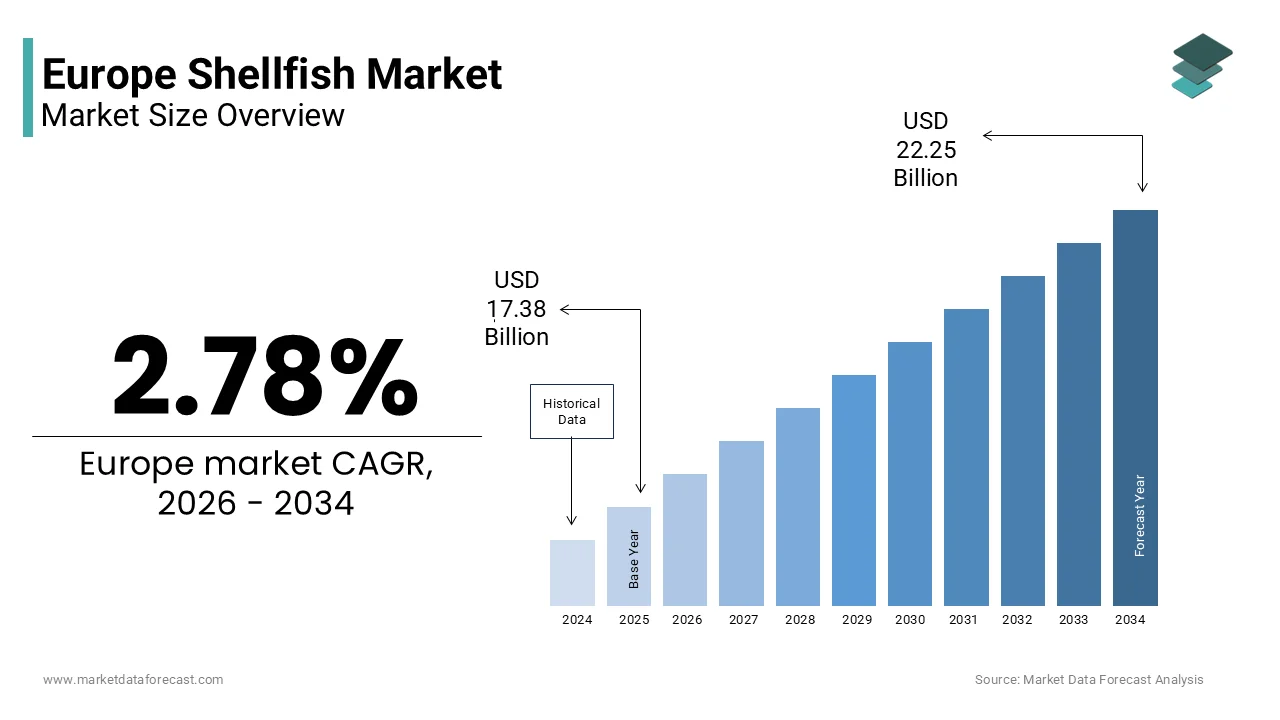

Europe Shellfish Market Size

The Europe shellfish market size was valued at USD 17.38 billion in 2025 and is projected to reach USD 22.25 billion by 2034 from USD 17.86 billion in 2026, growing at a CAGR of 2.78%.

Shellfish are a diverse range of crustaceans and mollusks including shrimp, crab, lobster, mussels, oysters, clams, and scallops and sourced from both wild fisheries and aquaculture systems across marine and coastal zones. This market is deeply embedded in regional culinary traditions, from French bouillabaisse and Spanish mariscada to Nordic shrimp salads and Italian seafood pastas. According to Eurostat, the European Union produced shellfish in 2023, with mollusks making up the majority of this volume, largely driven by mussel farming in Spain and the Netherlands. Wild-caught species such as Norway lobster and brown crab remain vital in the North Atlantic fisheries, particularly off the coasts of Ireland and Scotland. As per the European Commission’s Directorate-General for Maritime Affairs and Fisheries, the EU also imported shrimp in 2023, largely from aquaculture producers in Ecuador and Vietnam. This dual reliance on domestic aquaculture and global imports defines the structural complexity of Europe’s shellfish supply landscape.

MARKET DRIVERS Growing Consumer Preference for High Protein Low Fat Seafood

European consumers are increasingly prioritizing lean protein sources as part of health-conscious dietary patterns, which is positioning shellfish as a preferred alternative to red and processed meats and is propelling the European shellfish market. Shellfish such as shrimp and crab offer high-quality protein with minimal saturated fat and rich micronutrient profiles including selenium, zinc, and omega-3 fatty acids. According to the European Food Information Council, adults in Western Europe actively seek foods that support cardiovascular health, a trend that directly benefits shellfish consumption. National dietary guidelines in countries like Sweden and the Netherlands recommend weekly servings of seafood, with shellfish included as a key component. As per IRI Worldwide, chilled and ready-to-cook shellfish products grew in value across major EU markets in 2023, which is reflecting strong household demand. This nutritional alignment with public health messaging and evolving consumer wellness priorities continues to drive consistent demand across retail and foodservice channels.

Expansion of Premium Dining and Culinary Tourism

The rise of gastronomic tourism and premium restaurant experiences has significantly amplified demand for high-quality shellfish across Europe, which is further boosting the shellfish market expansion in Europe. Coastal regions such as Brittany, Galicia, and the Adriatic coast have built culinary identities around native shellfish, attracting visitors seeking authentic seafood experiences. According to the European Travel Commission, food-related travel motivations increased between 2022 and 2024, with seafood cited as a top attraction in Southern and Western Europe. Michelin-starred restaurants in cities like Copenhagen and San Sebastián routinely feature locally sourced oysters, scallops, and spider crabs, reinforcing shellfish as a symbol of luxury and terroir. This trend extends beyond fine dining, as seafood festivals in Portugal and Italy draw large numbers of attendees each year, stimulating local economies and normalizing shellfish consumption among broader demographics. The cultural valorization of shellfish as both heritage and indulgence sustains robust demand in experiential food contexts.

MARKET RESTRAINTS Stringent EU Regulations on Aquaculture Environmental Impact

The European shellfish market faces significant operational constraints due to rigorous environmental regulations governing aquaculture practices. The EU Water Framework Directive and Marine Strategy Framework Directive impose strict limits on nutrient discharge, habitat disruption, and chemical use in coastal farming zones. As per the European Environment Agency, many shellfish aquaculture sites in the Baltic and North Seas are located in protected Natura 2000 areas, requiring extensive permitting and monitoring. These requirements increase compliance costs and delay expansion approvals, particularly for new mussel and oyster farms. In France, regulatory reviews for shellfish farm renewals now take extended periods, slowing production scaling. Additionally, the EU’s Integrated Maritime Policy emphasizes ecosystem-based management, which may further restrict stocking densities and site selection. While environmentally necessary, these frameworks create administrative and financial barriers that limit supply growth and elevate production costs for European farmers.

Vulnerability to Harmful Algal Blooms and Marine Pollution

Shellfish production in Europe is acutely susceptible to episodic closures caused by harmful algal blooms and marine contamination events, which is further hampering the shellfish market growth in Europe. Filter-feeding species like mussels and oysters accumulate biotoxins during algal blooms, rendering them unsafe for human consumption. According to the European Marine Observation and Data Network, shellfish harvesting zones across the EU experienced temporary closures in 2023 due to phycotoxin levels exceeding safety thresholds. The Irish Sea and Bay of Biscay are particularly prone, with bloom frequency increasing since 2015 due to warming sea temperatures and eutrophication. These closures result in direct revenue losses, supply chain disruptions, and reputational damage. Producers must invest in real-time monitoring systems and emergency harvesting protocols, adding operational complexity. Climate change projections suggest such events will intensify, posing a persistent biological risk to the stability of European shellfish supply.

MARKET OPPORTUNITIES Advancement of Integrated Multi Trophic Aquaculture Systems

Integrated multi trophic aquaculture (IMTA) presents a transformative opportunity for the European shellfish market. IMTA systems combine fed species like fish with extractive species such as mussels and seaweed, where shellfish act as natural biofilters by absorbing excess nutrients. According to the Norwegian Institute of Marine Research, pilot IMTA farms in the Skagerrak demonstrated reductions in nitrogen discharge while producing marketable mussels. As per the European Commission’s Horizon Europe program, significant funding has been allocated since 2022 to support IMTA commercialization, recognizing its potential to align aquaculture with circular economy principles. Countries like Denmark and Spain are scaling IMTA models along their coasts, creating dual revenue streams and improving environmental licensing prospects. This innovation enhances ecological performance and appeals to eco-conscious consumers and retailers seeking certified sustainable seafood, opening premium market access and long-term resilience.

Rising Demand for Convenience and Value-Added Shellfish Products

The shift toward convenience-oriented food consumption in urban Europe is creating strong demand for pre-cleaned, cooked, and ready-to-eat shellfish formats, which is another prominent opportunity in the European shellfish market. Busy lifestyles and limited culinary skills among younger demographics have driven growth in chilled peeled shrimp, marinated mussels, and vacuum-packed crab meat. According to NielsenIQ, sales of prepared shellfish in Western Europe grew in 2023, outpacing whole raw categories. Retailers such as Carrefour and Tesco have expanded their seafood counters with chef-inspired shellfish bowls and tapas-style packs, capitalizing on this trend. Foodservice operators are also adopting portion-controlled shellfish for fast casual concepts and meal kits. This value-added segment commands higher margins and reduces post-harvest waste, incentivizing processors to invest in automation and cold chain logistics. By meeting modern consumption habits, the industry can expand beyond traditional users and integrate shellfish into everyday meals.

MARKET CHALLENGES Labor Shortages in Post Harvest Processing

The European shellfish market faces acute labor shortages in manual processing tasks such as shelling, grading, and packaging, particularly in rural coastal communities. Shellfish like crab and lobster require skilled hand processing to maintain quality, yet aging workforces and declining interest in seasonal seafood jobs have created critical gaps. According to the European Social Survey, employment in fisheries-related processing declined between 2018 and 2023, with fewer younger workers entering the sector. Brexit further exacerbated this in the UK, where restrictions on seasonal migrant labor reduced available workers in Scottish shellfish plants. Automation remains limited due to the delicate nature of shellfish, making labor dependency a persistent bottleneck. Without sufficient workforce investment or technological breakthroughs, processing capacity constraints will continue to limit value addition and export potential across the region.

Geopolitical Disruptions in Global Supply Chains

Europe’s reliance on imported shellfish, particularly warm-water shrimp from Latin America and Asia, exposes the market to geopolitical and logistical volatility, which is further challenging the growth of the European shellfish market. Trade policy shifts, port congestion, and diplomatic tensions can abruptly disrupt supply flows. As per the European Market Observatory for Fisheries and Aquaculture Products, the European Commission temporarily halted imports of certain Ecuadorian shrimp in 2023 due to antibiotic residue concerns, which impacted wholesale prices across major markets. Similarly, the Red Sea shipping crisis in early 2024 extended transit times, increasing spoilage risks for perishable shellfish. These disruptions force buyers to seek alternative sources at higher costs or reduce offerings, undermining menu and product stability. Diversifying sourcing and building strategic cold storage reserves are essential yet costly adaptations, which is indicating the fragility of Europe’s integrated global shellfish supply network.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

2.78%

Segments Covered

By Type, Application, and Region

Various Analyses Covered

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

Austevoll Seafood ASA, Bolton Group SRL, Grieg Seafood ASA, Mowi ASA, Thai Union Group PCL, Nordic Seafood A S, Roem van Yerseke B V, Delta Mossel B V, Lenger Seafoods Group, Sykes Seafood Ltd, Royal Greenland A S, and Nomad Foods Ltd

SEGMENTAL ANALYSIS By Type Insights

The shrimps segment led the market by holding 41.5% of the European market share in 2025. The dominance of shrimps segment in the European market is driven by their culinary versatility, widespread consumer acceptance, and consistent supply from both aquaculture imports and limited domestic fisheries. Unlike regionally specific shellfish such as oysters or crabs, shrimps are universally integrated into European diets, which is making them a staple across diverse cultures. According to the European Market Observatory for Fisheries and Aquaculture Products, the EU imported shrimp in 2023, with Ecuador, Vietnam, and India supplying the majority of this volume. The chilled and frozen retail formats of peeled and cooked shrimp have further accelerated household adoption, particularly in urban centers where convenience is paramount. Additionally, foodservice operators favor shrimps for their consistent sizing, rapid cooking time, and high yield, enabling efficient menu execution in both fast casual and fine dining establishments. This combination of accessibility, adaptability, and reliable global supply secures shrimps’ position as the cornerstone of European shellfish consumption.

The oysters segment is the fastest-growing segment in the Europe shellfish market and is predicted to witness a CAGR of 7.5% over the forecast period owing to their repositioning from a luxury delicacy to a symbol of sustainable aquaculture and coastal identity. According to FranceAgriMer, France produces the majority of the EU’s Pacific cupped oysters. The revival of native flat oyster farming in the Netherlands and Ireland has added premium heritage appeal. Urban consumers in cities like Berlin and Barcelona increasingly seek “oyster bar” experiences that emphasize traceability, terroir, and minimal processing, aligning with clean label values. Furthermore, scientific recognition of oysters’ ecosystem services such as water filtration and habitat creation has enhanced their environmental credibility. Retailers like E.Leclerc and Waitrose now feature live oysters with QR codes detailing farm origin and harvest date, bridging transparency with indulgence. These cultural, ecological, and commercial convergences propel oysters beyond niche markets into mainstream premium seafood demand.

By Application Insights

The supermarket channel dominated the Europe shellfish market by capturing 56.9% of the European market share in 2025. The growth of the supermarket channel segment in this regional market is driven by the expansion of chilled seafood sections, private label innovation, and the growing consumer preference for home meal preparation. Major retailers across Germany, France, and the UK have invested heavily in temperature-controlled logistics and in-store seafood counters staffed by trained fishmongers, enhancing freshness perception and purchase confidence. According to IRI Worldwide, supermarket sales of prepared shellfish grew in value across Western Europe in 2023. The rise of “premium everyday” positioning has broadened their appeal beyond festive occasions. Private label offerings now include marinated scallops, ready-to-grill packs, and sustainably certified crab cakes, catering to convenience without compromising quality. Additionally, supermarkets leverage loyalty data to tailor promotions during peak consumption periods such as Christmas and summer holidays, reinforcing habitual purchasing. This infrastructure, scale, and consumer trust solidify supermarkets as the primary gateway for shellfish in European households.

The restaurant segment is the fastest-growing application channel in the Europe shellfish market and is expected to record a CAGR of 8.18% over the forecast period. The proliferation of seafood-focused casual dining concepts and the integration of shellfish into globally inspired menus are propelling the growth of the restaurant segment in the European market. Coastal tourism plays a pivotal role; as per the World Tourism Organization, Spain welcomed millions of international tourists in 2023, many of whom dined on fresh local shellfish in seaside taverns. Inland cities are also embracing shellfish through fusion cuisine—such as Nordic shrimp bao buns in Copenhagen or Sicilian red prawn pasta in Milan. Michelin guide data shows an increase in restaurants featuring shellfish as a signature ingredient between 2022 and 2024. Moreover, chefs increasingly highlight traceability and seasonality, partnering directly with local fishermen to offer daily catch specials that resonate with conscious diners. The experiential value of consuming freshly prepared shellfish in a social setting—enhanced by visual presentation and storytelling—creates emotional engagement that retail cannot replicate, driving sustained growth in this high-margin channel.

REGIONAL ANALYSIS France Shellfish Market Analysis

France had the leading position in the European shellfish market in 2025 by capturing 23.8% of the regional market share. The dominating spot of France in the European market is attributed to its dual role as a leading producer and a culinary standard bearer. The country is the EU’s top oyster producer and a major harvester of mussels, scallops, and spider crabs. Its coastal regions—particularly Brittany, Normandy, and the Mediterranean coast—operate sophisticated aquaculture systems that blend tradition with innovation. French consumers exhibit deep cultural affinity for shellfish, with many reporting annual consumption during holiday seasons. The government actively supports the sector through initiatives such as the France Relance plan, which allocated funding in 2023 to modernize shellfish hatcheries and combat marine biosecurity threats. Additionally, France’s culinary standards shape shellfish preparation techniques across Europe, reinforcing demand for high-quality products. This synergy of production heritage, policy support, and gastronomic prestige cements France’s unrivaled position in the regional market.

Spain Shellfish Market Analysis

Spain commanded for the second-largest market share in the European market in 2025. It is the EU’s foremost producer of mussels through raft culture in Galicia’s Rías Baixas. The country also leads in wild capture of red shrimp and Norway lobster along the Mediterranean slope. Domestically, shellfish are central to tapas culture and festive gatherings, ensuring consistent household demand. Internationally, Spain functions as a key redistribution hub, exporting processed mussel meat and frozen prawns to Germany, Italy, and France. The Spanish government’s Strategic Plan for Aquaculture 2021–2027 prioritizes sustainability certifications and digital traceability, aligning with EU Green Deal objectives. Furthermore, Spain’s tourism influx fuels direct consumption in coastal restaurants, creating a resilient dual demand stream that anchors its market leadership.

United Kingdom Shellfish Market Analysis

The United Kingdom is expected to showcase a promising CAGR in the European market during the forecast period owing to the strong per capita consumption despite limited domestic production capacity. British consumers favor brown crab, langoustines, and cold-water shrimp, with household expenditure on shellfish reaching significant levels. The UK imports most of its shellfish needs, primarily from Norway, Iceland, and Morocco, reflecting post-Brexit trade realignments. Cities such as London, Edinburgh, and Bristol host vibrant seafood scenes where premium shellfish feature prominently in modern British cuisine. The Marine Stewardship Council reports that a majority of UK shellfish sold in major retailers carries eco-certification, indicating high consumer sensitivity to sustainability. Despite labor shortages in processing, innovation in ready-to-eat formats has maintained market vitality. The UK’s affluent urban demographics and culinary openness sustain its status as a high-value destination within the European shellfish landscape.

Italy Shellfish Market Analysis

Italy is predicted to hold a notable share of the European shellfish market over the forecast period. The regional diversity and emphasis on native species are driving the Italian market growth. The Adriatic coast supplies clams and mussels, while Sicily and Sardinia are renowned for red prawns and scampi. Annual shellfish landings are supported by artisanal small-scale fisheries that play a crucial socioeconomic role. Italian cuisine integrates shellfish into iconic dishes such as spaghetti alle vongole and risotto ai frutti di mare, ensuring intergenerational consumption continuity. The Slow Food movement has amplified interest in protected designations, indirectly boosting shellfish appreciation. Retailers promote locally sourced shellfish with short supply chains, resonating with the “km zero” ethos. Additionally, Italy’s aging fishing fleet is undergoing EU-funded modernization, improving catch quality and reducing waste. This fusion of tradition, locality, and culinary pride positions Italy as a guardian of Mediterranean shellfish heritage.

Netherlands Shellfish Market Analysis

The Netherlands is projected to register a healthy CAGR in the European shellfish market over the forecast period. While domestic production focuses on mussels from the Wadden Sea and Zeeland delta, the country’s true strength lies in its distribution infrastructure. The Port of Rotterdam handles a significant portion of shellfish imports entering the EU. Dutch processors specialize in value-added formats including IQF peeled shrimp and ready-to-steam mussel pouches distributed across Northern and Central Europe. The nation is also pioneering offshore mussel cultivation in the North Sea, supported by Wageningen University research demonstrating carbon sequestration potential. Retailers such as Albert Heijn prioritize MSC-certified shellfish, influencing supplier practices across the supply chain. This combination of logistical prowess, technological adoption, and sustainability leadership enables the Netherlands to exert disproportionate influence far beyond its production volume.

COMPETITIVE LANDSCAPE

The Europe shellfish market features a multi-tiered competitive landscape comprising large integrated multinationals regional cooperatives and specialized artisanal producers. Global players like Royal Greenland and Pescanova dominate volume through scale logistics and brand recognition while local fishermen collectives in France Italy and Spain maintain strong footholds in premium fresh segments through direct sales and terroir-based storytelling. Competition is increasingly defined by sustainability credentials traceability and product differentiation rather than price alone. The entry barriers are high due to strict EU hygiene regulations vessel licensing quotas and cold chain requirements yet niche opportunities exist in organic certification native species revival and experiential retail. Innovation in packaging automation and alternative feed for farmed species further intensifies rivalry. As consumer expectations rise around ethics freshness and convenience companies must continuously adapt to retain relevance across fragmented yet discerning European markets.

KEY MARKET PLAYERS

Some of the notable key players in the Europe shellfish market are

- Austevoll Seafood ASA

- Bolton Group SRL

- Grieg Seafood ASA

- Mowi ASA

- Thai Union Group PCL

- Nordic Seafood A/S

- Roem van Yerseke B.V.

- Delta Mossel B.V.

- Lenger Seafoods Group

- Sykes Seafood Ltd

- Royal Greenland AS

- Nomad Foods Ltd

Top Players in the Market

- Royal Greenland is a leading seafood company headquartered in Denmark with extensive operations across the North Atlantic. It plays a pivotal role in the Europe shellfish market through its vertically integrated supply chain that sources cold water shrimp and snow crab from sustainable fisheries in Greenland Iceland and Canada. The company supplies both raw and value-added shellfish products to retailers, foodservice operators and industrial customers throughout Europe. To strengthen its position Royal Greenland recently upgraded its processing facility in Nuuk to enhance traceability and reduce energy consumption aligning with EU sustainability standards. It also launched a blockchain enabled provenance platform allowing European buyers to verify catch location and handling practices in real time reinforcing trust in premium Arctic shellfish.

- Pescanova is a Spanish multinational with deep roots in aquaculture and wild catch fisheries specializing in prawns, mussels and clams. The company operates one of Europe’s largest integrated shellfish networks spanning hatcheries sea farms and processing plants primarily in Spain Portugal and Latin America. Pescanova supplies fresh frozen and ready to cook shellfish to major European supermarket chains and restaurant groups. In recent years it has invested heavily in recirculating aquaculture systems to produce whiteleg shrimp inland reducing pressure on coastal ecosystems. The company also partnered with the University of Santiago de Compostela to develop disease resistant mussel strains enhancing yield stability and biosecurity across its European operations.

- Mowi is a Norwegian based global seafood leader that has strategically expanded into shellfish through diversified marine protein offerings. While primarily known for salmon Mowi has developed a growing portfolio of cold-water shellfish including northern shrimp and scallops sourced from certified fisheries in Norway and Scotland. The company leverages its advanced logistics infrastructure to deliver chilled shellfish across Western and Northern Europe within 48 hours of harvest. Mowi recently integrated shellfish into its digital sales platform enabling chefs and retailers to access real time inventory and sustainability documentation. This move strengthens its value proposition as a one stop supplier of premium responsibly sourced seafood aligned with evolving European procurement policies.

Top Strategies Used by the Key Market Participants

Key players in the Europe shellfish market focus on vertical integration to control quality from ocean to plate ensuring freshness and compliance with stringent EU food safety norms. They prioritize sustainability certifications such as MSC and ASC to meet retailer and consumer demands for responsible sourcing. Investment in value added processing including ready to eat and portion controlled formats addresses urban convenience trends. Companies are adopting digital traceability tools like blockchain and IoT sensors to provide end to end transparency on origin handling and environmental impact. Strategic partnerships with research institutions support innovation in disease resistant stocks low impact aquaculture and offshore farming. Additionally, they expand cold chain logistics and regional distribution hubs to reduce delivery times and minimize waste across diverse European geographies.

MARKET SEGMENTATION

This research report on the European shellfish market has been segmented and sub-segmented based on categories.

By Type

- Crabs

- Prawns

- Shrimps

- Oysters

- Others

By Application

- Restaurant

- Supermarket

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe