The EU unveiled its latest sanctions package on Russia last week. This didn’t receive much press coverage – presumably because it’s the 20th such package and fatigue has set in – but the measures announced signal an important change in approach that’s worth discussing. That’s what I’m going to do in today’s post.

Up until this package, the EU had focused on sanctioning as many shadow fleet oil tankers as possible. The goal was to shut down this fleet and force Russia to switch back to using Western-owned oil tankers. That would improve enforcement of the G7 oil price cap, which the shadow fleet was circumventing. The big problem with this approach has been that the Trump administration didn’t join the EU in sanctioning the shadow fleet. US sanctions pack a punch that EU sanctions just don’t and – as a result – the shadow fleet continued to operate pretty much unfettered in the Baltic.

The latest sanctions package changes tack. It prohibits the provision of maritime services – most importantly insurance – to ships transporting Russian oil. This will shut down any Western-owned oil tankers that are still transporting Russian oil and marks a shift from going after the shadow fleet. It also marks a de facto end for the G7 price cap, since export capacity will now shift almost entirely to the shadow fleet that operates outside the cap. This shift in strategy presumably stems from the Trump administration’s reluctance to join the EU in sanctioning shadow fleet ships, which makes it entirely understandable. But there’s a problem. Inevitably, the shadow fleet will now become even more important in the Baltic. These are old ships that pose a grave environmental hazard. Ultimately, there’s no way around shutting this fleet down. Ben Harris and I just released a paper that proposes a new way to do this.

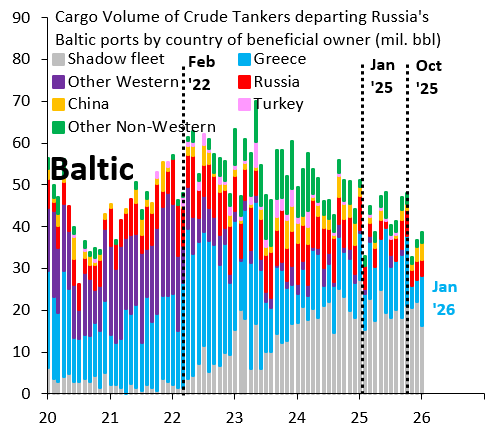

The chart above shows monthly export volumes out of Russia’s Baltic ports and is based on daily data on oil tanker departures from Bloomberg’s AHOY function. The chart breaks down tanker traffic by country of ownership. There’s only one Western country that’s still operating meaningful tanker capacity out of Russia’s Baltic ports and that’s Greece (blue bars). Greek ships in recent months have made up between 15 and 30 percent of total capacity. This number will now go down to zero and leave Russia scrambling for capacity. This may put additional downward pressure on the Urals oil price, which is already trading at a record discount versus Brent in the wake of US sanctions on Rosneft and Lukoil. The EU’s maritime services ban therefore packs a real punch and will hurt Russia in the short term.

In the medium term, however, Russia will source additional shadow fleet capacity, including from Greece’s shipping magnates who continue to sell oil tankers to the shadow fleet. This means that capacity in the Baltic will migrate almost entirely to the shadow fleet, which can’t be a positive outcome given how old and poorly maintained these vessels are. A big oil spill is only a matter of time. There’s sadly no way around shutting down the shadow fleet. The 20th sanctions package dodges this issue, which mutes its effectiveness.