")

- Earlier in January 2026, National Bank of Canada completed a €998.94 million fixed-to-floating senior secured covered bond offering due 2032 and opened a new office in the Dubai International Financial Centre to support Canadian clients in the Middle East.

- These moves, alongside ongoing integration of Canadian Western Bank, signal an effort to broaden funding sources and deepen international and cross-border capabilities.

- We’ll now examine how the ahead-of-schedule Canadian Western Bank integration shapes National Bank of Canada’s broader investment narrative.

We’ve found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

What Is National Bank of Canada’s Investment Narrative?

To own National Bank of Canada, you need to be comfortable with a regional champion that is leaning harder into national scale and selective international reach. The ahead-of-schedule Canadian Western Bank integration remains the key short term catalyst, with revenue and cost synergies under close watch, especially given the bank’s higher-than-peer valuation multiples and only moderate earnings growth. The Dubai office and the €998.94 million covered bond are helpful, but they mainly fine tune funding flexibility and cross-border support rather than shift the investment case on their own. The ongoing lawsuit from fintech founders and a relatively low allowance for bad loans still sit near the top of the risk list, particularly if credit conditions or regulatory attention tighten.

However, one risk around loan losses and provisions is easy to underestimate at first glance and investors should be aware of it.

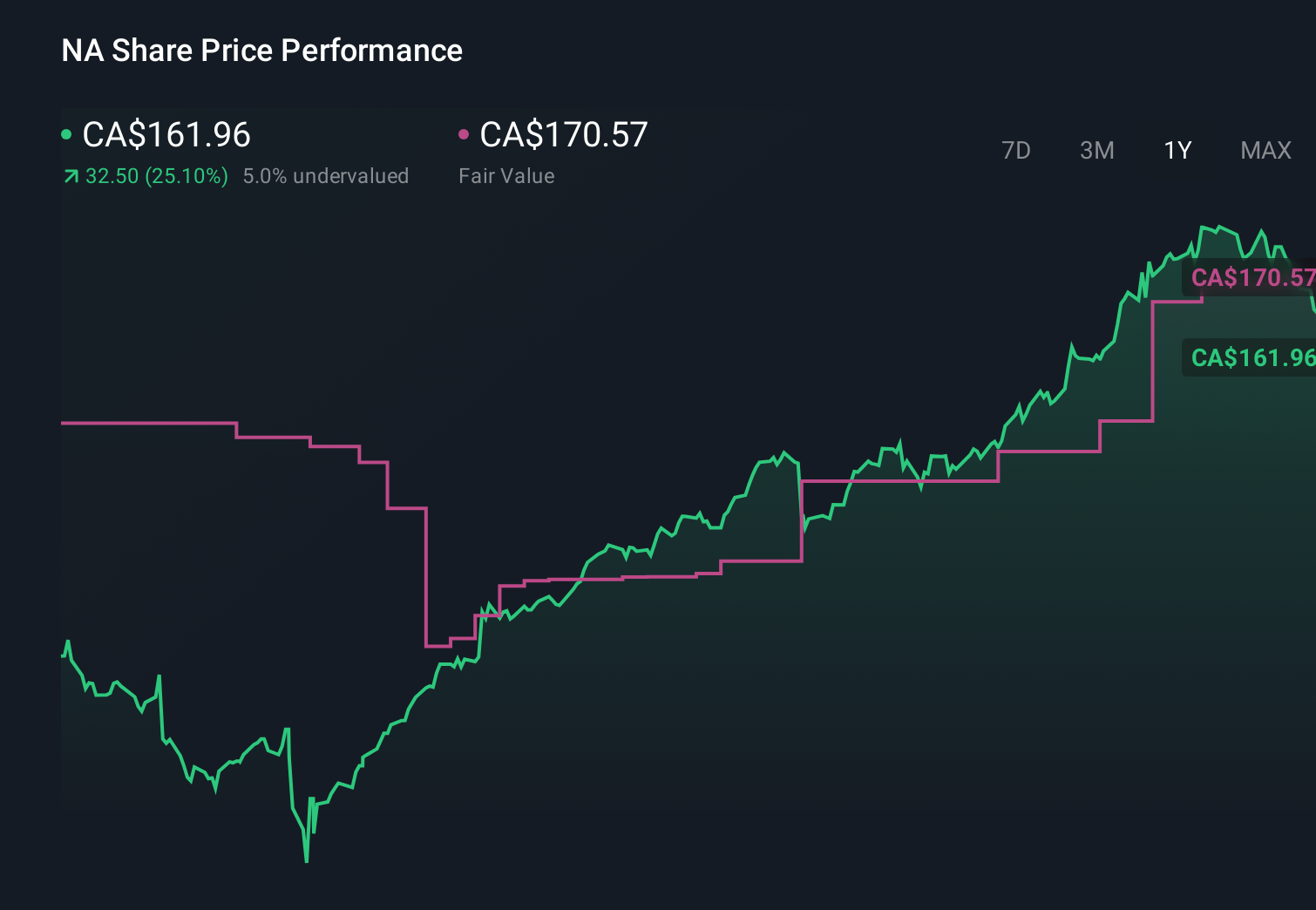

Despite retreating, National Bank of Canada’s shares might still be trading 34% above their fair value. Discover the potential downside here.Exploring Other Perspectives TSX:NA 1-Year Stock Price Chart

TSX:NA 1-Year Stock Price Chart

Three Simply Wall St Community valuations span from C$152.65 to about C$245.70, underlining how differently individual investors view National Bank of Canada. Set those views against the integration and legal risks discussed above and you start to see why it helps to weigh several perspectives before forming your own expectations for the bank’s performance.

Explore 3 other fair value estimates on National Bank of Canada – why the stock might be worth 6% less than the current price!

Build Your Own National Bank of Canada Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Curious About Other Options?

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if National Bank of Canada might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com