Valuation After Strong Quarterly Revenue And Earnings Beat")

SkyWater Technology (SKYT) is back in focus after reporting quarterly revenue of US$150.74 million, up 60.7% year over year, with EPS of US$0.24 versus US$0.08 a year earlier.

See our latest analysis for SkyWater Technology.

The earnings beat and revenue jump have coincided with strong momentum, with a 30 day share price return of 123.05% and a 1 year total shareholder return of 186.58%, while the latest share price sits at US$33.10.

If SkyWater’s recent move has caught your eye, it could be a good moment to see what else is gaining attention among high growth tech and AI stocks.

After such a sharp move, the key question is whether SkyWater’s current US$33.10 price still leaves room for upside, or whether the recent surge already reflects the growth investors expect from here.

Most Popular Narrative: 58% Overvalued

With SkyWater’s fair value in the most followed narrative at roughly US$21, compared with a last close of US$33.10, the key issue is how much long term growth and profitability this view is baking in.

The analysts have a consensus price target of $13.2 for SkyWater Technology based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $18.0, and the most bearish reporting a price target of just $9.0.

Want to see what kind of revenue ramp and margin shift sit behind that fair value? The narrative is built on bold growth, profitability and valuation assumptions. Curious how those pieces fit together in the model?

Result: Fair Value of $21 (OVERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are real pressure points too, including higher debt from the Fab 25 deal and an ongoing reliance on government contracts that could unsettle revenue and cash flow.

Find out about the key risks to this SkyWater Technology narrative.

Another Angle On Valuation

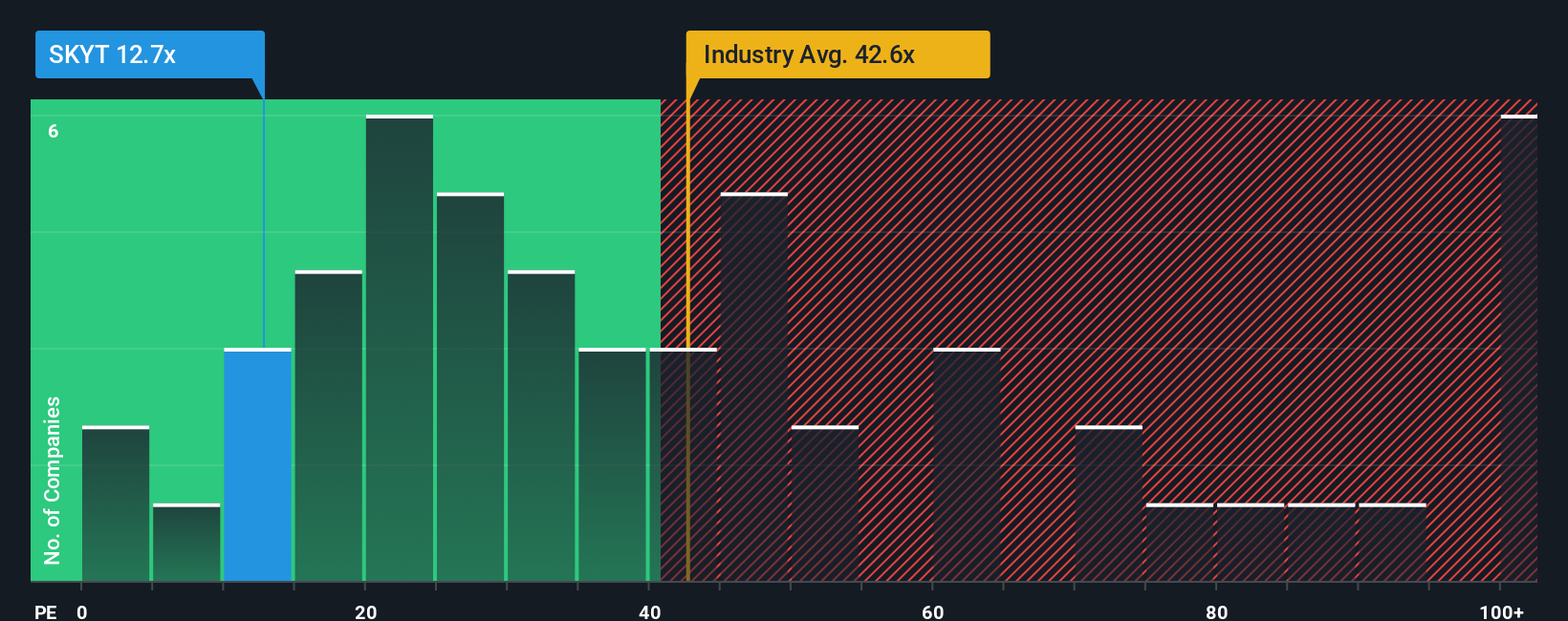

Those narrative fair value estimates of about US$21 sit alongside a very different signal from traditional earnings multiples. SkyWater trades on a P/E of 12.7x, which is far below peers at 83.4x and the US Semiconductor industry at 43.4x, yet above its fair ratio of 6x. That gap suggests the market could still shift either way, so which number do you trust?

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqCM:SKYT P/E Ratio as at Jan 2026 Build Your Own SkyWater Technology Narrative

NasdaqCM:SKYT P/E Ratio as at Jan 2026 Build Your Own SkyWater Technology Narrative

If you see the numbers differently or prefer to stress test your own assumptions, you can build a complete SkyWater story yourself in minutes, Do it your way.

A great starting point for your SkyWater Technology research is our analysis highlighting 3 key rewards and 5 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If SkyWater has sparked your interest, do not stop here. Use the Simply Wall St Screener to quickly surface other focused ideas that could sharpen your watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com