Stocks Have Crushed Nvidia in 2026 With Gains of 67% and 121%. They Can Still Soar Higher")

Artificial intelligence (AI) pioneer Nvidia is having an underwhelming 2026 so far despite delivering outstanding results quarter after quarter. Shares of the chipmaker have appreciated only 12% this year, well below the 74% jump in the PHLX Semiconductor Sector index.

However, shares of Lumentum Holdings (LITE 0.71%) and Applied Materials (AMAT +0.03%) have been flying high in 2026. While Lumentum stock has gained 121% this year, Applied Materials has also jumped by an impressive 67%. Both companies have benefited from massive investments in AI infrastructure.

Let’s take a closer look at the reasons why these two stocks have been in fine form on the market so far this year and check why they are likely to deliver more upside.

Image source: Getty Images

AI is driving phenomenal growth at Lumentum Holdings

Lumentum Holdings manufactures optical and photonic components, such as lasers, transceivers, and amplifiers, which are deployed in the cloud, networking, and industrial markets. The company’s products enable high-speed connectivity in data centers, which explains why they are in high demand from hyperscalers to reduce latency when transmitting large datasets.

Today’s Change

(-0.71%) $-6.12

Current Price

$854.50

Market Cap

$67B

Day’s Range

$822.50 – $867.83

52wk Range

$72.29 – $1085.68

Volume

176.9K

Avg Vol

6.5M

Gross Margin

35.36%

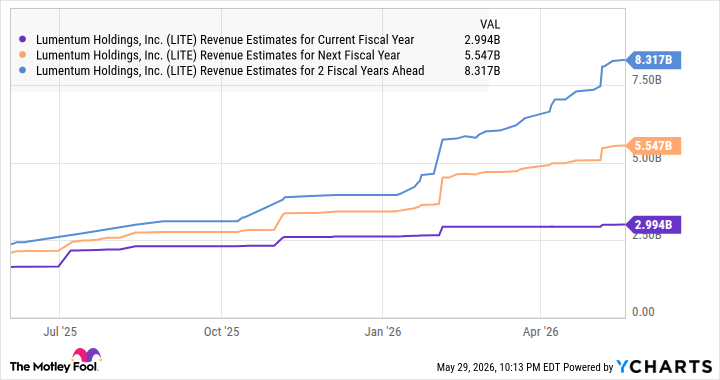

Lumentum’s revenue and earnings growth have taken off amid AI-fueled demand from data centers. Its revenue in the first nine months of fiscal 2026 (which ended on March 28) increased by 72% year over year to just over $2 billion. Lumentum’s guidance of $985 million in revenue for the current quarter suggests that its top line will more than double from the year-ago period’s reading of $480.7 million.

This acceleration in Lumentum’s growth suggests that demand for its products is strengthening. That’s not surprising, as Lumentum’s optical and photonics components remove a key bottleneck in AI model training and inference tasks. The high-speed connectivity enabled by Lumentum’s products means AI accelerator chips don’t need to sit idle waiting for data, thereby reducing the time required to run workloads in the cloud.

Not surprisingly, the optical component market is expected to grow at an annual rate of 21% through 2029, generating $30 billion in revenue at the end of the forecast period, according to market research provider Cignal AI. So, Lumentum’s addressable market is poised to grow nicely in the coming years, which is why analysts expect solid revenue growth from the company.

Data by YCharts

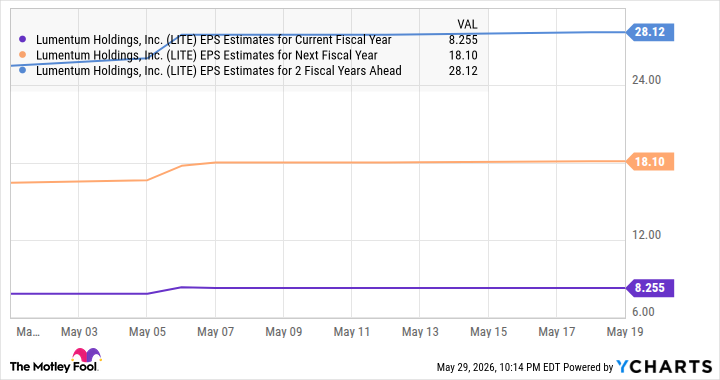

Even better, Lumentum notes that its data center products carry higher margins. This is translating into solid bottom-line growth for the company, with its earnings per share increasing by 4.5x year over year in the first nine months of fiscal 2026 to $5.27. Importantly, the robust revenue growth that Lumentum is expected to deliver is poised to translate into healthy earnings growth as well.

Data by YCharts

Of course, Lumentum trades at an expensive 56 times forward earnings, but its red-hot earnings growth justifies that valuation. Assuming this AI stock trades at a discounted 50 times earnings after a couple of years and achieves $28.12 in earnings per share (as per the chart above), its price could reach $1,406. That’s a potential upside of 64%, which means that it isn’t too late for investors to buy this high-flying stock.

Applied Materials’ growth is picking up on the back of healthy AI chip demand

The semiconductor industry has been booming thanks to AI, which is driving up demand for wafer and fabrication equipment (WFE) needed to manufacture chips for data centers and other AI applications. Applied Materials is capitalizing on the growth of the semiconductor equipment market, as it sells manufacturing equipment and also offers software and services to optimize the performance of such equipment.

The company’s revenue increased 11% year over year in the second quarter of fiscal 2026 (which ended on April 26) to $7.91 billion. Earnings per share jumped by 20% year over year to $2.86 per share. These numbers were a big improvement over the company’s fiscal Q1 performance when its revenue fell 2%, and earnings remained flat.

Applied Materials’ guidance suggests that its growth is poised to accelerate impressively in the current quarter. The company anticipates $8.95 billion in revenue and $3.36 in non-GAAP earnings per share in the current quarter, indicating that its top line could jump by 23% year over year while earnings growth will accelerate to 36%.

Applied Materials management anticipates an increase of over 30% in its semiconductor equipment business this year, followed by another solid jump in 2027 due to the continued investments in this space. The company notes that investments in leading-edge foundry equipment, dynamic random-access memory (DRAM), and advanced packaging will account for 80% of the WFE market’s growth in 2026, and a similar pattern is expected to follow next year.

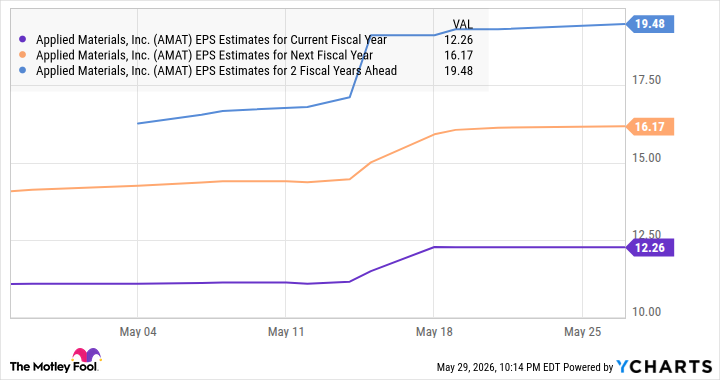

Additionally, Applied Materials’ partnerships with TSMC, Micron Technology, SK Hynix, and Samsung to develop AI-focused equipment put it in a solid position to capitalize on the growth of the semiconductor equipment market. Not surprisingly, analysts have substantially increased their earnings growth expectations for Applied Materials.

Data by YCharts

If its earnings indeed jump to $19.48 after a couple of fiscal years and it trades at 43 times earnings at that time (in line with the tech-focused Nasdaq Composite index’s earnings multiple), its stock price could reach $837. That suggests potential upside of 86% in this semiconductor stock, which is why investors can consider buying it before it soars higher.