Before It Goes Ex-Dividend")

Regular readers will know that we love our dividends at Simply Wall St, which is why it’s exciting to see Brookfield Business Corporation (TSE:BBUC) is about to trade ex-dividend in the next 4 days. Typically, the ex-dividend date is one business day before the record date, which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn’t show on the record date. This means that investors who purchase Brookfield Business’ shares on or after the 29th of May will not receive the dividend, which will be paid on the 30th of June.

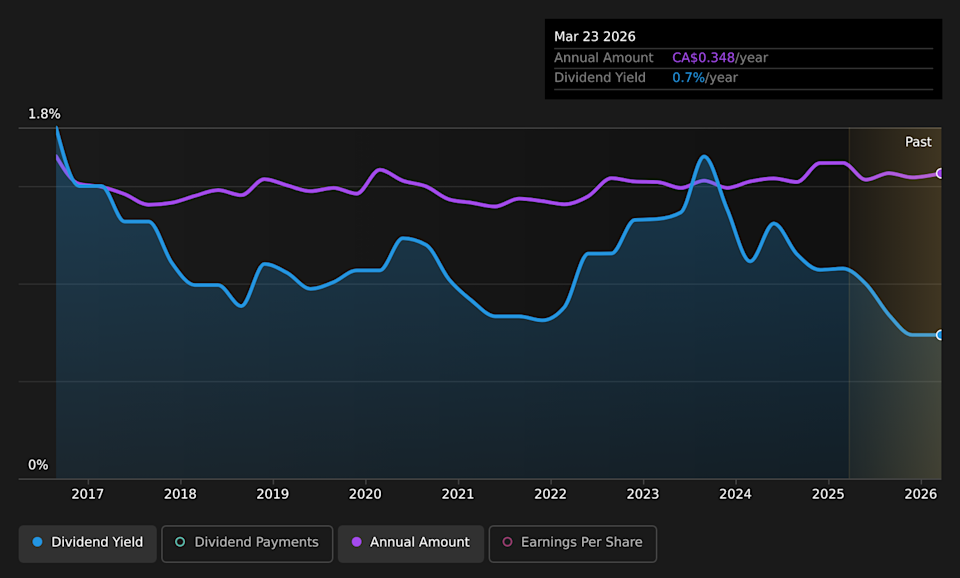

The company’s next dividend payment will be US$0.0625 per share, on the back of last year when the company paid a total of US$0.25 to shareholders. Calculating the last year’s worth of payments shows that Brookfield Business has a trailing yield of 0.7% on the current share price of CA$46.54. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to check whether the dividend payments are covered, and if earnings are growing.

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Brookfield Business’s dividend is not well covered by earnings, as the company lost money last year. This is not a sustainable state of affairs, so it would be worth investigating if earnings are expected to recover. Given that the company reported a loss last year, we now need to see if it generated enough free cash flow to fund the dividend. If Brookfield Business didn’t generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. Luckily it paid out just 2.0% of its free cash flow last year.

View our latest analysis for Brookfield Business

Click here to see how much of its profit Brookfield Business paid out over the last 12 months.

TSX:BBUC Historic Dividend May 24th 2026 Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Brookfield Business reported a loss last year, and the general trend suggests its earnings have also been declining in recent years, making us wonder if the dividend is at risk.