AlixPartners are most popular:

- with readers working within the Retail & Leisure industries

The European chemicals industry faces a challenging landscape

through to 2029–2030, according to the latest industry

forecasts. Despite hopes for a cyclical rebound, sentiment is now

leaning toward a structural shift rather than merely part of the

typical cycle.

There are four key issues currently facing the European

chemicals market:

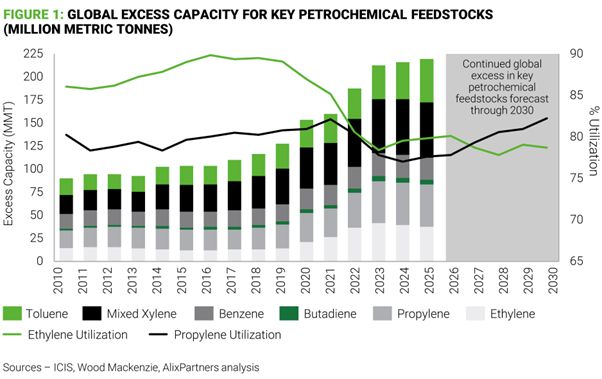

- No let-up in global overcapacity

Recent capacity additions, especially in Asia, have pushed

operating rates down towards 70%1in many European

countries, far below historical averages. The signs, however, are

that limited recovery is expected this decade.

Four new ethane-fed crackers (4.15 MMt/y combined) coming online

in Asia and Europe by 2027 will lower feedstock costs while further

expanding overall supply. Further global cracker capacity expansion

like this will drive the need for plant closures, especially assets

in high-cost regions such as Western Europe and Northeast Asia.

Japan will retire three naphtha crackers by 2028, while South Korea

targets 2.7–3.7 MMt/y of capacity reductions under government

restructuring.

Global overcapacity of basic chemicals is not expected to

recover through 2030, impacting price and adding to margin

pressure.

Beyond commodities, China is now rapidly scaling speciality

chemicals production, with double‑digit export growth since

2021. This expansion is eroding traditional Western advantages

based on differentiation and technical intimacy. In response,

speciality players increasingly require faster innovation cycles,

clearer commercial discipline, and stronger service models to

maintain competitiveness.

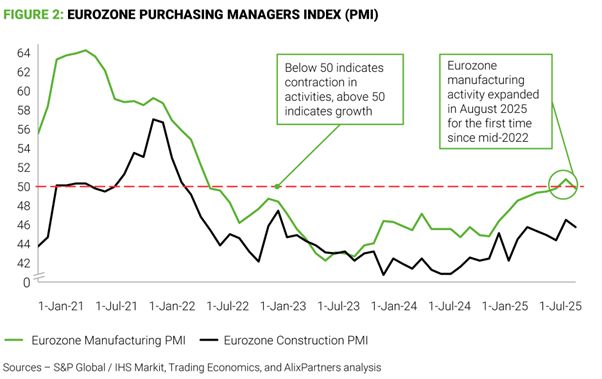

- Stagnant end-market demand

Downstream sectors heavily reliant on chemicals, such as

automotive, construction, and consumer goods, have contracted

across the Eurozone, creating a negative ripple effect across the

chemicals landscape.

Respite appears limited in the medium term, with the Euro Zone

Manufacturing PMI projected to trend around 51.50 points in 2026

and 52.00 points in 2027, so chemical producers can only expect a

gradual, modest recovery at best.

- Structural cost disadvantages

Europe’s reliance on natural gas imports means producers

face power costs that can be 3-4x higher than in the U.S. and Asia.

This, coupled with the higher cost of regulatory compliance in

Europe, yields structurally higher cost bases and eroded price

competitiveness compared to global counterparts.

European chemical industry players exposed to more

energy-intensive production processes (e.g., Titanium Dioxide,

isocyanates, polyamides, etc.) are even more likely to face higher

levels of stress if European energy cost disadvantages persist.

These chemical product groups also coincide with relative ease

of product transport, which facilitates imports from outside the

Euro Zone and creates even more elastic demand and price

competition.

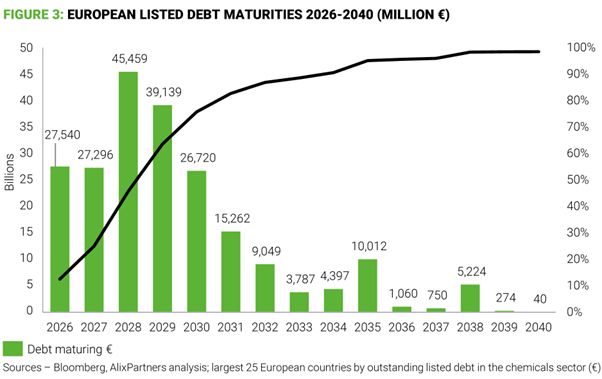

- Balance sheet and liquidity pressure

Sector leverage has risen in the wake of underperformance, and

the ongoing negative outlook creates refinancing risks for the

upcoming sector-wide maturity wall by 2029. Declining liquidity

across much of the sector compounds the issue and hinders

investment in business turnaround.

Borrowers and issuers of listed debt, most of which matures

before 2030, will be refinancing during a period when leading

operational indicators in both supply and demand are still expected

to be down from historic levels.

Market sentiment and valuation multiples are likely to factor

into this dimmer outlook, which in turn affects pricing,

transaction values and volumes, and strategic options.

So, what next?

The European chemicals sector faces sustained pressure, making

timely restructuring essential.Analysis indicates that the sector

is not merely in a cyclical trough, but in a structurally prolonged

downturn. Successful companies will act early, recognising that

market headwinds will persist and that inaction erodes value. A

clear, reset strategy and business plan are needed to address

underperformance and position the business for future

resilience.

Engaging stakeholders – especially lenders – builds

trust and supports a credible turnaround. Rigorous liquidity

management and a strong cash culture are vital to understanding the

runway and the delivery of the plan.

We’ve already seen several chemical businesses take

proactive action and provide examples for peers to follow. Across

the wide range of practical levers available, we highlight three

which we are most likely to benefit those under stress:

- Portfolio and plant rationalisation–

reviewing geographic profitability, analysing supply chain unit

economics, and refining the offering to where margin can be made is

fundamental to a chemicals turnaround plan. - Be aggressive in streamlining costs–

business owners and managers often take pride in lean structures;

however, our experience tells us there is often more that can be

done.Reducing overhead that doesn’t directly contribute to

profitability is a consistent lever for repurposing cash

utilisation. - You can never know too much about cash–

with large business plan revamps at stake, focus can be lost on the

short-term. Clarity over the cash outlook can make or break the

ability to take strategic action.

If you or your clients are interested in any of these topics,

please reach out to a member of our chemicals team listed below,

and we’d be very happy to discuss.

Footnote

1 Oxford Economics

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.