- Baker Hughes (NasdaqGS:BKR) agreed a multiyear preferred provider deal with Marathon Petroleum to supply hydrocarbon treatment solutions across U.S. refineries.

- The company secured new contracts to support a low carbon ammonia facility for Wabash Valley Resources.

- Baker Hughes expanded its partnership with Hydrostor to provide technology for advanced energy storage projects.

For you as an investor, these moves illustrate how Baker Hughes is working across both established refining activity and newer low carbon projects. The company supplies equipment and services across the energy value chain, and these agreements extend that reach into downstream chemicals, clean ammonia and long duration storage technology.

In considering the company, you may factor in how these contracts affect Baker Hughes’ mix of revenue sources between traditional energy and transition related projects. The breadth of end markets touched by these deals also gives you additional areas to monitor, including refinery operations, ammonia production and grid scale storage projects.

Stay updated on the most important news stories for Baker Hughes by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Baker Hughes.

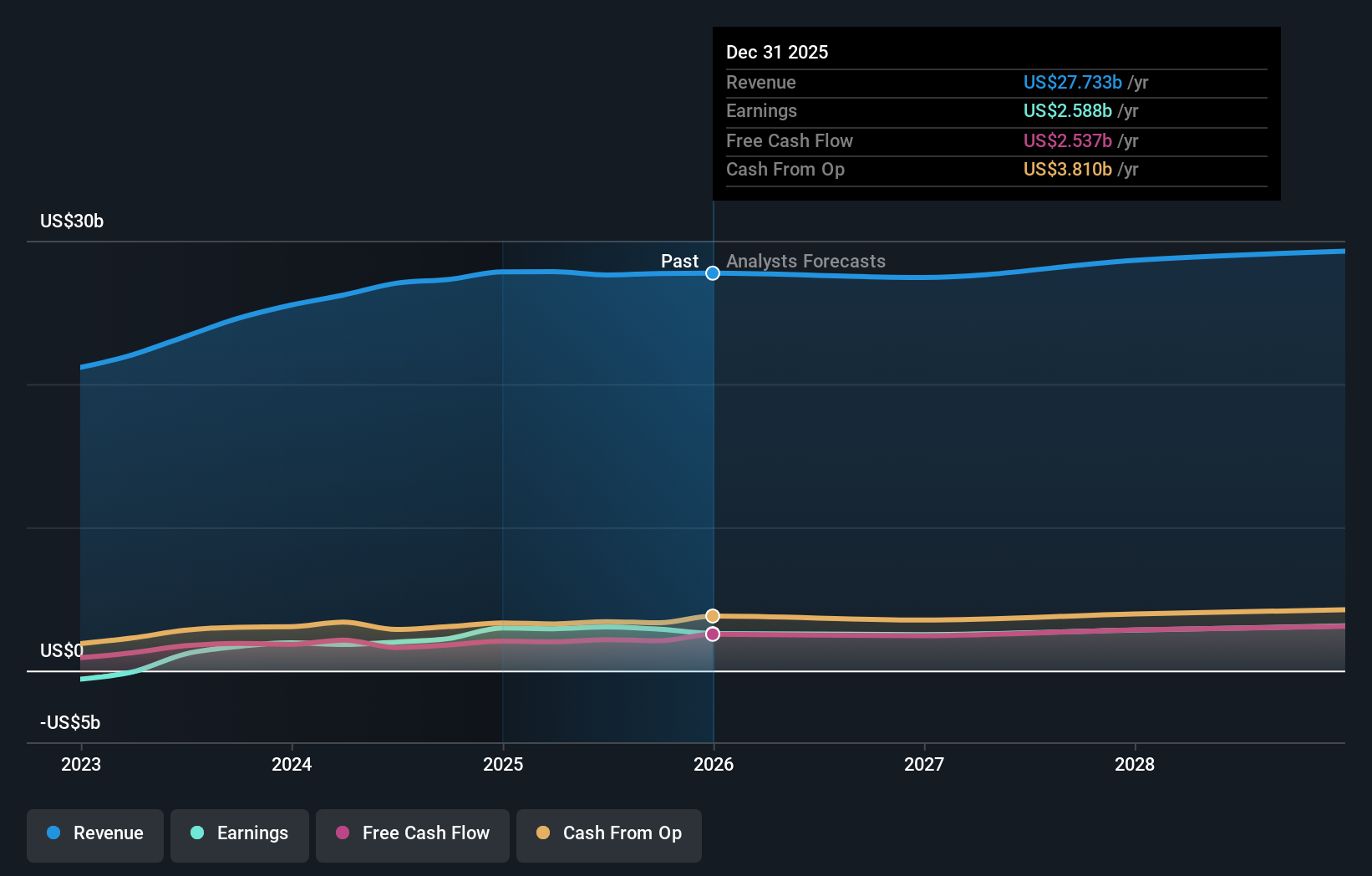

NasdaqGS:BKR Earnings & Revenue Growth as at Feb 2026

NasdaqGS:BKR Earnings & Revenue Growth as at Feb 2026

How Baker Hughes stacks up against its biggest competitors

The new Baker Hughes agreements point in two directions at once: deeper ties with a major refiner in Marathon Petroleum and wider exposure to energy transition projects through Wabash Valley Resources and Hydrostor. For you, that means the company is reinforcing its core hydrocarbon-chemicals business while also plugging its compression and storage equipment into low carbon ammonia and long-duration storage projects that could sit alongside offerings from peers like Schlumberger and Halliburton.

Baker Hughes narrative, from traditional energy to transition projects

These contracts line up with the existing narrative that Baker Hughes is leaning into energy transition markets and technology-driven services while still serving conventional oil and gas clients. A preferred-provider role at 12 refineries and two renewable fuel facilities, plus equipment across hydrogen, CO2 capture and grid-scale storage, fits that story of using its industrial and energy technology portfolio to build a broader mix of recurring, project-based work.

Risks and rewards to keep in mind

- Large multiyear work scopes with Marathon and Hydrostor add visibility to equipment and services tied to both downstream refining and energy storage.

- The Wabash Valley Resources plant and Hydrostor pipeline broaden exposure to clean ammonia, hydrogen and CO2 management projects that some investors see as structurally important themes.

- Execution risk is present across multiple complex projects, and any delays, cost issues or regulatory hurdles could affect timing of benefits from these contracts.

- Baker Hughes still competes with sizeable rivals like Schlumberger and Halliburton, so pricing, margins and future awards are not guaranteed in these segments.

What to watch next

From here, you might track how quickly these agreements convert into booked orders, reported backlog and follow-on work, as well as any disclosures on profitability of energy-transition-related projects compared with traditional service lines. If you want to see how other investors are thinking about this mix of opportunities and risks, take a look at the community views on Baker Hughes by checking the narratives that investors are sharing about the stock.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if Baker Hughes might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com