Get insights on thousands of stocks from the global community of over 7 million individual investors at Simply Wall St.

-

If you are wondering whether National Energy Services Reunited is still reasonably priced after its recent run, this article will walk through what the current share price might be implying about future expectations.

-

The stock last closed at US$24.17, with returns of 17.3% over 7 days, 33.0% over 30 days, 53.1% year to date and 155.8% over 1 year. These figures naturally raise questions about how much optimism is already in the price.

-

Recent coverage of National Energy Services Reunited has focused on its role in the energy services space and how investor interest has shifted toward companies exposed to that sector. This backdrop helps explain why some traders are reassessing both the potential opportunity and the risks attached to the shares.

-

Right now, the company scores 2 out of 6 on our valuation checks. We will walk through what different methods such as discounted cash flow, multiples and asset based views each suggest, and then finish with a framework that can help you interpret all these signals in a more complete way.

National Energy Services Reunited scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

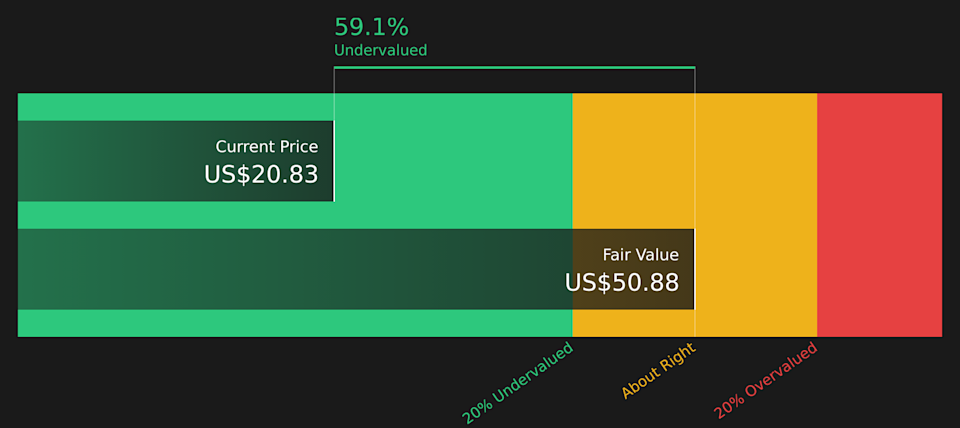

A Discounted Cash Flow, or DCF, model takes the cash that a business is expected to generate in the future and discounts it back to what that stream might be worth in today’s dollars.

For National Energy Services Reunited, the model used is a 2 Stage Free Cash Flow to Equity approach, based on its recent free cash flow of about $153.0 million. Analysts provide free cash flow estimates for several years, and Simply Wall St then extends those projections further. Under this framework, projected free cash flow in 2035 is about $273.2 million, with interim years ranging from $170.8 million in 2026 to $264.5 million in 2034, all in US$ terms.

After discounting those future cash flows back to today, the model arrives at an estimated intrinsic value of about $51.14 per share. Compared with the recent share price of $24.17, this implies the stock is 52.7% undervalued on this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests National Energy Services Reunited is undervalued by 52.7%. Track this in your watchlist or portfolio, or discover 56 more high quality undervalued stocks.

NESR Discounted Cash Flow as at Feb 2026

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for National Energy Services Reunited.

For a profitable company, the P/E ratio is a useful snapshot of how much investors are paying for each dollar of earnings. It helps you quickly compare what the market is willing to pay for National Energy Services Reunited’s earnings against other options.

What counts as a “normal” P/E depends a lot on how the market views a company’s growth potential and risk. Higher expected growth or lower perceived risk can justify a higher P/E, while slower growth or higher risk tends to align with a lower P/E.

National Energy Services Reunited currently trades on a P/E of about 47.6x. That sits above the Energy Services industry average of around 25.3x and also above the peer group average of roughly 9.6x. Simply Wall St’s Fair Ratio, which estimates an appropriate P/E after factoring in elements like earnings growth, profit margins, industry, market cap and risk, comes in at about 29.3x. This tailored Fair Ratio is more specific than a simple comparison with industry or peers because it adjusts for the company’s own characteristics rather than assuming all businesses are alike.

Comparing the current 47.6x P/E to the 29.3x Fair Ratio points to the shares trading above that Fair Ratio estimate.

Result: OVERVALUED

NasdaqCM:NESR P/E Ratio as at Feb 2026

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 23 top founder-led companies.

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which let you attach a clear story to your numbers by linking your view of National Energy Services Reunited’s future revenues, earnings and margins to a forecast and then to a Fair Value that you can compare directly with today’s price.

On Simply Wall St’s Community page, Narratives are presented as an easy tool that many investors already use. This means you can review different cases side by side, see how a Fair Value of about US$10, US$22.14 or US$30 lines up against the current share price, and quickly frame whether that particular story points you toward being more cautious or more optimistic.

Because these Narratives refresh when new information such as news, contract updates or earnings is added to the platform, you are not locked into a static view. You can see how the story and the implied Fair Value for National Energy Services Reunited evolve over time as conditions change.

For National Energy Services Reunited however we will make it really easy for you with previews of two leading National Energy Services Reunited Narratives:

🐂 National Energy Services Reunited Bull Case

Fair Value: US$30.00

Implied pricing gap vs last close: 19.4% above this Fair Value, based on the current share price of US$24.17

Revenue growth used in this narrative: 19.65%

-

Analysts who take this view see National Energy Services Reunited’s hydraulic fracturing scale in Saudi Arabia and its heavy exposure to Middle East upstream spending as key supports for long cycle cash flows.

-

The narrative leans on contract visibility, extended durations and regional technology platforms to frame a path to higher margins and earnings by 2028, all discounted at 7.34% and tied to a Fair Value of US$30 per share.

-

Risks under this view focus on oilfield reliance, geographic concentration in MENA and the capital intensity needed to support growth while energy transition and decarbonization pressures evolve.

🐻 National Energy Services Reunited Bear Case

Fair Value: US$22.14

Implied pricing gap vs last close: 9.2% above this Fair Value, based on the current share price of US$24.17

Revenue growth used in this narrative: 18.93%

-

This narrative centres on the idea that while National Energy Services Reunited benefits from long term contracts and Jafurah exposure, reliance on MENA oil contracts and high capital needs could limit how much value the current share price reflects.

-

Analysts in this camp anchor on a Fair Value of about US$22.14, using earnings assumptions that reach US$168.6 million by 2028, a future P/E of about 10.37x and a discount rate of 7.35%.

-

The key watchpoints here are contract timing, concentration in a single region, decarbonization trends and working capital demands, all of which could affect how reliable those projected cash flows turn out to be.

If you want to see how these stories are built line by line from assumptions on revenue, margins and P/E through to Fair Value, you can read them in full and compare them directly on the Community page, starting with Curious how numbers become stories that shape markets? Explore Community Narratives.

Do you think there’s more to the story for National Energy Services Reunited? Head over to our Community to see what others are saying!

NasdaqCM:NESR 1-Year Stock Price Chart

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NESR.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

After 1 Year 155% Rally?")