The economy is a bit confusing right now. While the labor market appeared to be standing still, the estimated growth in gross domestic product (GDP) stood at 3.8 percent for the 3rd quarter, according to the Atlanta Federal Reserve. Similarly, within the household sector there appears to be an increasing bifurcation between higher-income and lower-income Americans.

The New York Times reports:

The share of subprime auto loans that were 60 days or more past due reached a high of nearly 6.5 percent in January and has lingered near that level, according to Fitch Ratings. Repossessions have swelled, more drivers are trading in vehicles that are worth less than they owe and lenders such as CarMax and Ally Financial have warned investors about auto loan performance.

CNBC has a similar story, with the added color: “The average price paid for a new vehicle last month topped $50,000 for the first time ever, Cox Automotive’s Kelley Blue Book reported Monday.”

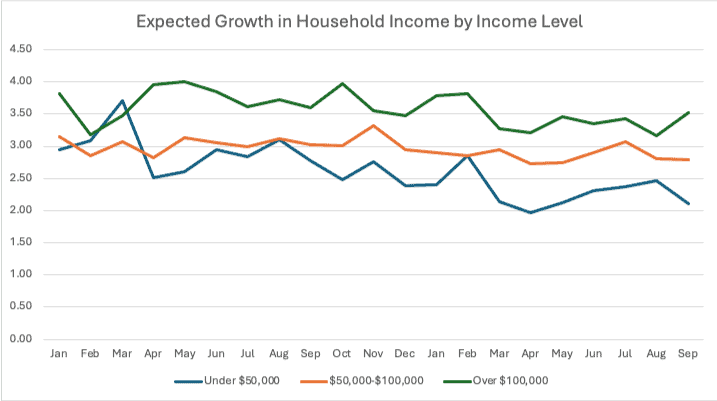

And households are expecting the divergence to increase. Shown below are data on expected growth in household income from the New York Federal Reserve’s survey of consumer expectations. Since the beginning of 2024, expected growth in household income has diminished across the income distribution. It declined by 0.31 percentage points for the highest-income households (over $100,000). Similarly, middle-income households ($50,000 to $100,000) have lowered their expectations for growth by 0.35 percentage points. But the drop off was nearly three times as large – 0.83 percentage points – among the lowest-income households (under $50,000).

These data suggest a dilemma for the Fed as it considers its next move in the meeting next week. The low-income households are likely more interest-rate sensitive, and would benefit from a rate cut. But they are also simultaneously most exposed to inflation pressures, which are likely to increase even more if the Fed cuts rates aggressively.