Source: U.S. Bureau of Economic Analysis retrieved from FRED, Federal Reserve Bank of St. Louis

Tools: Datawrapper, Illustrator

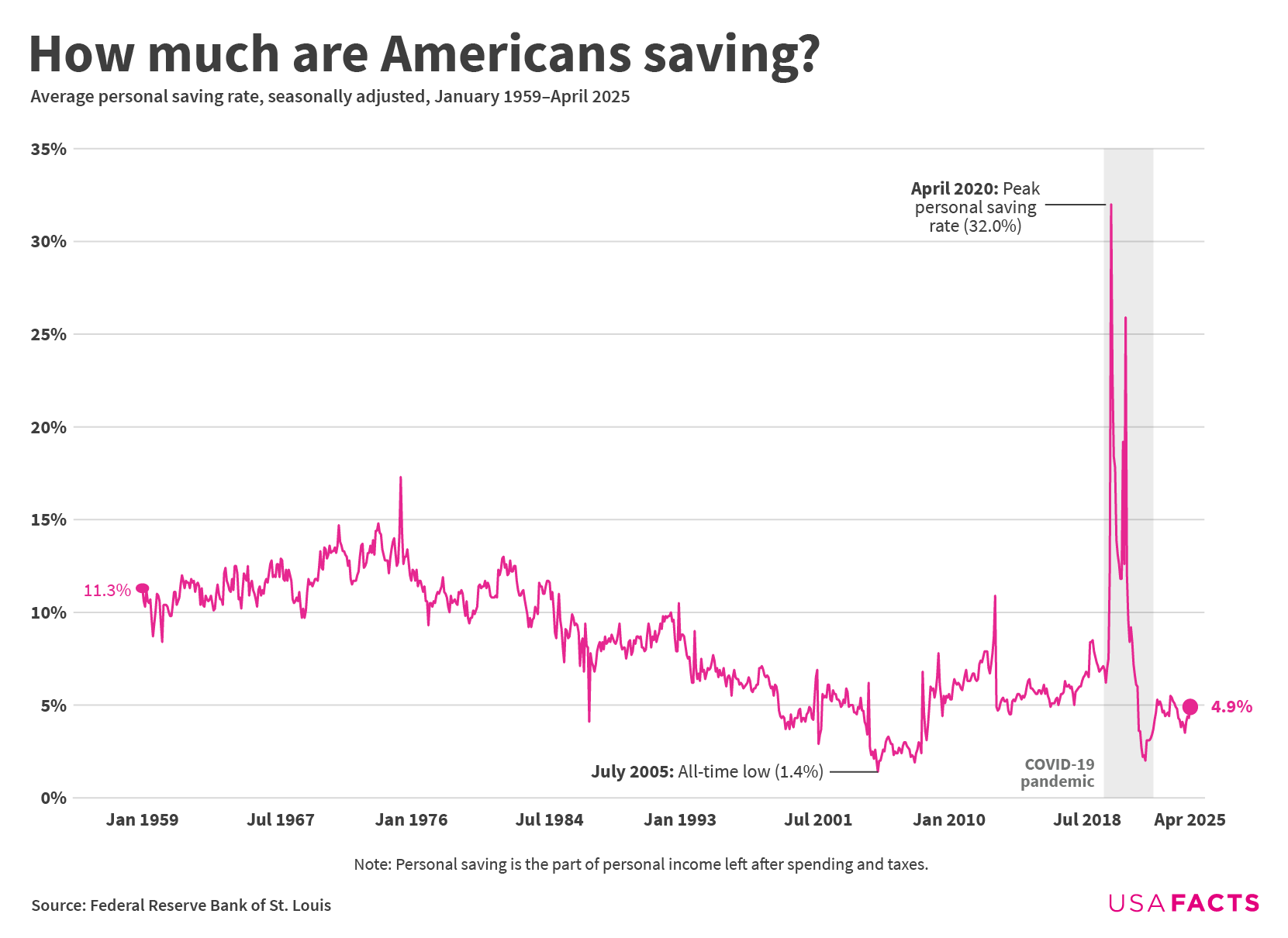

Note: Personal saving as a percentage of disposable personal income (DPI), frequently referred to as “the personal saving rate,” is calculated as the ratio of personal saving to DPI. Personal saving is equal to personal income less personal outlays and personal taxes; it may generally be viewed as the portion of personal income that is used either to provide funds to capital markets or to invest in real assets such as residences.

Simpler note: The personal saving rate is the share of disposable income people set aside after taxes and expenses, including money in checking and savings accounts, retirement plans like IRAs and 401(k)s, and other cash-based savings. It doesn’t count increases in home values or stock market gains unless they’re cashed out.

nopoonintended on

Isn’t it concerning that our savings rate increased 28% when we couldn’t travel / eat out / go out like damn so people could save if they stayed home more

Hold on people are really only saving 5% of there money? That’s crazy to me.

CakeisaDie on

Surprised it was 5%

Thought was lower.

ndt29 on

Is retirement savings (401k) counted here?

USAFacts on

Americans aren’t saving like they used to. In 2024, the average personal saving rate was 4.6% of disposable income. In the 1960s and 70s, Americans saved an average of 11.7%, with a high point of 17.3% in May 1975. Even the 2010s had a higher average saving rate than today, at 6.1%.

A few other moments stand out: There was a spike in savings during the early pandemic — peaking at 32% in April 2020 — due to stimulus checks, lockdowns, and reduced spending opportunities. But before that, the lowest point on record came in 2005, when savings dropped to just 1.4%. The FDIC pointed to high consumer and housing-related debt and a *sense* of financial security driven by strong economic indicators at the time.

I’m not sure I understand how this works. Like, on average, *everyone* is saving? Does it not go negative if you are consuming your savings?

TheHappyEater on

These steep jumps in May 1975, April 1987, around 9/11, December 2012/January 2013 as well as the covid pandemic makes me wonder if these are

– artefacts of some kind of change of methodolgy of underlying time series

– changes because the denominator (the disposable income) did change drastically (which can be seen for the 2012/2013 change and covid pandemic)

– changes of the nominator (less spending and taxes), which is at least plausible for covid as well, where there were less oppurtunities to spend money.

SlimJim0877 on

That’s crazy. I am currently saving ~29% to buy a house and it still doesn’t feel like enough.

kodex1717 on

Whenever I hear the word “saving” in personal finance discussions, it’s often unclear to me whether it’s referring to literal money in cash account or if it also includes semi-liquid investments such as 401k’s, Roth IRA’s, or a stock portfolio. Based on the note at the bottom, I *think* this would exclude 401k investments, but not sure about IRAs or stocks.

It’s an important distinction. Someone would be in a far different financial position if they were saving 4.9% of their **salary** in cash alone vs saving 4.9% of their take-home after maxing out their 401k.

DisastrousCat13 on

I would love to see this by quintile. And maybe remove the top 1% from the top quintile depending on how it screws the data.

The_Fluffness on

I have job that I don’t make much money at. I don’t go out, I don’t willy nilly spend the money. Once a week when I get paid I buy all the food I need and pay bills. My friends who all have better jobs are completely blown away that I have over 50 grand saved since COVID.

Completedspoon on

Wasn’t that from those COVID relief checks that almost everyone got?

ireaditonwikipedia on

Seems like we are headed towards economic catastrophe as a country.

The skyrocketing cost of living, increased people living on credit, jobs going offshore, just not sustainable.

The billionaires don’t give a shit but they are too short sighted to see that even if they don’t care about the regular American (they don’t), if they are not able to afford products and services they are going to suffer as well. This country is so short sighted and it’s going to cost us all.

![[OC] How much money are Americans saving?](https://www.byteseu.com/wp-content/uploads/2025/06/ol2v2764uh9f1-1536x1119.png "[OC] How much money are Americans saving?")

21 Comments

Source: U.S. Bureau of Economic Analysis retrieved from FRED, Federal Reserve Bank of St. Louis

Tools: Datawrapper, Illustrator

Note: Personal saving as a percentage of disposable personal income (DPI), frequently referred to as “the personal saving rate,” is calculated as the ratio of personal saving to DPI. Personal saving is equal to personal income less personal outlays and personal taxes; it may generally be viewed as the portion of personal income that is used either to provide funds to capital markets or to invest in real assets such as residences.

Simpler note: The personal saving rate is the share of disposable income people set aside after taxes and expenses, including money in checking and savings accounts, retirement plans like IRAs and 401(k)s, and other cash-based savings. It doesn’t count increases in home values or stock market gains unless they’re cashed out.

Isn’t it concerning that our savings rate increased 28% when we couldn’t travel / eat out / go out like damn so people could save if they stayed home more

You guys are saving money?

https://preview.redd.it/eycs13aevh9f1.jpeg?width=520&format=pjpg&auto=webp&s=af807f82447ff873388ff46fee47fed730db8d7f

Hold on people are really only saving 5% of there money? That’s crazy to me.

Surprised it was 5%

Thought was lower.

Is retirement savings (401k) counted here?

Americans aren’t saving like they used to. In 2024, the average personal saving rate was 4.6% of disposable income. In the 1960s and 70s, Americans saved an average of 11.7%, with a high point of 17.3% in May 1975. Even the 2010s had a higher average saving rate than today, at 6.1%.

A few other moments stand out: There was a spike in savings during the early pandemic — peaking at 32% in April 2020 — due to stimulus checks, lockdowns, and reduced spending opportunities. But before that, the lowest point on record came in 2005, when savings dropped to just 1.4%. The FDIC pointed to high consumer and housing-related debt and a *sense* of financial security driven by strong economic indicators at the time.

[This CRS Report](https://www.congress.gov/crs-product/IF10963) (not a PDF, I promise) talks about the economic implications of the personal saving rate.

I was still gainfully employed. I bought i-bonds.

This percentage could easily be doubled if people actually applied discipline to their spending

As with so many other data, things started going to shit in the early 70s, thanks Nixon! https://wtfhappenedin1971.com/

I’m not sure I understand how this works. Like, on average, *everyone* is saving? Does it not go negative if you are consuming your savings?

These steep jumps in May 1975, April 1987, around 9/11, December 2012/January 2013 as well as the covid pandemic makes me wonder if these are

– artefacts of some kind of change of methodolgy of underlying time series

– changes because the denominator (the disposable income) did change drastically (which can be seen for the 2012/2013 change and covid pandemic)

– changes of the nominator (less spending and taxes), which is at least plausible for covid as well, where there were less oppurtunities to spend money.

That’s crazy. I am currently saving ~29% to buy a house and it still doesn’t feel like enough.

Whenever I hear the word “saving” in personal finance discussions, it’s often unclear to me whether it’s referring to literal money in cash account or if it also includes semi-liquid investments such as 401k’s, Roth IRA’s, or a stock portfolio. Based on the note at the bottom, I *think* this would exclude 401k investments, but not sure about IRAs or stocks.

It’s an important distinction. Someone would be in a far different financial position if they were saving 4.9% of their **salary** in cash alone vs saving 4.9% of their take-home after maxing out their 401k.

I would love to see this by quintile. And maybe remove the top 1% from the top quintile depending on how it screws the data.

I have job that I don’t make much money at. I don’t go out, I don’t willy nilly spend the money. Once a week when I get paid I buy all the food I need and pay bills. My friends who all have better jobs are completely blown away that I have over 50 grand saved since COVID.

Wasn’t that from those COVID relief checks that almost everyone got?

Seems like we are headed towards economic catastrophe as a country.

The skyrocketing cost of living, increased people living on credit, jobs going offshore, just not sustainable.

The billionaires don’t give a shit but they are too short sighted to see that even if they don’t care about the regular American (they don’t), if they are not able to afford products and services they are going to suffer as well. This country is so short sighted and it’s going to cost us all.

Idk why this was aggregated by a third party but it’s readily available here:

https://fred.stlouisfed.org/series/PSAVERT

5% in the average & Americans wonder why they can’t retire

Heh, I remember when there was literally nothing to spend money on.