Narrative")

- Eversource Energy has been reassessing its business mix, pulling back from offshore wind exposure while prioritizing its core regulated transmission and distribution operations amid higher grid upgrade costs and clean‑energy policy uncertainty.

- This shift, combined with cautious Wall Street views and ongoing regulatory risk, underscores how capital‑intensive infrastructure needs are reshaping the company’s risk profile.

- Next, we’ll examine how this renewed emphasis on core regulated operations influences Eversource Energy’s investment narrative for long‑term‑focused investors.

The latest GPUs need a type of rare earth metal called Neodymium and there are only 32 companies in the world exploring or producing it. Find the list for free.

What Is Eversource Energy’s Investment Narrative?

For someone considering Eversource Energy, the core belief is that a regulated electric and gas utility with established assets can still be attractive even as it cleans up past missteps. The recent slide in the share price toward its 52‑week low, alongside the decision to lean harder into core transmission and distribution while retreating from offshore wind, reinforces that the near‑term story is now less about growth projects and more about execution, regulation, and balance sheet strain from grid upgrades. Short term, the upcoming 2025 results and any update to capital plans or offshore wind exposure on the February earnings call look like the key catalysts, while interest coverage, free cash flow pressure from heavy capex, and persistent policy uncertainty remain front‑of‑mind risks that this latest news brings into sharper focus.

However, investors should also weigh how grid upgrade costs and policy shifts could pressure returns.

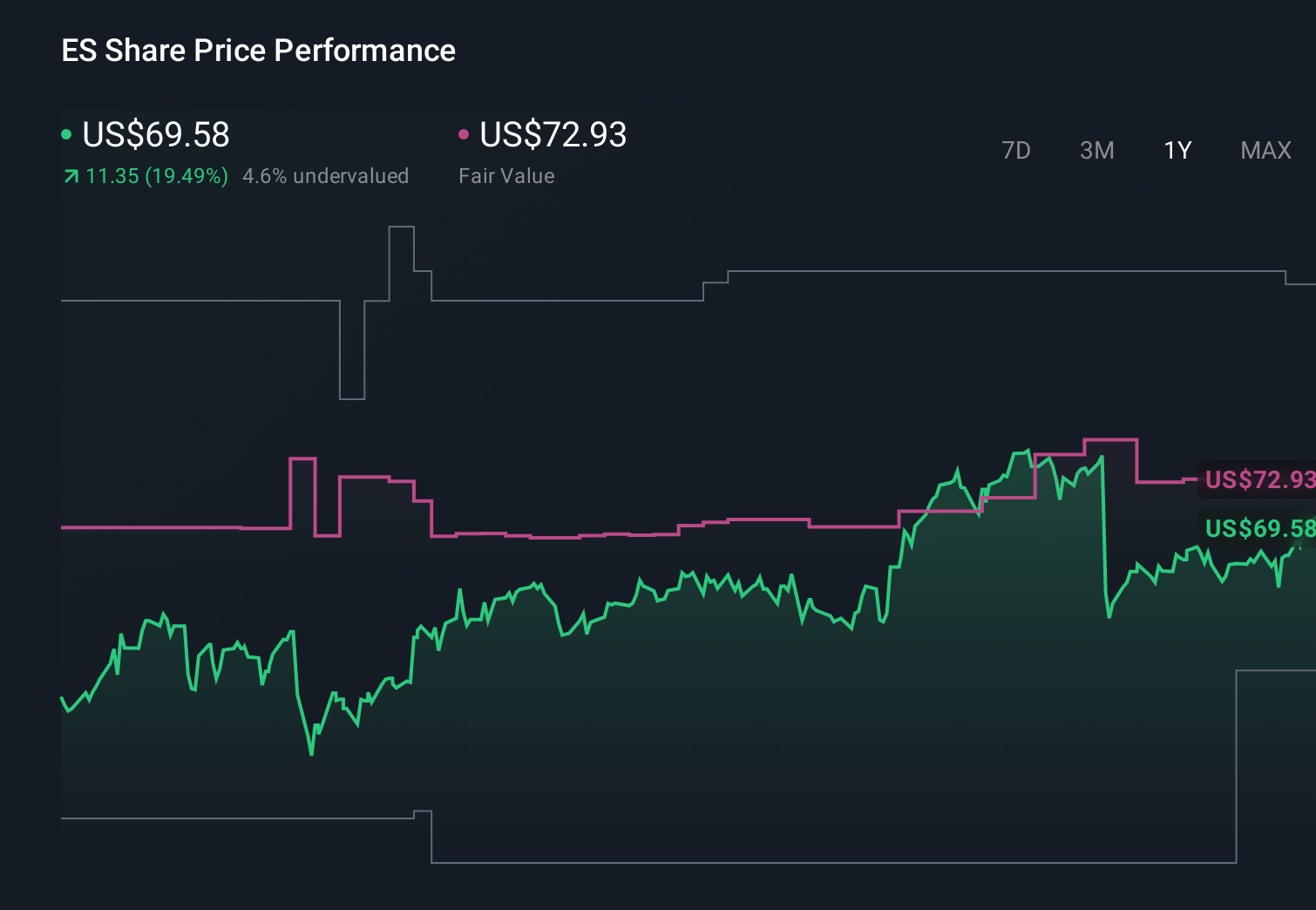

Despite retreating, Eversource Energy’s shares might still be trading above their fair value and there could be some more downside. Discover how much.Exploring Other Perspectives ES 1-Year Stock Price Chart Four fair value estimates from the Simply Wall St Community span roughly US$50 to a very large US$172, reflecting very different views on Eversource’s prospects. Set this against the current focus on regulated operations, rising grid investment needs, and ongoing regulatory risk, and you can see why opinions differ so widely on how the company’s performance may evolve.

ES 1-Year Stock Price Chart Four fair value estimates from the Simply Wall St Community span roughly US$50 to a very large US$172, reflecting very different views on Eversource’s prospects. Set this against the current focus on regulated operations, rising grid investment needs, and ongoing regulatory risk, and you can see why opinions differ so widely on how the company’s performance may evolve.

Explore 4 other fair value estimates on Eversource Energy – why the stock might be worth 28% less than the current price!

Build Your Own Eversource Energy Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don’t miss this chance:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if Eversource Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com