlog. The applications business rarely gets a paragraph. That’s a mistake, because the two are connected in ways the market hasn’t fully priced.

Per Sicilia’s Q3 prepared remarks, cloud applications revenue reached an annualized run rate of $16.1 billion, growing 11% in constant currency. Inside that number: Fusion ERP grew 14%, Fusion HCM and SCM each grew 15%, and industry-specific SaaS (hospitality, banking, retail, healthcare) combined to grow 19%. Over 2,000 customers went live on Oracle’s applications in Q3 alone. Notable competitive wins included Memorial Hermann Health System over Workday, a major Wall Street bank standardizing on Fusion ERP company-wide over SAP, and Investec Bank selecting Fusion over SAP.

The connection to the infrastructure thesis is what Sicilia called the “halo effect.” When Oracle moves a customer’s workloads to OCI, it often creates budget headroom because OCI costs less and runs faster than competing clouds which then funds the ERP or HCM transformation Oracle pitches next. As Sicilia put it on the call: “We can often help customers get to a position of budget creation simply by moving their workloads to OCI we can run them more quickly, more efficiently, and less expensively than our competitors.”

Some have argued that AI coding tools will let startups displace enterprise SaaS incumbents quickly, what Oracle’s team calls the “SaaSpocalypse” thesis. Sicilia addressed it directly: “I have not yet met a customer who tells me they’re ready to give away their retail merchandising system, their core banking system, or their electronic health record systems for some cobbling together of niche AI features.” Oracle has already embedded over 1,000 AI agents inside Fusion applications, included at no additional cost as part of quarterly updates. The applications business isn’t waiting to be disrupted; it’s doing the disrupting.

On valuation multiples, Oracle trades at 15.68x NTM EV/EBITDA, per TIKR’s Competitors page as of May 8. That’s a premium to Microsoft at 13.65x and a significant premium to Salesforce at 8.62x. The premium over Salesforce is defensible: Oracle is growing total cloud revenue at 44% year over year while Salesforce grows in the high single digits, and Oracle competes in an infrastructure category Salesforce doesn’t touch.

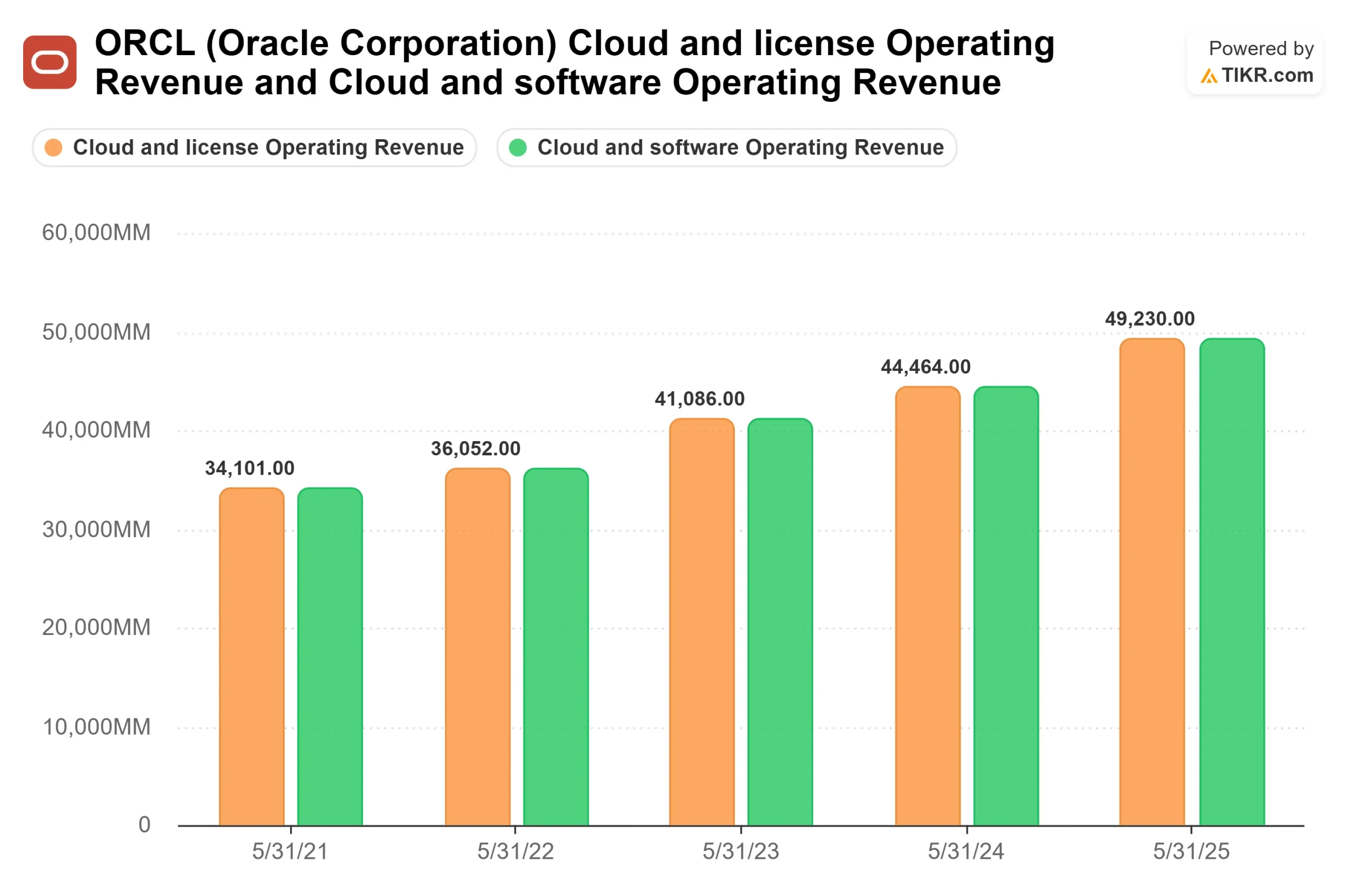

Oracle Cloud, License, & Software Operating Revenue (TIKR)

Oracle Cloud, License, & Software Operating Revenue (TIKR)

The Multicloud Database: The 531% Story Nobody Is Talking About

The most underappreciated number from Q3 wasn’t in the headlines. Multicloud database revenue grew 531% year over year, per Oracle’s Q3 FY2026 earnings release.

Oracle’s database had historically only run on OCI. Partnerships with Microsoft, Google, and AWS changed so that Oracle’s database now runs natively inside each hyperscaler’s own environment. By the end of Q3, Oracle had 33 live regions with Microsoft and 14 with Google. With AWS, Oracle started Q3 with 2 live regions and exited with 8, targeting 22 by the end of Q4, per CEO Clay Magouyrk’s prepared remarks.

This matters for two reasons beyond the revenue number. First, it unlocks Oracle’s massive installed database customer base, who already run workloads on Azure, AWS, or Google Cloud but couldn’t previously use Oracle’s database inside those environments. Second, Magouyrk confirmed on the call that multicloud database gross margins run in the 60% to 80% range, compared to 30% to 32% for AI infrastructure GPU capacity. As multicloud scales, it structurally lifts Oracle’s blended margin profile, and that’s the mechanism the TIKR model depends on to support the 2030 price target.

What the Bears Are Right About

Oracle’s LTM free cash flow is deeply negative, per TIKR data. FY2026 capital expenditures are guided at $50 billion, per Oracle’s Q3 earnings release. TIKR consensus estimates show FCF remaining negative through fiscal 2028 before recovering in fiscal 2029, a long runway of cash burn before the thesis proves out in the financials.

The balance sheet carries roughly $123 billion in net debt at a 4.12x LTM Net Debt/EBITDA ratio, per TIKR. A securities class action was filed in March 2026. And a meaningful portion of the $553 billion RPO is concentrated among a small number of large AI customers; any pullback in committed spend from that group would pressure both the backlog and revenue conversion timelines.

The structural offset Magouyrk described on the call is important context: since Q2, Oracle has signed more than $29 billion in contracts using a bring-your-own-hardware and customer upfront payment model that, as he put it, “enables us to continue expanding without any negative cash flow from Oracle.” That structure caps Oracle’s actual cash exposure even as the gross capex figure looks alarming.

See how Oracle performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $195.95

- Target Price (Mid): ~$622

- Potential Total Return: ~217%

- Annualized IRR: ~33% / year

Oracle Stock Price Target (TIKR)

Oracle Stock Price Target (TIKR)

See analysts’ growth forecasts and price targets for Oracle stock (It’s free!) >>>

The TIKR mid-case assumes a revenue CAGR of around 26% from fiscal 2025 through 2030, per the valuation model screenshot. Two drivers underpin that: OCI consumption growth as the $553 billion RPO converts to recognized revenue, and multicloud database attach rates accelerating across all three hyperscaler partner networks. The net income margin is modeled at around 28% by fiscal 2030, declining modestly from current levels as the mix shift toward lower-margin AI infrastructure is only partially offset by high-margin multicloud database and SaaS growth. The P/E multiple compresses modestly at around -0.6% per year as Oracle transitions from a pure software valuation to a blended infrastructure-and-software multiple.

On the upside: the TIKR high case at around 29% revenue CAGR prices the stock at around $905 by May 31, 2030. On the downside: if capex stays elevated through fiscal 2028 and a major AI customer reduces committed spend, the FCF recovery shifts further right and the thesis gets pushed out materially.

The Street’s mean target of around $242 from 30 Buy, 6 Outperform, 6 Hold, 1 No Opinion, 0 Underperform, and 1 Sell among 44 analysts implies roughly 24% upside from today. The gap between $242 and $622 tells you the TIKR mid-case requires Oracle to execute at the higher end of its own guidance, consistently, for four years.

Conclusion

Watch total cloud revenue at Q4 FY2026 earnings on June 16. Oracle has guided 46% to 50% total cloud revenue growth for Q4 in USD. If Oracle hits that range while multicloud database regions with AWS continue expanding toward the guided 22, it demonstrates the $553 billion backlog is converting on schedule and clears the path toward the Street mean target of ~$242. Oracle has built a full-stack AI position spanning infrastructure, database, and enterprise applications that no single-layer competitor can replicate. The Pentagon deal didn’t start that story. It confirmed it.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Oracle?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Oracle, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Oracle alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!