Lower Rates Combined with Strong Economic Growth Needs Housing Supply Growth to Avoid Higher Home Prices

President Trump plans to release his housing initiative on Wednesday at the 2026 Davos World Economic Forum.

According to Realtor.com, returning the housing market to 2019 levels of affordability is a daunting task. Mortgage rates would need to fall 2.5 percentage points, or incomes rising 56%, or home prices falling 35%. At the same time, President Trump has cautioned about “creating a lot of housing all of the sudden, and [driving] home prices down.”

Yet inaction on supply has its own risks. Implementation of multiple demand boosters combined with a strong economy would ignite strong home price appreciation.

The Trump administration is projecting strong economic growth and lower interest rates on 30-year fixed rate mortgages to say 4.5% from 6.25% during the first week of January 2026.

At 6.25% the monthly principal and interest payment on a $240,000 mortgage loan would be $1,478 compared to $1,216 for the same mortgage loan at 4.5%.

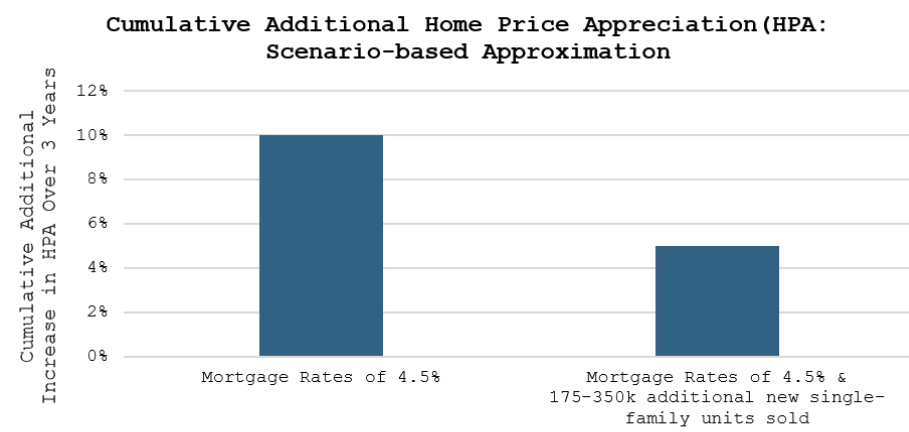

Our analysis considers two possible supply and home price appreciation (HPA) scenarios over the next 3 years¹:

Scenario 1:

A 10% increase in cumulative HPA over the next three years, if a rate drop of this magnitude were combined with no change in the level of supply additions.

- This 10% increase in HPA would increase the monthly payment at 4.5% from $1,216 to $1,378, cancelling out about half of the benefit.

Scenario 2:

A 5% increase in cumulative HPA over the next three years, if a rate drop of this magnitude were combined with an increase in single-family supply additions to about 875,000 – 1,050,000 homes from the current annual level of 700,000 (roughly a 25–50% increase in production).

- This 5% increase in HPA would increase the monthly payment at 4.5% from $1216 to 1378, cancelling out about one quarter of the benefit.

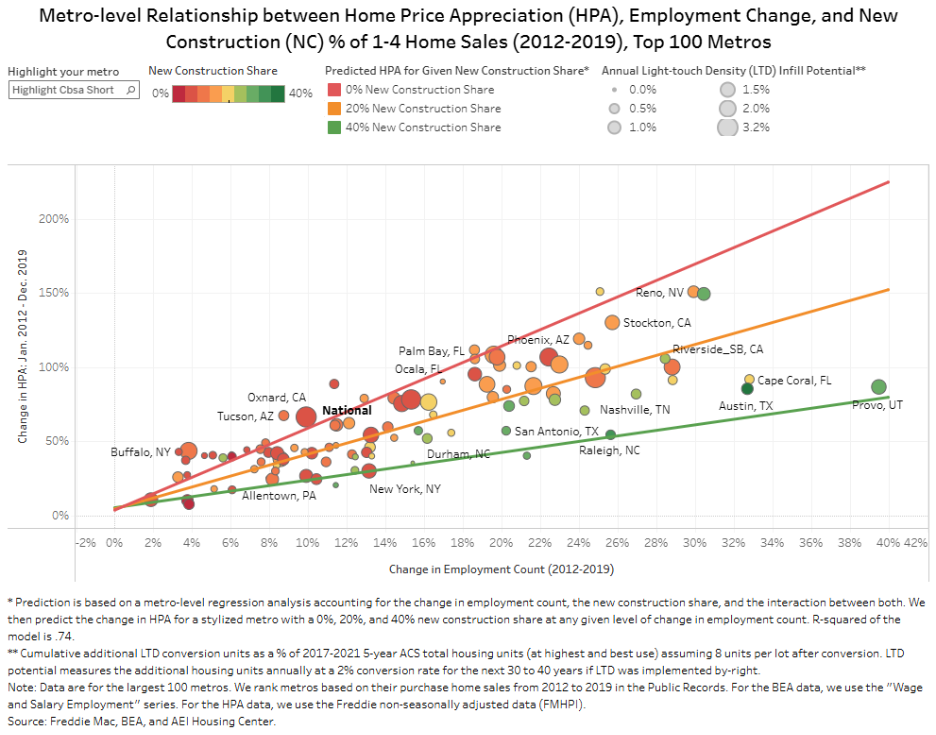

Both the supply increase and economic growth will likely not be evenly distributed, meaning some areas will see much higher HPA growth than others.

Further, the HPA increase could be even larger given higher levels of economic growth.

Finally, it is reasonable to infer it would take a very large increase in single-family home production (on the order of 50%-100%) to result in a 0% increase in cumulative HPA over the next three years.

There is broad agreement among housing analysts that the way to make housing more affordable is to build more homes.

President Trump and Congress could make housing more affordable by providing a small lot bounty to incentivize the states to allow the building of more starter homes currently made illegal by state and local lot size and other land use regulations.

1 HPA projections are based on various studies on the responsiveness of home prices to mortgage rates. See for example, https://www.dallasfed.org/research/economics/2023/0815 and https://libertystreeteconomics.newyorkfed.org/2021/09/the-housing-boom-and-the-decline-in-mortgage-rates/. It also considers the relationship at the metro level between housing stock, home price appreciation, and employment growth from 2012-2019.