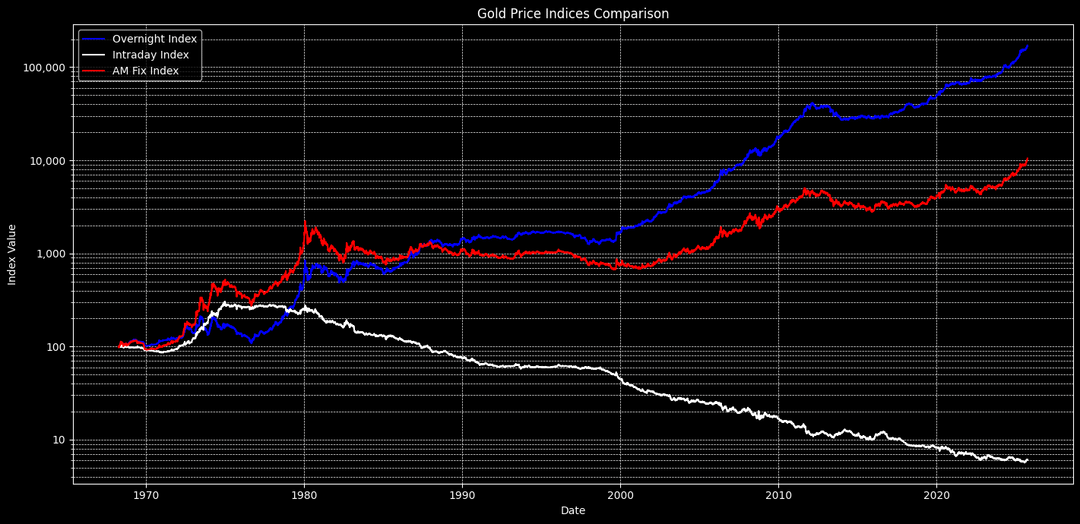

![[OC] I analyzed 50+ years of LBMA precious metals prices and found something wild: all the gains happen overnight](https://www.byteseu.com/wp-content/uploads/2025/10/eusvagt4l2wf1-1024x497.png "[OC] I analyzed 50+ years of LBMA precious metals prices and found something wild: all the gains happen overnight")

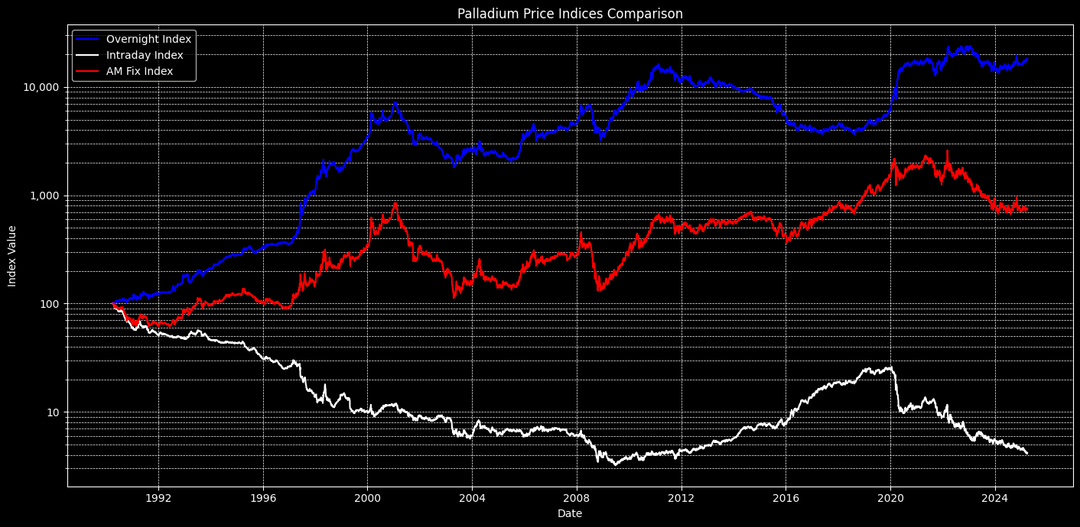

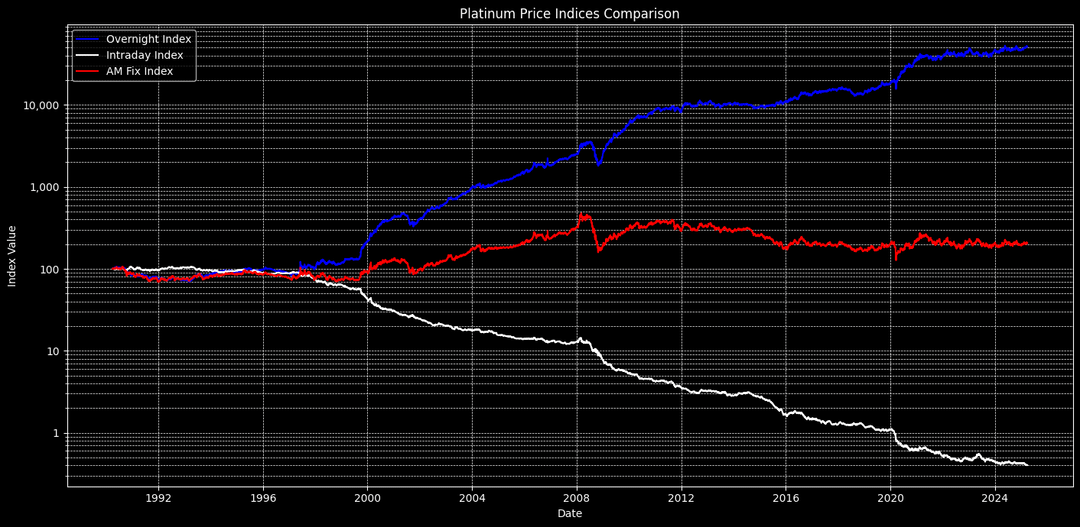

I split gold, platinum, and palladium prices into two strategies: buying at morning fix and selling at afternoon fix (intraday/Western hours) vs. buying at afternoon fix and selling next morning (overnight/Eastern hours).

The results are pretty shocking:

Gold (1968-2025):

- Overnight strategy: +171,205.59% (13.83% CAGR)

- Intraday strategy: -93.88% (-4.73% CAGR)

- Buy & hold: +10,383.91% (8.43% CAGR)

Platinum (1990-2025):

- Overnight: +84,293.88% (20.86% CAGR)

- Intraday: -99.6% 🤯

If you'd only held the metals during London/NY hours for the past 50 years, you'd have basically lost everything. All the appreciation happened during Asian trading hours.

Full analysis and code: https://github.com/Robin-Haupt-1/lbma-east-west-divergence

I've seen this analysis somewhere else before for gold, but not the other metals. As far as i'm aware this is the first public analysis of all LBMA metals that have AM and PM fixes.

Posted by robinhaupt

11 Comments

Data source: Official LBMA website (scraped)

Tool used for visualization: matplotlib

see codebase for details

I’ve seen this analysis somewhere else before for gold, but not the other metals. As far as i’m aware this is the first public analysis of all LBMA metals that have AM and PM fixes.

Thanks! This is very cool! I will never sleep again!

Sorry there where some mistakes in the percentage calculations in this post. I have fixed them.

Cross post that to /r/investing, see what they say 😉

Edit typo

It would be nice to see this showing the nightly returns instead of the price.

But do all the losses also happen overnight?

Shouldn’t red be a combination of white and blue but it isn’t for gold?

I found the same thing with the S&P500 by accident when I was doing some analysis several years ago. I took the close price – the open price assuming that this would approximately equal the s&p500 return of 8-12%. Instead it was close to -32%. Then i realized I got the math wrong. I wasn’t including the close to open price changes and was a huge eye opener about long and steady.

If you were to recalculate numbers, and include standard spread in your calculations, by how much would the profit drop? Would it become negative? (For example, last update before market close on the Amundi Physical Gold ETC sell was 144,38€ and buy was 145€ – was at 11pm, so prbably wider spread than usual)

Might be worth experimenting for a year with 1k budget and a trading bot on an ETC

Edit: Did it myself, i assumed a 0.1% spread, reminded me why i hate python and especially jupyter notebooks, a pain to get running, bu there’s the result for gold, safe to say not a worthwhile trading strategy, you’re gonna loose relatively fast, if you were to try it with physical gold you’re gonna have to sassume closer to 1-2% spread.

https://preview.redd.it/evpq400633wf1.png?width=1404&format=png&auto=webp&s=ed8a5e557b91852ac91aec41ef8ffe03963fe71e

So in the Asian market the investment pattern would be reversed? Buy in the morning and sell in the afternoon?

The Asian arb trade was famous. It stopped working some time ago. I recall that you could have made 50000% return just buying and selling AM and PM. I think that this was difficult to do in practice. I don’t remember why.