Find your next quality investment with Simply Wall St’s easy and powerful screener, trusted by over 7 million individual investors worldwide.

-

KBC Group (ENXTBR:KBC) has acquired Business Lease Czech Republic and Slovakia, expanding its leasing footprint in Central Europe.

-

The transaction covers Business Lease operations in both countries and adds to KBC Group’s existing leasing activities in the region.

-

Following a record year, KBC Group also announced an extraordinary collective bonus for employees.

KBC Group is a banking and insurance group with a strong presence in Central Europe, and leasing is a key part of its broader financial services offer. By adding Business Lease Czech Republic and Slovakia, the group increases its reach across two important markets for corporate and retail clients that use vehicle and equipment leasing. For you as an investor, it ties the group more closely to real economy activity in these countries.

The extraordinary bonus for staff following a record year points to a culture that links company performance with employee rewards. That can influence retention, morale and, over time, service quality across KBC’s banking, insurance and leasing units. As you assess ENXTBR:KBC, these moves sit alongside traditional metrics such as capital position, asset quality and dividend policy when you think about the group’s longer term positioning.

Stay updated on the most important news stories for KBC Group by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on KBC Group.

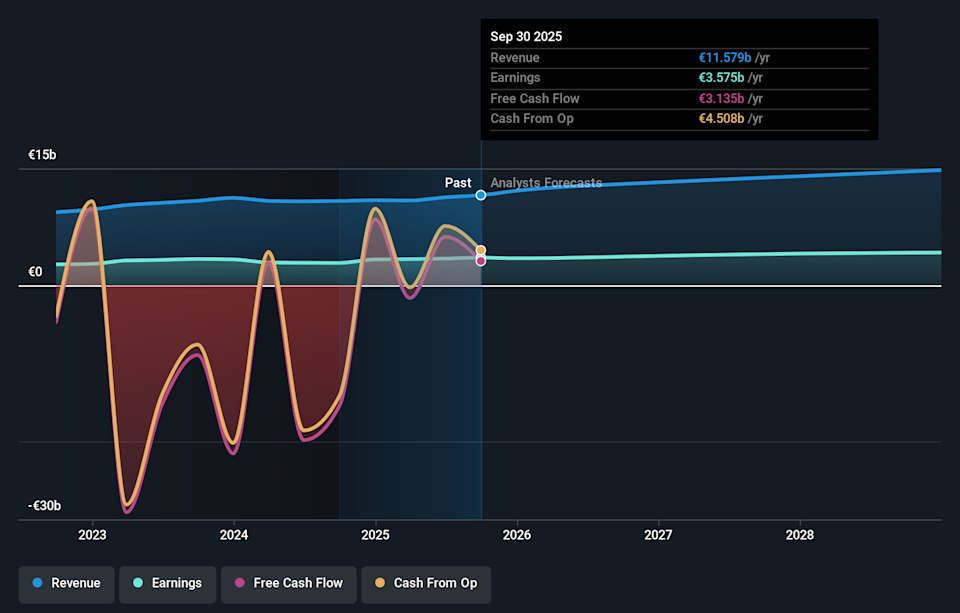

ENXTBR:KBC Earnings & Revenue Growth as at Feb 2026

3 things going right for KBC Group that this headline doesn’t cover.

The Business Lease deal and the earlier acquisition of 365.bank in Slovakia both push KBC deeper into Central Europe, where it already sees banking, insurance and leasing as core growth pillars. Folding Business Lease Czech Republic and Slovakia into ČSOB Leasing gives KBC more scale in vehicle and equipment leasing, which can support fee income and cross selling to existing clients. At the same time, a proposed total dividend of €5.1 per share for 2025 and an extraordinary collective bonus for employees indicate that management is comfortable returning a large share of 2025 net profit to shareholders while still funding expansion. For you, the key question is whether these acquisitions can be integrated efficiently enough to support returns relative to other European banks such as BNP Paribas, ING or Erste Group that are also active in the region.

-

The broader Central European expansion through Business Lease and 365.bank fits with the idea that KBC is relying on Central European operations and diversified revenue streams to support earnings.

-

Further investment in new businesses raises execution and cost discipline questions. This could challenge the view that digital transformation and efficiency gains on their own are enough to support margins.

-

The extraordinary employee bonus and specific leasing acquisitions are not explicitly covered in the narrative, so their effect on long term cost trends and income diversification may not be fully reflected there.