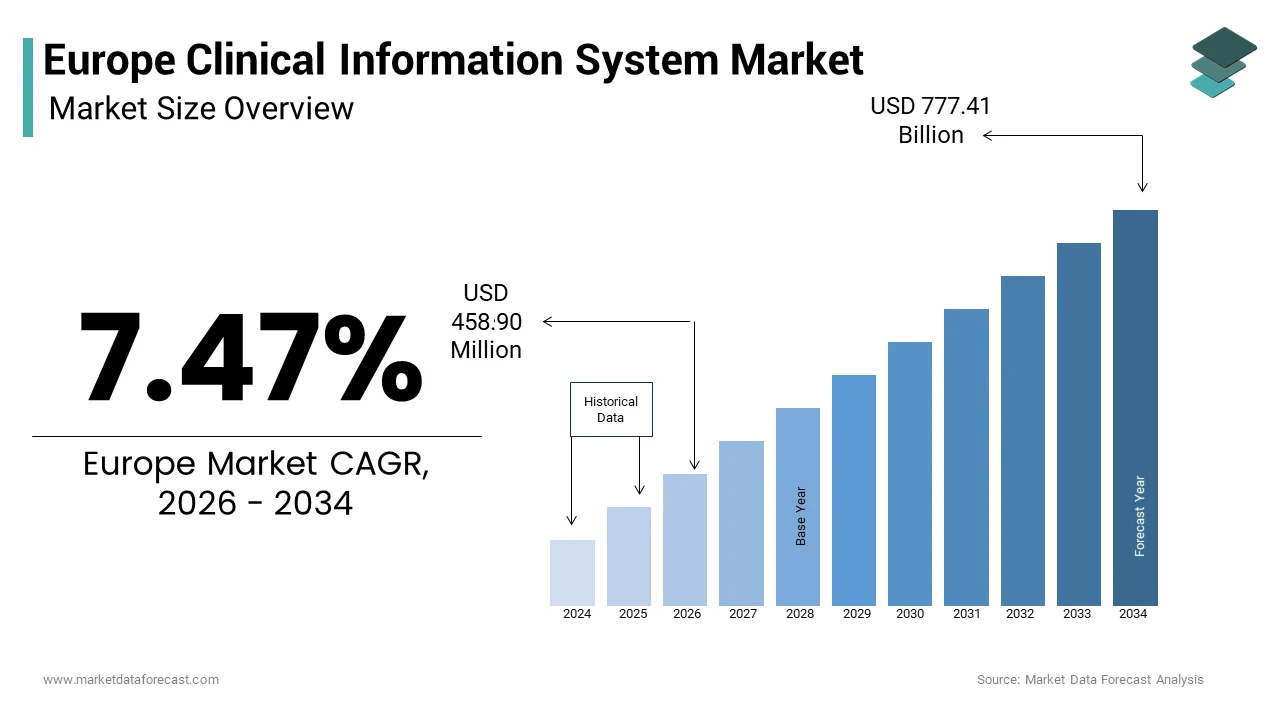

Europe Clinical Information System Market Size

The Europe clinical information system market size was valued at USD 426.94 million in 2025 and is anticipated to reach USD 458.90 million in 2026 to reach USD 777.41 million by 2034, growing at a CAGR of 7.475 during the forecast period from 2026 to 2034.

Clinical information system comprises integrated digital platforms designed to manage, store, and exchange patient health data across care settings, including electronic health records (EHR), computerized physician order entry (CPOE), clinical decision support systems (CDSS), and nursing documentation tools. These systems are foundational to modern healthcare delivery, enabling coordinated, evidence based, and efficient patient care. The market is being propelled by a confluence of demographic, regulatory, and technological imperatives. According to Eurostat, the share of the EU population aged 65 and over has been steadily increasing, which significantly raises the demand for chronic disease management and seamless care coordination. As per the European Commission, workforce shortages are expected to create a substantial deficit of healthcare professionals in the EU, necessitating technology that enhances productivity and reduces administrative burden. Furthermore, the EU’s cross border health data exchange framework, operational under the European Health Data Space, mandates interoperability standards that compel healthcare providers to upgrade legacy systems, thereby accelerating the adoption of modern clinical information infrastructure across the continent.

MARKET DRIVERS Mandatory Interoperability Requirements Under the European Health Data Space

The European Union’s binding legislative framework for health data interoperability, spearheaded by the European Health Data Space regulation is one of the major factors driving the growth of the Europe clinical information system market. This landmark policy mandates that all member states ensure their healthcare providers can securely exchange structured electronic health records across borders by 2027. As per the European Commission, this requires the adoption of standardized data formats such as HL7 FHIR and the implementation of national electronic health record exchange infrastructures. The directive effectively compels hospitals and clinics to replace or significantly upgrade outdated, siloed systems that cannot communicate with external networks. According to the European Centre for Disease Prevention and Control, many EU hospitals still lack fully interoperable EHR systems capable of cross border data sharing, highlighting the vast scale of required investment. This regulatory push aims to enable large scale health research, improve public health surveillance, and empower patients with control over their own data. The legal obligation creates a non-discretionary demand for compliant clinical information systems, making it the single most powerful catalyst for market growth across the region.

Severe Healthcare Workforce Shortages Demanding Workflow Automation

The acute and worsening shortage of clinical staff across Europe that is forcing healthcare institutions to adopt clinical information systems as a critical tool for enhancing workforce productivity and mitigating burnout is further boosting the expansion of the Europe clinical information system market. According to the State of Health in the EU 2024 report, the bloc faces a projected shortfall of nearly 1 million doctors, nurses, and allied health professionals by 2025, driven by an aging workforce and insufficient training capacity. In this context, manual documentation and fragmented communication are no longer sustainable. Clinical information systems directly address this crisis by automating routine tasks such as medication reconciliation, order entry, and discharge summaries. As per the European Observatory on Health Systems and Policies, hospitals with advanced CPOE and CDSS have demonstrated reductions in physician time spent on administrative duties, while integrated nursing documentation modules cut charting time significantly. By streamlining workflows and reducing cognitive load, these systems allow existing staff to focus more on direct patient care, making them an essential operational necessity rather than a discretionary IT investment.

MARKET RESTRAINTS Fragmented Legacy Infrastructure and High Integration Costs

A significant restraint on the Europe clinical information system market is the pervasive presence of heterogeneous, decades old legacy systems that are technically incompatible and prohibitively expensive to integrate or replace. Many European hospitals, particularly in Southern and Eastern Europe, operate on a patchwork of department specific software from multiple vendors, creating data silos that impede holistic patient care. According to the European Hospital and Healthcare Federation, a majority of hospitals reported that integrating new clinical modules with their existing infrastructure was their top technical challenge. The cost of a full EHR replacement can be extremely high for large academic medical centers, a sum that is difficult to justify amid constrained public health budgets. Moreover, the lack of standardized interfaces means that even when new systems are procured, extensive custom middleware development is required, adding years to implementation timelines and increasing total cost of ownership. This technological debt traps institutions in suboptimal workflows, stifling innovation and delaying the realization of a truly connected health ecosystem across the continent.

Stringent Data Privacy Regulations Limiting Cloud Adoption

The Europe clinical information system market is constrained by the rigorous data protection requirements of the General Data Protection Regulation, which create significant barriers to the adoption of cloud-based solutions. While cloud platforms offer scalability, cost efficiency, and rapid deployment, GDPR’s strict rules on data residency, processing transparency, and patient consent make many healthcare providers hesitant to migrate sensitive clinical data off premise. According to the European Data Protection Board, any health data processed in the cloud must remain within the EU unless equivalent safeguards are guaranteed, limiting the choice of hyperscalers. In countries like Germany and France, national interpretations of GDPR have led to additional certification requirements for cloud service providers, further complicating procurement. As per the Centre for Digital Health in Berlin, only a minority of hospitals in Germany used cloud hosted EHR components, citing compliance risk as the primary concern. This regulatory caution slows the transition to modern, agile architectures and forces providers to maintain costly on-site data centers, ultimately hindering the market’s ability to leverage the full potential of scalable digital health infrastructure.

MARKET OPPORTUNITIES Expansion of AI Powered Clinical Decision Support for Chronic Disease Management

The integration of artificial intelligence into clinical decision support systems to manage the growing burden of chronic diseases is a prominent opportunity in the Europe clinical information system market. As per the European Society of Cardiology, millions of Europeans live with diabetes and cardiovascular conditions, creating urgent demand for scalable tools that can assist clinicians in complex treatment planning. Modern clinical information systems are embedding AI algorithms that analyze longitudinal patient data to predict disease progression, recommend personalized therapies, and flag early signs of deterioration. According to validation studies conducted across Nordic hospitals, AI models integrated into EHRs have demonstrated strong predictive capabilities for conditions such as diabetic ketoacidosis. These intelligent systems not only improve clinical outcomes but also reduce hospital readmissions, a key cost driver in publicly funded systems. As the European Health Data Space facilitates access to larger, high-quality datasets, the performance of these AI tools will continue to improve, creating a powerful value proposition for healthcare providers seeking to deliver proactive, precision care in an era of resource scarcity.

Development of National Federated Health Data Infrastructures for Real World Evidence Generation

The EU’s strategic push to establish national federated health data infrastructures that enable large scale research without centralizing raw patient data is another promising opportunity in the Europe clinical information system market. The European Health Data Space envisions a network where clinical information systems act as secure nodes, allowing researchers to query distributed databases while preserving privacy. This model creates immense demand for clinical platforms that can support standardized data extraction, anonymization, and secure API access. According to the Innovative Medicines Initiative, numerous European countries are building such infrastructures, with projects like France’s Health Data Hub and Germany’s Medical Informatics Initiative already connecting hospitals nationwide. Clinical information system vendors that can certify their products for these frameworks will gain a decisive competitive advantage. This shift transforms EHRs from operational tools into engines of scientific discovery, enabling faster drug development, post market surveillance, and health technology assessment. The convergence of clinical care and research infrastructure represents a paradigm shift that will redefine the value and scope of clinical information systems in Europe.

MARKET CHALLENGES Persistent Clinician Resistance Due to Poor User Experience and Workflow Disruption

A primary challenge confronting the Europe clinical information system market is sustained resistance from frontline clinicians, who often perceive these systems as cumbersome, time consuming, and disruptive to patient interaction. Despite technological advances, many EHR interfaces remain cluttered, requiring excessive clicks and free text entry that detract from consultation time. As per the European Federation of Public Service Unions, a majority of physicians believe their current clinical system negatively impacts their work life balance, with many reporting symptoms of digital burnout. This dissatisfaction leads to workarounds, incomplete documentation, and even outright rejection of new modules, undermining digitization goals. The problem is exacerbated by inadequate training and a lack of clinician involvement in system design. According to The Lancet Digital Health, hospitals co designing EHR workflows with end users have shown significantly higher adoption rates. Until vendors prioritize human centered design and seamless integration into natural clinical routines, this cultural and ergonomic barrier will continue to limit the effectiveness and return on investment of even the most advanced systems.

Inadequate Cybersecurity Preparedness in Public Healthcare Institutions

The Europe clinical information system market faces a critical challenge in the form of widespread cybersecurity vulnerabilities within public healthcare institutions, which are increasingly targeted by ransomware attacks. Clinical systems house the most sensitive personal data, making them prime targets, yet many hospitals operate with outdated software, unpatched systems, and limited IT security staff. According to the European Union Agency for Cybersecurity, the healthcare sector has experienced a sharp increase in ransomware incidents, with several high profile attacks forcing hospitals to revert to paper records. As per the Centre for Strategic and International Studies, the financial and operational impact of healthcare data breaches in Europe has been severe, costing millions of euros annually. This threat environment creates a paradox, as digitization is essential for modern care but also expands the attack surface. Without significant investment in cyber resilience, often competing with clinical priorities, the trust and continuity of digital health services remain at serious risk, potentially derailing broader adoption efforts across the region.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

7.47%

Segments Covered

By Deployment, Component, Application, End-User, By Country

Various Analyses Covered

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe

Market Leaders Profiled

Cerner Corporation (An Oracle Company), Epic Systems Corporation, Allscripts Healthcare Solutions, Inc., GE HealthCare, Philips Healthcare, McKesson Corporation, Siemens Healthineers, eClinicalWorks, Meditech, IBM Watson Health

SEGMENTAL ANALYSIS By Deployment Insights

The on-premises deployment model segment led the market by holding 61.6% of the European market share in 2025. The dominance of on-premise segment in the European market is majorly driven by longstanding data sovereignty concerns and stringent interpretations of the General Data Protection Regulation in key markets like Germany and France. Many public hospitals and university medical centers, which form the backbone of European healthcare, have historically invested heavily in on-site data centers to maintain direct control over sensitive patient records. As per the European Hospital and Healthcare Federation, a majority of tertiary care hospitals in the EU still operate their core electronic health record systems on premises due to perceived security and compliance advantages. Additionally, legacy contracts with established vendors like Siemens Healthineers and Dedalus often include long term maintenance agreements that disincentivize migration. The high initial capital expenditure is offset by predictable operational costs and the ability to customize systems without reliance on third party cloud providers, making on-premises solutions the default choice for risk-averse institutions managing complex, high-volume clinical workflows.

The cloud-based deployment segment is anticipated to exhibit a CAGR of 19.1% over the forecast period owing to the urgent need for scalable, cost efficient, and interoperable health IT infrastructure to support the European Health Data Space. Cloud platforms offer rapid deployment, automatic updates, and seamless integration with national health data exchange networks, addressing critical gaps in legacy systems. As per the Centre for Digital Health in Berlin, cloud based EHR implementations have demonstrated faster go-live times compared to on-premises alternatives. Furthermore, the rise of specialized cloud providers offering GDPR compliant, EU hosted environments, such as Microsoft Azure sovereign cloud, has alleviated historical privacy concerns. Small and medium sized clinics, in particular, are embracing cloud solutions to access enterprise grade functionality without massive upfront investment. As the EHDS mandates cross border data sharing by 2027, the agility and standardization of cloud architectures position them as the inevitable future of clinical information systems in Europe.

By Component Insights

The software & systems segment led the market by holding 51.5% of the European market share in 2025. The growth of software and systems segment in the European market is attributed to the core function of these platforms as the central nervous system of modern healthcare delivery, integrating electronic health records, clinical decision support, order entry, and documentation into a unified digital environment. The complexity and continuous evolution of clinical software, driven by regulatory updates, interoperability standards, and new clinical workflows, ensure sustained investment beyond initial purchase. As per the European Observatory on Health Systems and Policies, large hospitals allocate a majority of their clinical IT budgets to software licensing, customization, and upgrades. Vendors like Epic, Cerner, and Dedalus command premium pricing for their comprehensive suites, which are deeply embedded in daily clinical operations. Unlike hardware, which has a finite lifecycle, software requires ongoing maintenance, module expansion, and compliance certification, creating a recurring revenue stream that anchors the entire market ecosystem.

The services segment is on the rise and is expected to exhibit a CAGR of 16.4% over the forecast period in this regional market. Factors such as the increasing complexity of system implementation, integration, and optimization in an era of regulatory transformation and technological convergence is propelling the expansion of the services segment in the European market. As hospitals migrate to new platforms or upgrade legacy systems to comply with the European Health Data Space, they require extensive consulting, data migration, workflow redesign, and staff training. As per the European Association of Hospital Managers, most healthcare IT leaders cite lack of internal expertise as their top barrier to successful digital transformation, necessitating external specialist support. Additionally, the shift toward value-based care models demands continuous system tuning to extract actionable insights from clinical data, which is fuelling demand for analytics and optimization services. Managed services for cybersecurity, cloud operations, and 24/7 helpdesk support further contribute to this growth, as institutions outsource non-core IT functions to focus on patient care.

By Application Insights

The hospital information systems (HIS) segment dominated the market by capturing 36.6% of the European market share in 2025. The growth of the HIS segment in the European market is attributed to their role as the foundational platform that integrates administrative, financial, and clinical functions across entire hospital enterprises. HIS modules manage everything from patient registration and bed allocation to billing and pharmacy orders, serving as the operational backbone for complex care delivery. As per the European Commission State of Health in the EU 2024 report, a majority of public hospitals in Western Europe have implemented comprehensive HIS platforms, driven by decades of policy incentives and efficiency mandates. The system’s centrality ensures continuous investment, as upgrades to one module, such as electronic prescribing, necessitate adjustments across the entire platform. Furthermore, national eHealth strategies in countries like Sweden and the Netherlands explicitly prioritize HIS modernization as a prerequisite for achieving interoperability and digital maturity, cementing its position as the cornerstone of clinical IT infrastructure.

The medical imaging information systems segment is the fastest-growing application segment in the Europe clinical information system market and is estimated to witness a CAGR of 17.4% over the forecast period owing to the exponential increase in diagnostic imaging volumes, the transition to digital radiology workflows, and the integration of artificial intelligence for image analysis. As per the European Society of Radiology, diagnostic imaging volumes have risen significantly, straining legacy film-based and siloed digital systems. Modern imaging platforms now combine PACS, VNA, and AI powered diagnostic tools that can detect anomalies in X-rays or mammograms with high accuracy. According to a validation study by the Karolinska Institute, AI integrated imaging systems have reduced radiologist workload while improving early cancer detection rates. As imaging becomes increasingly central to precision medicine and population health screening, demand for scalable, intelligent, and interoperable imaging platforms is surging across European hospitals and diagnostic centers.

By End Users Insights

The hospitals and clinics segment led the market by commanding for the highest share of 74.4% of the European market in 2025. The dominance of hospitals and clinics segment in the European market can be credited to their role as the primary sites of acute and chronic care delivery, where integrated digital systems are essential for managing complex patient journeys, coordinating multidisciplinary teams, and ensuring regulatory compliance. Large public hospitals, in particular, operate under intense pressure to optimize resource utilization and reduce medical errors, making advanced clinical information systems a strategic necessity rather than a luxury. As per Eurostat, there are thousands of hospitals in the EU employing millions of healthcare workers, creating a vast and stable customer base. National health authorities in countries like the UK and Germany have mandated EHR adoption as a condition for receiving public funding, further accelerating penetration. The scale and complexity of hospital operations ensure continuous demand for system upgrades, integrations, and support services, solidifying their position as the market’s core engine.

The diagnostic centers segment is growing at the fastest and is likely to witness a CAGR of 18.1% over the forecast period in this regional market. The decentralization of healthcare services, the rise of preventive screening programs, and the increasing outsourcing of imaging and laboratory testing by hospitals are propelling the expansion of the diagnostic services segment in the European market. As per the European Diagnostic Manufacturers Association, independent diagnostic facilities have grown significantly, fueled by aging populations and demand for faster, more accessible testing. These centers require specialized, streamlined clinical information systems that integrate laboratory information systems, radiology information systems, and patient scheduling into a single workflow. Unlike hospitals, they prioritize speed, cost efficiency, and interoperability with referring physicians’ EHRs. The adoption of cloud-based platforms allows them to scale rapidly without heavy IT infrastructure. As public health initiatives expand cancer screening and chronic disease monitoring, diagnostic centers are becoming critical nodes in the healthcare network, driving unprecedented demand for agile, purpose-built clinical IT solutions.

COUNTRY ANALYSIS Germany Clinical Information System Market Analysis

Germany dominated the clinical information system market in Europe in 2025 with 23.5% of the regional market share. The dominance of Germany in the European market is attributed to its advanced healthcare infrastructure and strong emphasis on data privacy. The country’s statutory health insurance system, which covers a majority of the population, mandates rigorous documentation and billing standards, driving widespread EHR adoption. As per the German Federal Ministry of Health, most hospitals and outpatient clinics use certified clinical information systems. Germany’s leadership in the Medical Informatics Initiative, a €200 million federal program connecting university hospitals via standardized data platforms, has created fertile ground for innovation in interoperable systems. However, strict interpretations of GDPR and a cultural preference for on-premises solutions have slowed cloud adoption. Despite this, the national push for the European Health Data Space is accelerating investments in FHIR compliant systems, ensuring Germany remains the region’s most sophisticated and valuable market for clinical IT vendors.

United Kingdom Clinical Information System Market Analysis

The United Kingdom captured a promising share of the Europe clinical information system market in 2025. The National Health Service that drives large scale digital transformation programs is contributing to the expansion of the UK market growth. NHS England’s Digital Transformation Strategy has committed billions to modernize IT infrastructure across all trusts by 2025, with a focus on integrated care records and interoperability. As per NHS Digital, most acute hospitals now use a core hospital information system, though legacy fragmentation remains a challenge. The UK pioneered national EHR initiatives like the Summary Care Record, which holds key clinical data for millions of patients. Recent policy shifts emphasize cloud adoption and real time data analytics to support predictive care models. The post Brexit regulatory environment allows for more agile procurement, enabling faster deployment of innovative solutions. This combination of top-down strategy, massive public investment, and a unified payer system makes the UK a high velocity market for next generation clinical information systems.

France Clinical Information System Market Analysis

France is estimated to command for a prominent share of the Europe clinical information system market over the forecast period. The ambitious national health data strategy and robust public investment are propelling the French market growth. The French government’s Ma Santé 2022 plan allocated billions to digitize healthcare, including the rollout of the Dossier Médical Partagé, a national shared medical record now used by millions of citizens. Hospitals are required to achieve Level 4 or higher on the HIMSS Digital Maturity Model to receive full public funding, creating a powerful incentive for system upgrades. France is also a leader in the European Health Data Hub, a federated research infrastructure connecting clinical data from major hospitals. As per the French National Authority for Health, most university hospitals have implemented advanced clinical decision support modules. This blend of regulatory mandate, citizen engagement, and research integration positions France as a dynamic and forward-looking market for integrated clinical IT solutions.

Italy Clinical Information System Market Analysis

Italy is predicted to showcase a healthy CAGR in the Europe clinical information system market over the forecast period. Italy is exhibiting significant regional variation but accelerating momentum due to EU recovery funds. The National Recovery and Resilience Plan has dedicated billions to healthcare digitization, with specific grants for EHR implementation in public hospitals. As per ISTAT, Italy’s national statistics institute, EHR adoption in hospitals is projected to rise significantly by 2026 due to targeted investments. The Lombardy and Emilia Romagna regions lead adoption, leveraging local health authority coordination to deploy integrated systems across networks of hospitals and clinics. A key driver is the need to manage Italy’s aging population, with a large proportion of citizens over 65 making chronic disease coordination a national priority. While legacy fragmentation persists, the influx of EU funds and centralized technical standards are rapidly closing the digital gap, transforming Italy into one of Europe’s most promising growth markets for clinical information systems.

Sweden Clinical Information System Market Analysis

Sweden is anticipated to record a notable CAGR in the Europe clinical information system market during the forecast period. Sweden is serving as a Nordic benchmark for interoperability and citizen centric design. The country’s National eHealth Agency has established a unified technical framework that enables seamless data exchange between all counties, which is resulting in one of the highest EHR adoption rates in Europe. As per the Swedish eHealth Agency, nearly all hospitals and primary care centers use interconnected clinical information systems that feed into the national Patient Summary. Sweden’s unique personal identity number system allows for lifelong health records that follow citizens across care settings. The government’s Vision for eHealth 2025 prioritizes AI enabled decision support and patient controlled data sharing. According to the Karolinska Institute, Swedish clinicians spend significantly less time on administrative tasks compared to their EU counterparts due to optimized digital workflows. This mature, standardized, and user focused ecosystem makes Sweden a model for scalable, high impact clinical IT deployment.

COMPETITIVE LANDSCAPE

The competition in the Europe clinical information system market is characterized by a dynamic interplay between established global vendors, strong regional champions, and emerging specialized innovators. Global players like Epic and Cerner compete on platform depth and research integration, primarily targeting large academic hospitals. European leaders such as Dedalus and CompuGroup Medical dominate through localized language support, regulatory alignment, and long-standing relationships with national health systems. Meanwhile, niche firms focus on specific applications like radiology or laboratory information systems, often leveraging cloud native architectures for agility. Intense rivalry is driving rapid innovation in areas like AI enabled diagnostics, federated data analytics, and patient centric portals. The European Health Data Space regulation is acting as a great equalizer, forcing all participants to adopt common standards and accelerating consolidation. However, fragmented procurement processes, legacy infrastructure, and varying national priorities sustain a complex and heterogeneous competitive landscape where no single vendor can claim dominance across all segments and geographies.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe clinical information systems market

- Cerner Corporation (An Oracle Company)

- Epic Systems Corporation

- Dedalus Group

- Allscripts Healthcare Solutions, Inc

- GE HealthCare

- Philips Healthcare

- McKesson Corporation

- Siemens Healthineers

- eClinicalWorks

- Meditech

- IBM Watson Health

Top Players In The Market

- Dedalus Group is a leading European provider of clinical information systems, offering a comprehensive portfolio of hospital information systems, electronic health records, and specialized clinical modules across more than 20 countries. Headquartered in Italy, the company plays a pivotal role in shaping the continent’s digital health landscape through its deep integration with national health services and commitment to interoperability. Dedalus contributes globally by advancing open standards like HL7 FHIR and supporting cross border health data exchange under the European Health Data Space framework. To strengthen its position, Dedalus launched its next generation AI powered clinical decision support platform across German and French hospitals in early 2025, enabling real time risk prediction for sepsis and other acute conditions. The company has also expanded its cloud hosted EHR offerings with sovereign EU data centers to address stringent privacy requirements while accelerating deployment for mid-sized clinics.

- Siemens Healthineers is a major force in the Europe clinical information system market, leveraging its legacy in medical technology to deliver integrated IT solutions that bridge imaging, laboratory, and enterprise clinical workflows. Its teamplay digital health platform connects diagnostic data with hospital information systems, creating a unified view of patient care. Globally, Siemens Healthineers drives innovation in precision medicine by embedding artificial intelligence into clinical decision pathways. In 2025, the company enhanced its Atellica Clinical Information System with advanced interoperability features compliant with the European Health Data Space, enabling seamless data sharing across public hospitals in Spain and the Netherlands. It also partnered with national eHealth agencies to deploy federated learning models that allow AI training on distributed clinical data without compromising patient privacy, reinforcing its leadership in secure, intelligent healthcare infrastructure.

- Epic Systems Corporation has established a growing footprint in the Europe clinical information system market, primarily through large academic medical centers and integrated care networks seeking enterprise-wide digital transformation. Known for its highly configurable and deeply integrated electronic health record platform, Epic enables longitudinal patient records across inpatient, outpatient, and community settings. Its global influence extends through standardized data models that facilitate international research collaborations. To reinforce its European presence, Epic opened a dedicated implementation and support center in Amsterdam in January 2025, staffed with multilingual clinicians and engineers to accelerate deployments. The company also achieved formal certification under the EU’s Electronic Health Record Quality Labeling scheme, demonstrating compliance with regional interoperability and security standards, thereby building trust among public health authorities and positioning itself for broader adoption across the continent.

Top Strategies Used by the Key Market Participants

Key players in the Europe clinical information system market are pursuing several strategic imperatives to secure competitive advantage. First, they are heavily investing in artificial intelligence and machine learning to embed predictive analytics and clinical decision support directly into physician workflows. Second, they are achieving formal certification under EU interoperability frameworks like the Electronic Health Record Quality Label to ensure compliance with the European Health Data Space. Third, they are expanding cloud-based deployment options with sovereign EU data hosting to address data residency concerns while improving scalability. Fourth, they are forming strategic partnerships with national eHealth agencies and university hospitals to co-develop and validate next generation digital health solutions. Finally, they are enhancing cybersecurity capabilities through zero trust architectures and continuous threat monitoring to protect sensitive patient data against escalating ransomware threats in the healthcare sector.

MARKET SEGMENTATION

This research report on the clinical information system (CIS) market is segmented and sub-segmented into the following categories.

By Deployment

By Component

- Hardware

- Software & Systems

- Services

By Application

- Hospital Information Systems

- Pharmacy Information Systems

- Laboratory Information Systems

- Revenue Cycle Management

- Medical Imaging Information Systems

- Radiology Information Systems

- Others

By End-Users

- Hospitals and Clinics

- Academic & Research Centers

- Pharmaceutical & Biotechnology Companies

- Diagnostic Center

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic