Valuation After Q1 2026 Earnings Beat And Dividend Hike")

Tsakos Energy Navigation (TEN) is back in focus after Q1 2026 results and a fresh dividend move, reporting earnings per share of US$2.72 and the highest common dividend in more than a decade.

See our latest analysis for Tsakos Energy Navigation.

Despite the Q1 beat and higher dividend, Tsakos Energy Navigation’s share price has eased 4.2% in the last day. However, the 30 day share price return of 8.5% and year to date gain of 94.7% signal strong momentum, supported by a 1 year total shareholder return of 154.7%.

If you are watching how shipping and energy related trades are evolving, this can be a useful moment to look at other opportunities through our 35 power grid technology and infrastructure stocks

With TEN trading at US$42.61, only about 8% below a consensus price target of US$46.00 and showing a small premium to some intrinsic estimates, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 7.4% Undervalued

With Tsakos Energy Navigation last closing at $42.61 against a narrative fair value of $46.00, the current setup leans slightly in favor of the valuation case built around long term contracts and earnings resilience.

The company’s significant investment in fleet modernization with a focus on eco friendly, dual fuel, and high specification vessels positions it to secure higher time charter rates from energy majors, control operating expenses, and meet upcoming environmental regulations, all of which should improve net margins and earnings resilience. Growing long term contracted revenue backlog ($3.7–4.0 billion, representing more than $120 per share) with blue chip oil majors amid global energy security concerns provides strong revenue visibility and reduces earnings volatility, supporting prospective dividend growth and underpinning a higher intrinsic valuation.

Want to see what earnings path and profit margins sit behind that fair value and how much multiple expansion it assumes for 2029 profits? The narrative unpacks one central revenue trajectory, a reset in profitability, and a future valuation multiple that looks very different from today.

Result: Fair Value of $46 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, you also need to weigh the heavy reliance on oil transport and relatively high net debt, which could bite if decarbonization pressure or financing costs increase.

Find out about the key risks to this Tsakos Energy Navigation narrative.

Another View: DCF Flips The Story

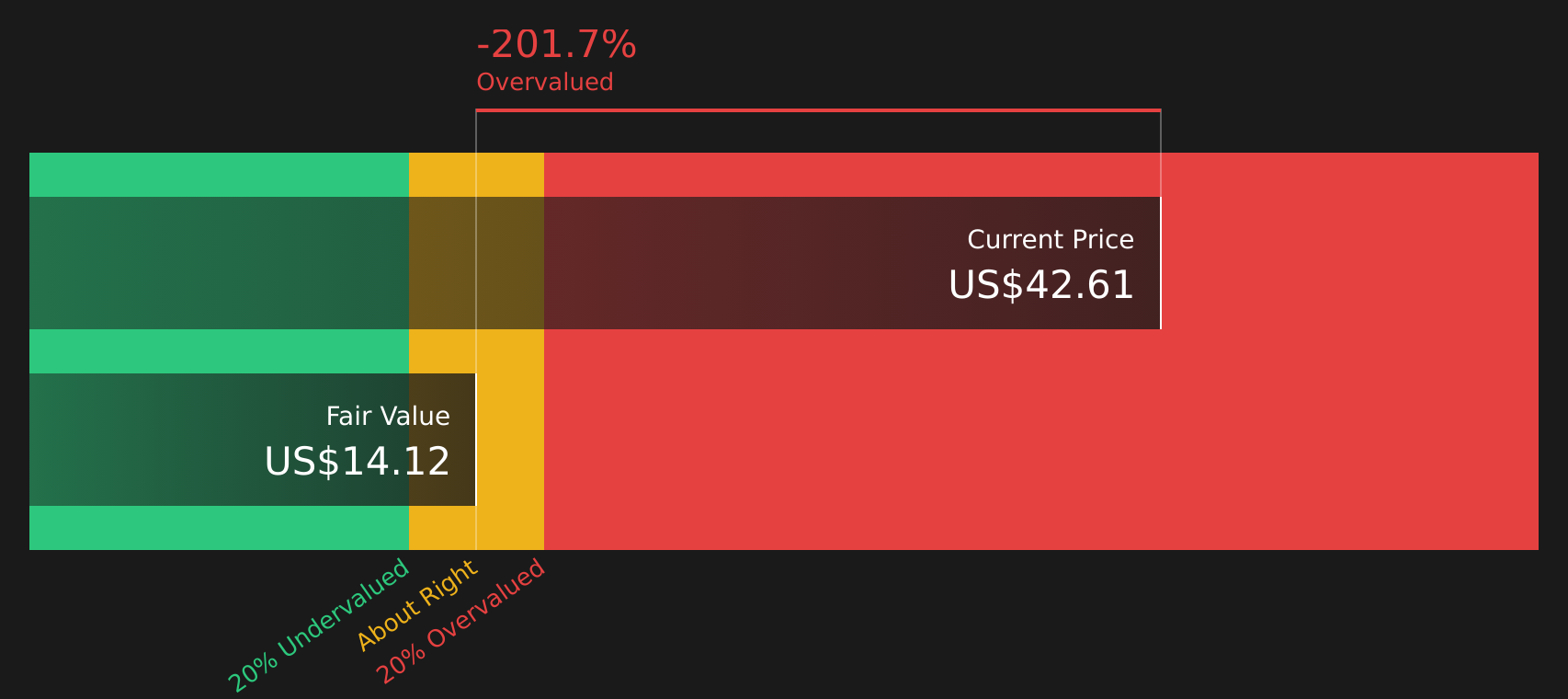

While the narrative fair value points to Tsakos Energy Navigation being 7.4% undervalued at $46, the SWS DCF model tells a very different story, with a future cash flow value of $14.12, which would frame the current $42.61 share price as expensive rather than cheap. Which set of assumptions do you find more realistic for your own thesis?

Look into how the SWS DCF model arrives at its fair value.

TEN Discounted Cash Flow as at May 2026

TEN Discounted Cash Flow as at May 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tsakos Energy Navigation for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

With such a mixed picture on valuation and outlook, the real question is how you weigh the trade off between risk and reward. Take a closer look at the underlying data, pressure test both sides of the argument, and use the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If you stop here, you only see one corner of the market. Use the screener to widen your field of vision and pressure test your next move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if Tsakos Energy Navigation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com