Valuation After Romania Approves 462 MW SMR Project")

Nuclearelectrica’s approval of a 462 MW small modular reactor project at Romania’s Doicesti site, using NuScale Power (SMR) technology, gives investors a fresh reference point for this early stage nuclear stock.

See our latest analysis for NuScale Power.

Despite the Romania decision and fresh U.S. Department of Energy support for small modular reactors, NuScale’s share price return has been weak recently, with a 30 day share price return of 27.84% and a 1 year total shareholder return of a 38% decline. However, the 3 year total shareholder return of 35.77% and 5 year total shareholder return of 23.47% show the longer term story has still rewarded patient holders.

If this SMR milestone has you looking wider across nuclear, you may want to see what else is on the radar with our 85 nuclear energy infrastructure stocks as a starting list of ideas.

So with NuScale trading at a discount to both analyst targets and some intrinsic value estimates, yet still years from commercial operations, are you looking at an underappreciated SMR pure play here, or is the market already baking in future growth?

Most Popular Narrative: 58% Undervalued

NuScale Power’s most followed narrative pegs fair value at about $33.96 per share, more than double the last close at $14.31. This sets up a wide valuation gap that rests heavily on future deployment and cash flow visibility.

With an NRC-approved SMR technology and the commitment of over $2 billion towards its development and licensing, NuScale is uniquely positioned for immediate commercial deployment compared to competitors focused solely on demonstration plans. This potentially accelerates revenue growth once commercial operations commence.

Curious what has to happen for that valuation to make sense? The narrative leans on rapid revenue expansion, rising margins, and a rich future earnings multiple. Want the full set of projections and timing assumptions that underpin that fair value? The details sit inside that narrative.

Result: Fair Value of $33.96 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, the narrative can easily crack if long term power purchase agreements keep slipping, or if funding and cash burn worries pick up again.

Find out about the key risks to this NuScale Power narrative.

Another View: Market Ratio Sends A Different Signal

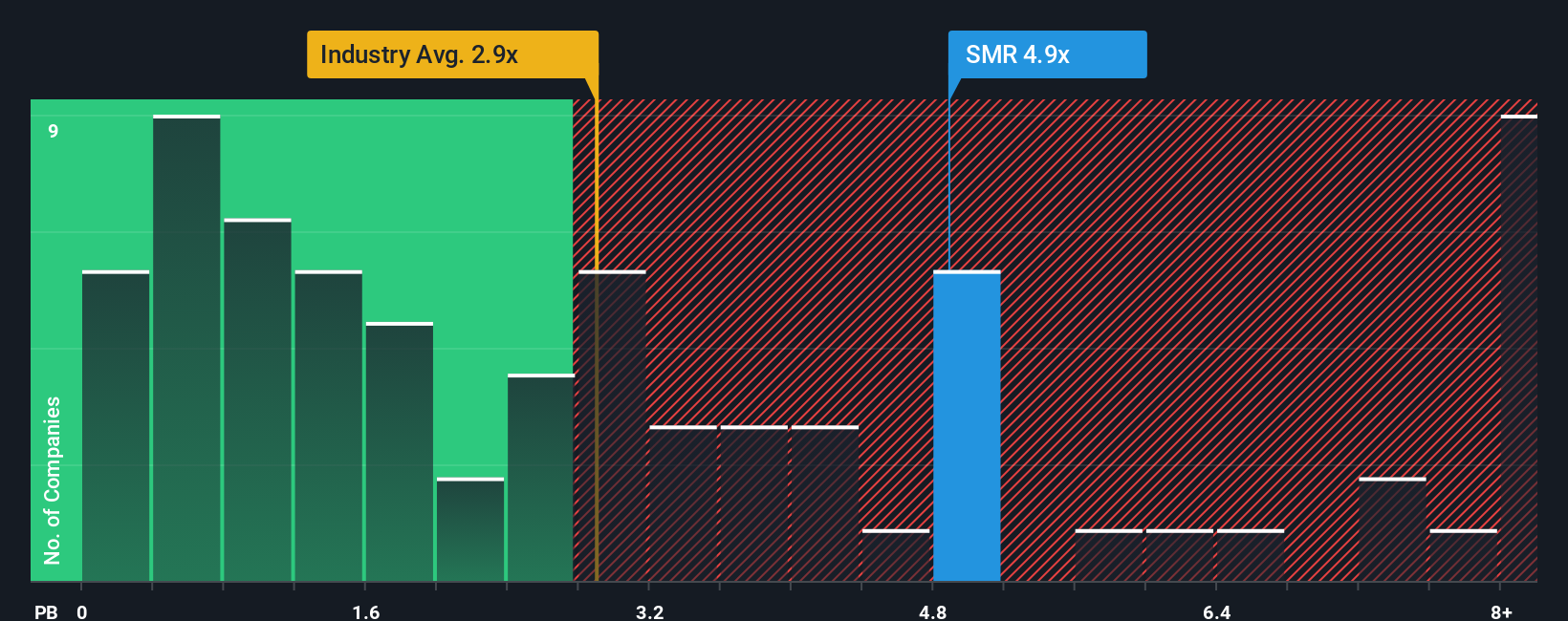

While our DCF model suggests NuScale is trading at a 63.5% discount to estimated fair value, the market ratio view is less forgiving. On a P/B of 4.9x, NuScale looks expensive versus the US Electrical industry at 2.9x, even if it screens cheaper than peers at 19.3x. So is this a rare opportunity or just a richer price tag for an early stage story?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:SMR P/B Ratio as at Feb 2026 Build Your Own NuScale Power Narrative

NYSE:SMR P/B Ratio as at Feb 2026 Build Your Own NuScale Power Narrative

If you see the numbers differently or want to stress test your own assumptions, the tools are available to build a custom view in minutes, so Do it your way and put your own stamp on the NuScale story.

A great starting point for your NuScale Power research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock story. Use the tools that surface other opportunities before they move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Discover if NuScale Power might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com