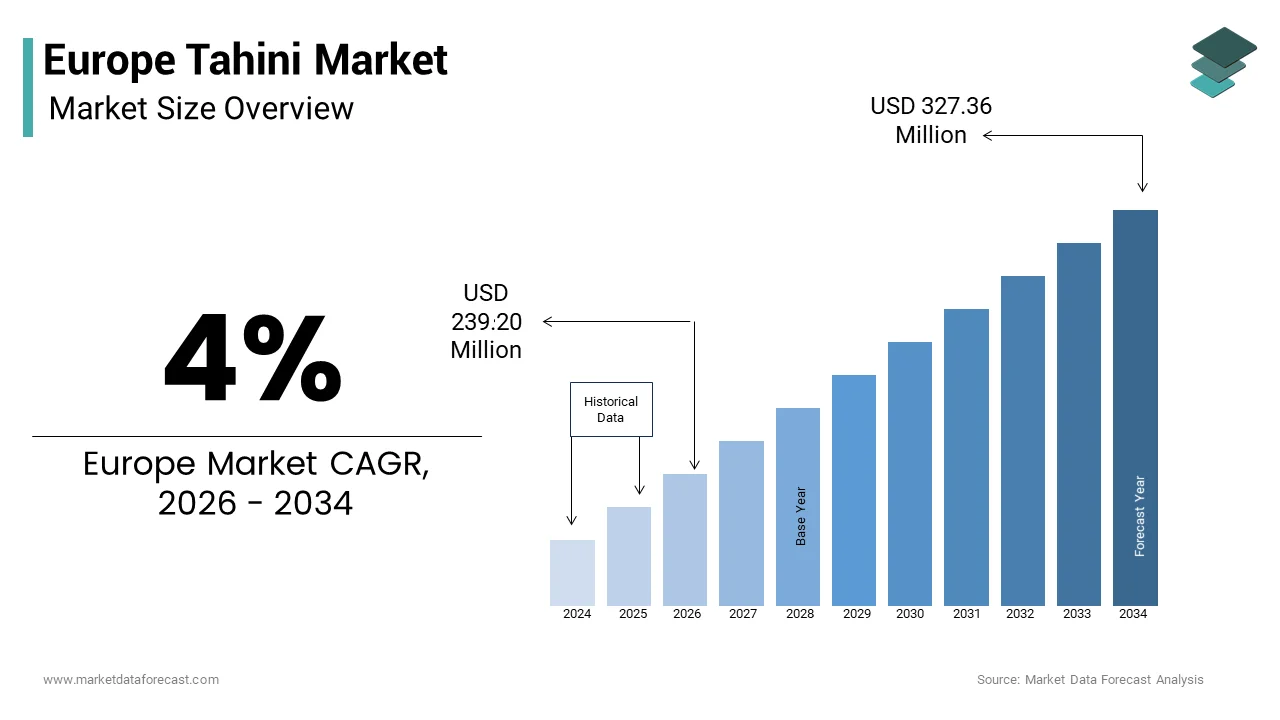

Europe Tahini Market Size

The European tahini market size was valued at USD 230 million in 2025 and is anticipated to reach USD 239.20 million in 2026 and USD 327.36 million by 2034, growing at a CAGR of 4% during the forecast period from 2026 to 2034.

Introduction of the European Tahini Market

Tahini is a smooth paste, or a seed butter, made from ground sesame seeds. Its integration into plant-based diets, Mediterranean cuisine revival, and clean-label food trends has accelerated consumer acceptance beyond traditional Middle Eastern communities. Europe’s growing multicultural demographics have significantly influenced pantry diversification, with tahini now featured in supermarkets, artisanal food stores, and food service menus from Lisbon to Helsinki. The increasing population of foreign-born individuals in the European Union, including those from non-EU nations, is fueling a growing demand for authentic, traditional, and diaspora-driven food products. Additionally, driven by the European Commission’s Farm to Fork Strategy and a widespread shift toward sustainable, healthier eating, a significant portion of European consumers are actively incorporating plant-based alternatives to dairy and animal fats into their diets, enhancing the appeal of nutrient-dense options like tahini. This cultural fusion and dietary recalibration have positioned tahini not merely as an import but as a locally resonant ingredient embedded in contemporary European gastronomy.

MARKET DRIVERS Rising Popularity of Plant-Based and Flexitarian Diets

The region’s dietary landscape is undergoing a fundamental transformation driven by environmental awareness, health consciousness, and ethical consumption, which in turn fuels the growth of the European tahini market. Tahini, as a plant-based source of healthy fats and protein, benefits directly from this shift. A significant portion of adults in the European Union are actively reducing their meat intake and adopting flexitarian diets, driven by concerns regarding health and the environment. Furthermore, Consumers in Western Europe are increasingly replacing animal fats with plant-derived alternatives, motivated by desires to improve heart health and enhance sustainability. Tahini’s versatility, as a base for sauces, dressings, desserts, and dairy-free alternatives, makes it an ideal ingredient for this demographic. Supermarket chains in Germany are rapidly expanding shelf space for products like tahini, reflecting a sharp increase in consumer demand for plant-based, versatile ingredients. The alignment of tahini with the clean label movement, containing typically only sesame seeds and sometimes salt, further enhances its appeal in a region where a notable share of consumers check ingredient lists before purchase. This convergence of dietary evolution and ingredient transparency solidifies tahini’s relevance in Europe’s evolving food culture.

Influence of Mediterranean and Middle Eastern Culinary Integration

The culinary fabric of the region is increasingly interwoven with flavors from the Eastern Mediterranean and Levant, with tahini serving as a cornerstone of this gastronomic exchange, thereby boosting the expansion of the European tahini market. Following the pandemic-related downturn in the food service sector, there has been a noticeable expansion of diverse and international dining options across the European Union, with a particular rise in popularity for Mediterranean-inspired fusion and Middle Eastern cuisine. Dishes such as hummus, baba ghanoush, and halva, all reliant on tahini, are now commonplace in urban food scenes from Paris to Stockholm. The European Travel Commission has observed a robust recovery in travel, with a growing number of European residents traveling to North African and Middle Eastern destinations, enhancing their familiarity with regional cuisine like tahini-based preparations. This experiential consumption often translates into home cooking adoption. Moreover, according to sources, the Mediterranean diet remains the most recommended eating pattern by nutritionists in Southern Europe, and tahini complements this model by providing monounsaturated fats and essential minerals. Culinary education platforms have seen a year-on-year increase in tahini-related recipe searches since 2022, indicating deepening consumer engagement beyond ethnic enclaves. This cultural resonance transforms tahini from an imported specialty into a domesticated pantry essential.

MARKET RESTRAINTS Price Volatility and Supply Chain Fragility of Sesame Seeds

Persistent pressure from the unstable global supply of sesame seeds, its sole primary ingredient, restrains the growth of the European tahini market. Most of the sesame used in European tahini production is imported, with major sources including Sudan, Ethiopia, India, and Myanmar. Driven by unpredictable climate events, export restrictions, and geopolitical instability in major producing nations, international sesame seed prices witnessed a steep upward trend over the 2021–2023 period. Civil conflict in 2023 severely crippled Sudan’s agricultural logistics, causing a significant disruption in its ability to export sesame, which necessitated a rapid shift in supply sources for European buyers. This dependency on politically and climatically vulnerable regions creates significant cost unpredictability for European tahini manufacturers. High import costs for sesame, stemming from supply shortages and logistical challenges, have forced European processors and brands to pass costs on to consumers or modify product formulations to maintain viability. Unlike staple oilseeds such as sunflower or rapeseed, sesame lacks strategic stockpiling mechanisms within the EU, leaving the tahini supply chain exposed. This fragility not only impacts profitability but also deters new entrants, thereby constraining market diversification and innovation in an otherwise growing sector.

Limited Consumer Awareness in Non-Urban and Northern European Regions

Tahini remains unfamiliar or underutilized across vast segments of Europe, particularly in rural and Northern regions, which inhibits the expansion of the European tahini market. This is despite its rising profile in cosmopolitan centers. According to a study, only a portion of households in the Baltic states, Finland, and parts of Central Europe could correctly identify tahini or describe its use, compared to those in France, Spain, and the Netherlands. This knowledge gap translates into low trial rates and minimal repeat purchases outside major cities. The absence of contextual culinary education, such as how to store tahini, prevent oil separation, or substitute it in baking, further hinders adoption. Additionally, mainstream advertising rarely features tahini, with food marketing budgets in Northern Europe heavily skewed toward dairy and conventional spreads. Tahini may remain a specialized ingredient unless it is actively integrated into school nutrition programs, retail demos, and online recipe content. This uneven geographic and demographic awareness acts as a structural brake on market expansion, despite favorable macro trends in plant-based eating.

MARKET OPPORTUNITIES Expansion of Clean Label and Organic Retail Channels

The region’s robust organic and clean-label retail infrastructure offers a high-potential growth corridor for premium tahini products, which is anticipated to propel the growth of the European tahini market. The European organic landscape is experiencing significant growth, with pantry essentials like nut and seed butters acting as key drivers. Tahini, particularly when certified organic and produced with non-roasted or stone-ground methods, aligns seamlessly with this consumer preference for minimally processed, traceable ingredients. Major European organic retailers are notably broadening their selection of tahini products to meet rising demand, emphasizing variants that highlight ethical sourcing and local production. Modern organic shoppers are increasingly drawn to “clean label” products with minimal components, a preference that naturally favors tahini due to its typically singular ingredient list. Furthermore, the EU’s updated Organic Regulation has streamlined certification for imported sesame, enabling more small-scale ethical suppliers to enter the European market. This regulatory and retail alignment creates a fertile environment for differentiated tahini offerings that emphasize terroir, artisanal production, and ethical sourcing, thereby unlocking value beyond commodity pricing and appealing to Europe’s conscious consumer base.

Innovation in Food Service and Ready Meal Applications

The European food service and convenience food sector provides a dynamic opportunity for the European tahini market. Plant-based dips and spreads are gaining significant traction in the retail and ready-meal sector, with a growing consumer preference for healthier, plant-forward options. Tahini-based dressings are increasingly featured in meal subscription kits, while Mediterranean ingredients, including tahini, are experiencing rising popularity on European restaurant menus. The ingredient’s emulsifying properties and rich mouthfeel make it an ideal dairy-free alternative in creamy dressings and sauces, aligning with the industry’s push to reduce animal-derived ingredients. In the UK, major supermarket chains launched several new tahini-infused ready meals. This application diversification not only expands consumption occasions but also normalizes tahini as a versatile kitchen staple rather than an ethnic specialty. Strategic partnerships between tahini producers and food developers can further accelerate this trend, embedding the ingredient into Europe’s evolving convenience food ecosystem.

MARKET CHALLENGES Stringent Food Safety and Import Compliance Regulations

European Union food safety protocols, while ensuring high quality, pose significant entry barriers for tahini producers, especially small-scale exporters from sesame-producing countries, which acts as a major challenge to the European tahini market. The European Union continues to heavily monitor and reject imported sesame products due to the presence of ethylene oxide, a sterilizing agent banned for agricultural use in the EU but still utilized in certain exporting regions. In 2022, a widespread recall of sesame paste from multiple brands followed the detection of this substance, as per sources. Compliance with EU regulations requires rigorous batch testing, traceability documentation, and adherence to maximum residue levels, which many artisanal or cooperative producers cannot afford. A significant majority of sesame processors in key African export markets face challenges in meeting strict European food safety standards without external assistance to address compliance gaps. These compliance costs are ultimately borne by European importers, inflating end prices and limiting the availability of authentic, small-batch tahini. The regulatory burden thus creates a paradox: while European consumers seek ethical and traditional foods, the system inadvertently favours large industrial suppliers with compliance infrastructure, curtailing product diversity and authenticity in the marketplace.

Intense Competition from Established Plant-Based Spreads

Well-entrenched plant-based spreads such as peanut butter, almond butter, and sunflower seed butter, all of which benefit from decades of brand recognition and distribution scale, pose a serious obstacle to the European tahini market. According to research, peanut butter holds a significant value share of the nut and seed butter category, with almond butter at a notable share, leaving alternative pastes like tahini with a lesser share. Major brands such as Calvé, Meridian, and Rapunzel allocate minimal marketing resources to tahini compared to their core products, reducing visibility. Unlike nut butters, which are often sweetened and positioned as breakfast or snack items, tahini’s savory and slightly bitter profile requires consumer education to drive habitual use. Tahini is often treated as a secondary ingredient, not a primary pantry staple, due to a lack of clear differentiation in the market. This competitive inertia hampers trial and loyalty building, even as overall plant-based spread consumption continues to rise across the region.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

4%

Segments Covered

By Product, Source, Nature, Packaging, End-User, Category, Color, Claim, And By Region

Various Analyses Covered

Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe

Market Leaders Profiled

HAITOGLOU BROS S.A., Prince Tahina Ltd., Sesame & Tahina Food Industries Ltd., Meridian Foods Limited, Grecious, Beyda Gida San. Tic. A.S., Inci Food Industry, Dipasa Europe B.V., Tahini Royal, Shamir, Al’Fez, Skoulikas Bedford Ltd, TAMPICO TRADING GmbH, meletiadis.gr., EDN, Carleys, Citir Susam, MED CUISINE, Al Wadi Al Akhdar, and BIONA, among others.

SEGMENTAL ANALYSIS By Product Insights

The paste or pure tahini segment dominated thEuropeanpe tahini market by accounting for a substantial share in 2025. The dominance of the paste or pure tahini segment is driven by its versatility, clean ingredient profile, and foundational role in both traditional and modern culinary applications. Pure tahini contains only ground sesame seeds, often hulled, and sometimes a trace of salt, aligning with Europe’s strong clean label movement. European consumers are increasingly prioritizing health by actively reducing their intake of products containing artificial additives and preservatives, favoring, in turn, simpler, minimally processed foods. Furthermore, the demand for authentic, plant-based dips across the European Union has made high-quality tahini a critical ingredient in the production of mainstream hummus and baba ghanoush, solidifying its place in retail and food service. Its neutral yet rich flavor profile also enables seamless integration into dairy-free baking, smoothies, and savory sauces, broadening its utility beyond niche ethnic dishes. This functional adaptability, combined with consumer trust in ingredient simplicity, sustains pure tahini’s market leadership across diverse European food cultures.

The seasoned tahini segment is likely to experience the fastest CAGR of 11.3% between 2026 and 2034 due to rising demand for convenient, ready-to-use flavor enhancers that align with evolving taste preferences and time-constrained lifestyles. According to research for 2024, European consumers are increasingly seeking condiments that provide both complex flavor profiles and functional health benefits, a trend favoring enhanced tahini products infused with various herbs and spices. Retail innovation has further catalyzed uptake. In 2023, French retailer Carrefour observed significant consumer uptake for its private label specialty food items, with new, flavored savory spreads, such as tahini, demonstrating high loyalty among shoppers. Additionally, the food service sector’s embrace of global fusion cuisine, particularly Levantine and modern Mediterranean, has normalized seasoned tahini as a chef’s preferred finishing element. Data indicates that the Netherlands’ hospitality sector experienced a notable rise in menu mentions of diverse tahini variations in 2023, reflecting a growing consumer preference for Mediterranean-inspired, plant-forward condiments. This convergence of convenience, flavor exploration, and culinary versatility propels seasoned tahini’s rapid ascent.

By Nature Insights

The conventional or inorganic tahini segment led the European tahini market by capturing a significant share in 2025. The leading position of this segment is attributed to lower production costs, broader availability, and established import supply chains from major sesame exporting nations such as India, Ethiopia, and Sudan. The vast majority of conventional sesame imported into the European Union is utilized for non-organic food processing, while organic sesame constitutes a significantly smaller, though growing, portion of the total import volume. Stringent EU food safety regulations regarding pesticide residues and contamination continue to heavily influence market dynamics and supplier sourcing. This scale enables competitive retail pricing. Additionally, mainstream supermarket chains, which account for a significant share of tahini sales in Europe, prioritize shelf space for high turnover, cost accessible products. The affordability and consistent supply of conventional tahini make it the default choice for bulk buyers in the food industry and budget-conscious households, particularly in Central and Eastern Europe, where price sensitivity remains high. These structural, al economic, and distribution advantages sustain the conventional segment’s market primacy despite rising organic interest.

The organic tahini segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 12.7% during the forecast period, owing to Europe’s deepening commitment to sustainable agriculture and clean eating, particularly among urban, high-income demographics. Germany leads this shift. Organic tahini sales there increased year on year. The EU’s revised Organic Regulation has also streamlined certification for imported sesame, enabling more ethical suppliers from Uganda and Tanzania to access European shelves with verified organic status. Furthermore, consumers increasingly associate organic tahini with superior taste and purity. Premium retailers and direct-to-consumer e-commerce platforms have capitalized on this perception, offering traceable, single-origin organic tahini at premium margins, thereby accelerating category growth beyond niche health food stores.

By Packaging Insights

The glass jars segment was the largest in the European tahini market by securing a 58.5% share in 2025 because of consumer perception of glass as inert, non-reactive, and protective of tahini’s delicate oil composition. European consumers widely perceive glass as the superior material for preserving the freshness and flavor of food products compared to plastic or metal alternatives. Major brands such as Al Arz, Kevala, and Rapunzel have long standardized on amber or clear glass jars, reinforcing category norms. Additionally, glass aligns with Europe’s circular economy goals. Additionally, research indicates that glass maintains a very high recycling rate, ranking as a top-performing packaging material in the European Union’s circular economy. Retailers also favor jars for their premium shelf presence and resealability, critical for a product prone to oil separation. In France and Italy, where tahini is increasingly used in gourmet cooking, glass jar packaging is associated with artisanal quality, further entrenching its dominance. The format’s compatibility with both ambient and chilled storage, coupled with strong consumer trust, secures its leading position despite higher weight and transport costs.

The sachets segment is expected to exhibit a noteworthy CAGR of 14.2% from 2026 to 2034. The rapid expansion of the sachets segment is propelled by the rise of single-serve convenience, food service innovation, and trial-driven marketing strategies. Driven by demand for sustainability and portion control, plant-based condiment options are increasingly appearing in food service, reflecting a broader industry shift toward smaller, eco-conscious packaging formats. Meal kit companies like HelloFresh and Gousto now include 20-gram tahini sachets in Mediterranean-inspired recipes, eliminating measurement friction and waste. In the UK, high-street food-to-go brands are successfully expanding their plant-based menu options, with additions like tahini-based dressings driving significant growth in popularity among consumers. Moreover, sachets lower the barrier to first time trial. Lightweight and low cost, sachets also reduce logistics emissions, critical for brands pursuing carbon neutrality under the EU Green Deal. These functional, commercial, and sustainability advantages position sachets as the vanguard of tahini packaging evolution.

By End User Insights

The domestic or household segment held the majority share of 54.4% of the European tahini market in 2025. The prominence of the domestic or household segment is credited to rising culinary curiosity and the proliferation of online recipe content. Consumer interest in tahini-based recipes has risen significantly across key European markets, driven by the popularity of Mediterranean flavors and plant-based diets. Supermarkets have responded by expanding tahini offerings in the condiment and international foods aisles. The leading Spanish supermarket chain has expanded its selection of tahini products to meet growing demand for diverse and healthy, plant-based food items. The pandemic era also normalized pantry stockpiling of versatile staples, with tahini’s long shelf life and multi-use functionality, applicable in dressings, desserts, and protein bowls, enhancing its household appeal. Furthermore, tahini has become an increasingly common pantry staple in younger European households, indicating a shift toward incorporating diverse, plant-based, and nutrient-dense ingredients into home cooking. This generational shift toward global, plant-centric cooking ensures sustained household demand, making it the bedrock of the European tahini market.

The food service segment is estimated to register the fastest CAGR of 13.1% from 2026 to 2034. The swift growth of this segment is fuelled by the professionalization of Middle Eastern and Levantine cuisine in European restaurants, coupled with chefs’ pursuit of clean, functional plant-based ingredients. In European urban centers, particularly within Italy, Belgium, and Sweden, tahini is increasingly utilized in new culinary offerings as a popular plant-based emulsifier and finishing sauce. The rise of “vegetable-forward” fine dining has further elevated tahini’s status. Michelin-starred restaurants in Copenhagen and Barcelona feature house-made tahini in composed vegetable dishes, signaling culinary legitimacy. Besides, the contract catering sector is adopting tahini for institutional menus. Sodexo has expanded the use of plant-based, nutrient-dense ingredients like tahini in its corporate cafeteria menus to improve the taste and appeal of plant-based meals. The growth is also amplified by delivery and cloud kitchen models, where tahini enhances perceived authenticity in Mediterranean bowls and wraps without requiring refrigeration. This professional endorsement and operational adaptability cement the food service sector as the most dynamic consumption channel.

COUNTRY ANALYSIS Germany Tahini Market Analysis

Germany was the top performer in the European tahini market by accounting for a 18.4% share in 2025. The dominance of the German market is driven by its robust health food culture, large Middle Eastern diaspora, and advanced organic retail infrastructure. The significant population of Turkish and Arab descent in Germany, as documented by official statistics, establishes a strong and enduring foundation for demand for related cultural food products. Beyond ethnic consumption, tahini has permeated mainstream wellness diets. Recent dietary trends in Germany indicate a growing consumer preference for plant-based fats, with Mediterranean-influenced ingredients, such as tahini, gaining prominence in everyday diets. The organic segment is particularly strong. Germany accounts for a portion of all organic tahini sales in Europe. Major retailers like Alnatura and Denn’s carry over a dozen tahini variants, including stone-ground and fair-trade options. Additionally, Germany’s strong manufacturing base supports local tahini production using imported sesame, reducing supply chain latency. This blend of demographic, cultural, and commercial factors solidifies Germany’s position as the continent’s tahini epicenter.

United Kingdom Tahini Market Analysis

The United Kingdom was the next prominent player in the European tahini market by capturing a 15.2% share in 2025. The growth of the Uk market is propelled by its highly cosmopolitan food culture and rapid adoption of global plant-based trends. London hosts numerous Middle Eastern restaurants, and tahini has transcended ethnic boundaries to appear in mainstream supermarkets like Tesco and Sainsbury’s, which together stock several tahini SKUs. Monthly consumption of tahini by British adults has significantly increased in recent years, according to consumer trends. The rise of meal kits has been instrumental. Tahini has become a frequently used ingredient in HelloFresh UK’s plant-based recipe offerings, increasing consumer exposure to the product. Additionally, British consumers show strong openness to innovation. The UK market has seen rapid growth in flavored tahini sales, with the region showing high consumer demand compared to other regions in Europe. The country’s departure from the EU has also spurred new import partnerships with non-traditional sesame suppliers, enhancing supply diversity. These dynamics make the UK a high velocity, innovation-led tahini market.

France Tahini Market Analysis

France holds a noteworthy share of the European tahini market, where the ingredient has been seamlessly woven into the country’s evolving gastronomic identity. French consumers, long champions of rich sauces and emulsions, have embraced tahini as a modern alternative to dairy-based preparations. The Mediterranean diet’s influence is particularly pronounced in southern regions like Provence, where a notable share of households report using tahini in cooking. Major brands such as Markal and Lima dominate organic shelves, while Carrefour’s private label tahini ranks among the top five best-selling international condiments in its stores. Culinary schools, including Le Cordon Bleu,u have also incorporated tahini into plant-based curriculum modules, signaling institutional acceptance. France’s unique fusion of traditional culinary rigor and openness to global ingredients positions it as a sophisticated and growing tahini market.

Italy Tahini Market Analysis

Italy experienced a consistent expansion in the European tahini market, with growth propelled by the synergy between Mediterranean dietary patterns and rising interest in Levantine flavors. Although not traditionally Italian, tahini is increasingly used in vegan reinterpretations of classic dishes, such as replacing butter in pesto or enriching vegetable purées. According to studies, plant-based fat consumption rose in urban centers like Milan and Rome over the years, with tahini among the fastest adopted. The country’s strong artisanal food ethos favors stone-ground, small-batch tahini, often sold in specialty stores and organic cooperatives. Importantly, Italy’s proximity to North Africa facilitates stable sesame supply routes. Italian tahini importers sourced a portion of their sesame from Tunisia and Egypt. Besides, food tourism plays a role; cooking classes in Tuscany and Sicily routinely include tahini-based recipes to cater to international visitors. This cultural adaptability ensures Italy’s steady ascent in the tahini landscape.

Netherlands Tahini Market Analysis

The Netherlands is predicted to expand in the European tahini market over the forecast period due to its progressive food innovation ecosystem and high per capita consumption of plant-based products. Dutch consumers lead Europe in openness to alternative proteins and fats. Amsterdam’s diverse food scene, with numerous Middle Eastern eateries, acts as a cultural incubator for tahini adoption. Retail penetration is equally strong. Albert Heijn, the country’s largest supermarket chain, stocks tahini in most of its stores and reported a sales increase. The Netherlands also serves as a logistics hub. Rotterdam Port handles a portion of the EU’s sesame imports, enabling efficient distribution to neighboring countries. Furthermore, Dutch food tech startups are exploring tahini fortification with omega-3s and probiotics, signaling product evolution beyond traditional uses. This combination of logistical advantage, consumer openness, and innovation cements the Netherlands as a pivotal and expanding tahini market.

COMPETITIVE LANDSCAPE

The European tahini market features a moderately fragmented competitive landscape with a mix of international specialty brands, regional organic producers, and private label entrants. While no single player dominates the entire region, competition intensifies in Western and Northern Europe, where consumer awareness and retail penetration are highest. Established brands distinguish themselves through ingredient quality, production methods, and ethical sourcing narratives, while newer entrants focus on flavor innovation and convenient packaging. Private label offerings from major supermarket chains exert pricing pressure, particularly in the conventional segment, prompting branded players to emphasize premium attributes such as stone grinding, organic certification, and origin transparency. Competition also extends to digital channels, wheredirect-to-consumerr models and social media-driven recipe marketing influence trial and retention. Food service partnerships have become a critical battleground, as restaurants and meal kit providers shape perception and usage occasions. Overall, rivalry centers on authenticity, convenience, and sustainability, with players continuously adapting to evolving European dietary preferences and regulatory standards to capture share in this growing plant-based category.

KEY MARKET PLAYERS

A few of the market players that are dominating the European tahini market are

- HAITOGLOU BROS S.A.

- Prince Tahina Ltd.

- Al Arz Tahini

- Kevala

- Rapunzel

- Sesame & Tahina Food Industries Ltd

- Meridian Foods Limited

- Grecious, Beyda Gida San. Tic. A.S.

- Inci Food Industry

- Dipasa Europe B.V.

- Tahini Royal

- Shamir

- Al’Fez

- Skoulikas Bedford Ltd

- TAMPICO TRADING GmbH

- meletiadis.gr.

- EDN

- Carleys

- Citir Susam

- MED CUISINE

- Al Wadi Al Akhdar

- BIONA, among others.

Top Players In The Market

- Al Arz Tahini is a leading producer of premium tahini with deep roots in Middle Eastern culinary tradition and a strong footprint across Europe. The company supplies both pure and seasoned tahini variants to major retail chains and food service distributors in Germany, France, and the Netherlands. In recent years, Al Arz has invested in sustainable sesame sourcing partnerships in Ethiopia and enhanced its production facility certifications to meet stringent EU organic and food safety standards. These efforts have improved product consistency and reinforced its reputation for authenticity among European consumers seeking traditional yet compliant tahini products.

- Kevala is a dynamic player known for itsorganic stone-ground tahini and innovative flavored variants tailored to Western palates. The brand has gained traction in health food stores and premium supermarkets across the United Kingdom, Sweden, and Denmark. Kevala recently launched a recyclable glass jar with an airtight seal to address consumer concerns about oil separation and freshness. Additionally, the company expanded its e-commerce logistics network to offer direct-to-consumer delivery across continental Europe, significantly improving accessibility and brand visibility among conscious urban shoppers.

- Rapunzel is a German-based pioneer in organic food products with a longstanding presence in the European tahini segment. The company integrates tahini into its broader portfolio of nut and seed butters, emphasizing traceability and fair trade principles. Rapunzel sources sesame through long-term contracts with certified organic cooperatives in Uganda and India, ensuring ethical supply chains.

Top Strategies Used By The Key Market Participants

Key players in the European tahini market prioritize clean label formulation by using only hulled sesame seeds and minimal additives to meet consumer demand for transparency. They actively invest in organic certification and ethical sourcing to align with EU sustainability regulations and conscious consumption trends. Product diversification through flavored and functional variants, such as lemon garlic or omega-enriched tahini, enables broader culinary appeal. Strategic partnerships with meal kit companies and food service providers facilitate trial and habitual use. Companies also upgrade packaging with recyclable materials and resealable features to enhance user experience and reduce waste. Continuous innovation in production technology ensures shelf stability without preservatives. Retail expansion into mainstream supermarkets alongside ethnic and organic channels broadens accessibility. Digital engagement through recipe content and social media builds brand loyalty among younger demographics. These integrated strategies strengthen market relevance and competitive differentiation across diverse European consumer segments.

MARKET SEGMENTATION

This research report on theEuropeane Tahini market is segmented and sub-segmented into the following categories.

By Product Type

- Paste/Pure Tahini

- Seasoned Tahini

- Others

By Source

- Hulled Sesame

- Dehulled Sesame

By Nature

- Conventional/Inorganic

- Organic

By Category

By Color

By Packaging Type

- Bottles

- Tubs

- Sachets

- Jars

- Tins

- Drum/Bucket

- Others

By Claim

- Dairy Free

- Fat Free

- Nut Free

- Soy Free

- Gluten Free

- Preservative Free

- Non-GMO

- Vegan

- With all the above claims

- Regular (No Claims)

By End-User

- Domestic/Household

- Food Service Sector

- Food Industry

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe