[OC] The High Cost of Big Banks: I tracked daily mortgage rates from 120+ Credit Unions vs. the Big 4 Banks to show how not shopping around costs homeowners $50k+

Posted by mhashemi

![[OC] The High Cost of Big Banks: I tracked daily mortgage rates from 120+ Credit Unions vs. the Big 4 Banks to show how not shopping around costs homeowners $50k+](https://www.byteseu.com/wp-content/uploads/2025/12/u2m62ckvlu4g1-675x1024.png "[OC] The High Cost of Big Banks: I tracked daily mortgage rates from 120+ Credit Unions vs. the Big 4 Banks to show how not shopping around costs homeowners $50k+")

[OC] The High Cost of Big Banks: I tracked daily mortgage rates from 120+ Credit Unions vs. the Big 4 Banks to show how not shopping around costs homeowners $50k+

Posted by mhashemi

14 Comments

I’ve only banked with a credit union while my SO had a big bank for a while. I was shocked at the basic things that he couldn’t do, like live mobile money management. Doesn’t much surprise me that mortgage costs are even worse.

What kind of graph is this, bird formation style?

I’d love to see the data, is it public?

went through Bank of America last December and got a 5.25% rate somehow

I’ve found credit unions are better when you’re borrowing their money and banks are better when they’re borrowing your money, but yeah: always shop around.

I am nearly 50 and have never in my life heard a practical reason that a bank is better than a CU.

*laughs in 3.5% fixed rate with no mortgage insurance* Damn, 2013 really was the last decent year for purchasing a home and getting a reasonable mortgage.

Fair enough, looking at historical average mortgage interest rates is crazy, in 2020 the average dipped below 3%.

Although the interest rates more than doubled over the past 5 years it is still way below what people used to pay (for 30 year mortgages).

[OC]

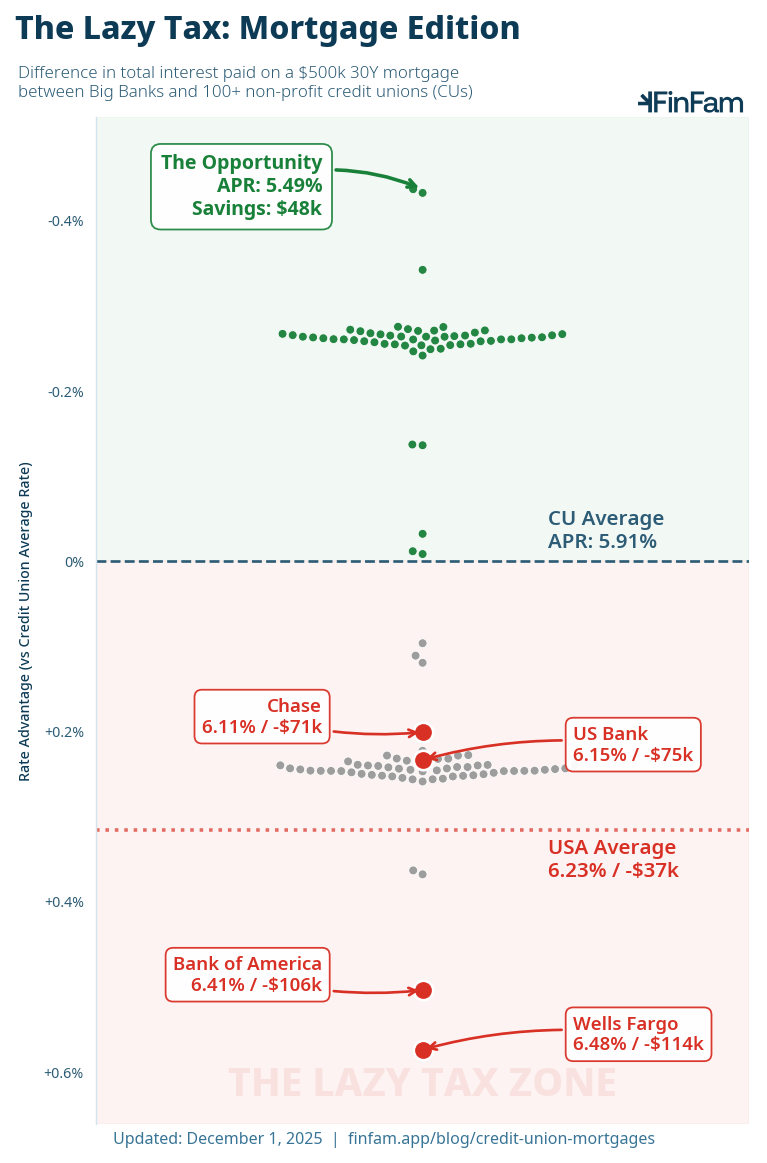

**Methodology**: Over the last couple weeks, I collected daily mortgage rates from 120+ credit union websites across the US and compared them against the big four banks (Wells Fargo, Chase, US Bank, Bank of America). The national benchmark comes from FRED (google St. Louis Fed’s weekly 30-year fixed rate survey).

The y-axis compares each rate to the average credit union APR, which is currently 30+ basis points cheaper than the national average. Went with average CU rate instead of median to stay consistent with the national benchmark. (At the time of writing, the median CU rate is 5.96%, so results are similar.) I calculated the total interest paid to show the real dollar impact ($50k+), despite the loan being virtually identical. Everything here assumes a conventional 30-year fixed mortgage with $500k loan, 20% down, 700+ credit score, and primary residence. Refi, other time frames, variants (FHA/VA/etc.) are also explorable on the FinFam blog (finfam dot app slash blog)

**Why**: I was inspired by the recent episode of Bloomberg Odd Lots with Itamar Dreschsler that explained why credit card rates are so high. TL;DR The higher rates are largely to pay for the advertising/marketing. As explained by the Bits About Money newsletter cheaper loans aren’t worse; the mortgages are all bought by the government (“Mortgages are a manufactured product”). We may naturally feel a privilege when a bank flatters you with what feels like an exclusive offer or a reward for loyalty. But in reality, credit Unions are non-profits, and bigger lenders have marketing departments that smaller institutions don’t have.

I go into this more on the FinFam blog, but there are real reasons to use a bigger lender, and not all credit unions are necessarily cheaper. I just want to enable folks to shop around and go in with eyes open.

**Tools**: I wanted something that’s quick to update, so I built this with Python (matplotlib/seaborn/pandas). The dashboard is Svelte. Font is Noto Sans.

NB: I posted an earlier comment with links but it’s hidden, so posting this one for now.

Guilty, didnt shop like I should’ve. I got a 4.875% rate through Chase in ’22.

Of course, I also naively assumed this stuff was standard at the time and a moving target. It was locked in August, the last day average rates were below 5%

I went through Chase earlier this year, and got a 6.125%. I can’t remember if I locked that in during March or April, but I closed at the end of April.

Yeah I dumped the mortgage company helping me because they couldn’t match my credit union’s interest rate. I’m not paying an extra $100 a month for 30 years just to make some mortgage guy happy.

I think it was like 2.87% vs 3.15%, which is kind of a lot of money.

Using my mortgage constant calculator on $500k borrowed over 30 years, I calculated:

* $196k savings from Wells fargo vs. lowest CU rate

* $117k savings using USA average vs. lowest CU rate

* $37 savings from USA average vs. average CU rate

May I ask who the top entities are on the graph?

Have you looked into HYSA?